The World Bank’s Board of Directors on Saturday night in Kiev approved a new $432 million support package “Building Resilient Infrastructure in a Vulnerable Environment in Ukraine (DRIVE)” aimed at helping the government improve the resilience of the national road network and operational efficiency in the transport sector.

The Bank told Interfax-Ukraine that DRIVE complements the existing project “Rehabilitation of Essential Logistics Infrastructure and Network Connectivity (RELINC)”, under which modular road bridges were delivered and 200 flatcars were manufactured to increase Ukrzaliznytsia’s freight capacity and export capability.

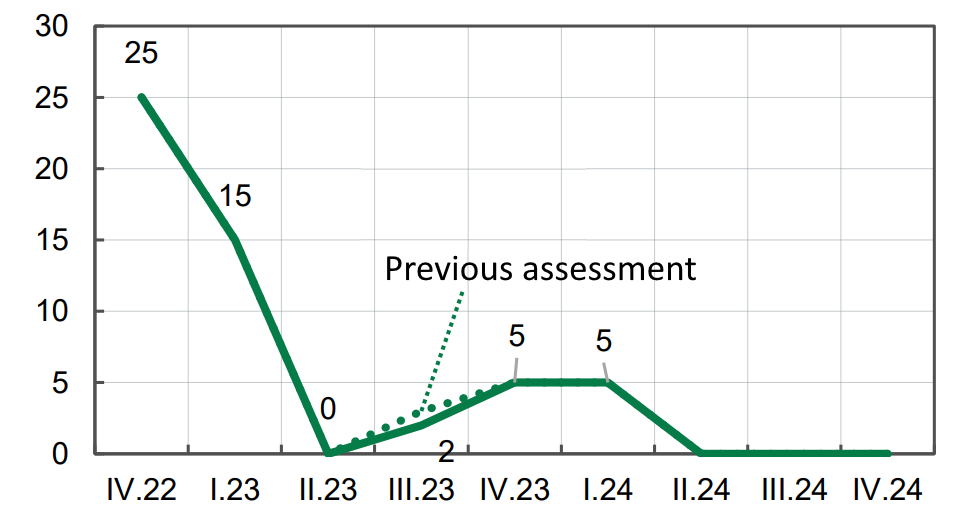

The World Bank noted that Ukraine’s transportation infrastructure has suffered significant damage since the war began in February 2022, disrupting key import and export routes. According to the recently published Rapid Damage and Recovery Needs Assessment (RDNA4), road infrastructure in the transport sector has suffered the most damage: 58% of the transport sector; 30% of state roads and bridges, 11% of local roads and bridges, and 17% of municipal roads suffered significant damage.

DRIVE financing includes a $212 million loan from the International Bank for Reconstruction and Development (IBRD) under the ADVANCE Ukraine (ADVANCE Ukraine) Trust Fund, which was supported by the Government of Japan. The financing also includes a $210 million loan from the Special Program for the Recovery of Ukraine and Moldova (SPUR) and a $10 million grant from the Ukraine Support, Recovery, Rehabilitation and Reform Trust Fund (URTF).

The project will be implemented by the State Agency for Infrastructure Rehabilitation and Development of Ukraine.

The project page on the Bank’s website notes that it has three components, the first of which is the preservation of the national road network. This component includes two components. The first, a $270.48 million investment for national roads, finances the design, execution, and supervision of construction works aimed at maintaining certain sections of national roads in proper operational condition, including through operational maintenance, major road repairs, and major bridge repairs.

The second component, National Roads and Road Transport Reform, allocates $90 million for transportation sector performance with a results-based approach.

The second component for $39 million is periodic maintenance of the national road network, it also has two components: installation of emergency modular road bridges and climate-smart preservation of key links in the road network.

The third component is technical assistance and project management, which also has two components: technical assistance and project development ($9 million URTF grant), which complements the investment-oriented components, and project management ($1 million URTF grant), which finances eligible costs for implementation and project management support, training, and knowledge sharing.

The death toll in Myanmar as a result of a powerful earthquake has exceeded 1,000 people, Reuters reports citing government sources.

“International rescue teams began flying to Myanmar on Saturday to help search for survivors after Friday’s earthquake killed more than 1,000 people,” the agency said.

The military government on Saturday put the death toll in Myanmar at 1,002. The 7.7-magnitude quake reportedly damaged critical infrastructure amid an intense civil war.

At least nine people were killed in neighboring Thailand, where the magnitude 7.7 quake destroyed buildings and collapsed a skyscraper under construction in the capital Bangkok, 30 people were trapped under the rubble and 49 were reported missing.

The National Bank of Ukraine (NBU) has added four insurance and/or reinsurance brokers to the Register of Insurance Intermediaries in accordance with the electronic applications submitted by them.

According to the NBU website, the following companies have been included in the said register: Insurance Broker Yutiar LLC, Aston Ukraine LLC, Representative Office of Yueidibibi Pragma Insurance Brokers, Representative Office of Marsh Europe C. A.” (all Kiev).

In addition, the National Bank has excluded these companies from the State Register of Insurance and Reinsurance Brokers and canceled the certificate of their inclusion in this register.

The relevant decisions were made by the Committee on Supervision and Regulation of Non-banking Financial Services Markets on March 27, 2025.

Issue #2 – March 2025

The purpose of this review is to provide an analysis of the current situation on the Ukrainian currency market and a forecast of the hryvnia exchange rate against key currencies based on the latest data. We analyze current conditions, market dynamics, key influencing factors, and likely scenarios.

Analysis of the current situation on the Ukrainian currency market

In the second half of March, Ukraine’s FX market remained relatively stable, showing predictable local fluctuations in the dollar and a more pronounced, albeit predictable, strengthening of the euro. Both developments were primarily driven by external factors, as the domestic FX market remained balanced due to high cash liquidity and active actions by the NBU.

The NBU’s informal signal to banks to raise deposit rates after the key policy rate hike is a classic soft pressure from the NBU, which is trying to keep hryvnia instruments attractive. One by one, banks raised hryvnia rates, confirming that they understood the NBU’s signals, which should potentially reduce demand for foreign currency from the population and encourage at least short- and medium-term savings in hryvnia, easing pressure on the exchange rate.

International factors affecting the market:

Ø The US Federal Reserve has been pursuing a consistent policy of lowering its key policy rate for several months now, clearly implementing a cycle of easing. This reduces the attractiveness of the dollar as an asset for investors and stimulates the flow of capital into alternative currencies and assets.

Ø In contrast, the European Central Bank gave positive signals about the improvement of the economic situation in the eurozone, which pushed the euro to a significant increase.

Ø The global market witnessed a moderate weakening of the US dollar and a strengthening of the euro, which became the main driver of changes in the exchange rates of key currencies in Ukraine.

Internal factors that influenced the foreign exchange market:

Ø Increased supply of cash foreign currency: according to the NBU, in February 2025, banks imported more than $1.08 billion in cash foreign currency to Ukraine, of which $749 million was in US dollars and $330 million in euros. This is a decrease compared to January ($1.77 billion), but remains high historically, ensuring high foreign exchange liquidity and exchange rate stability.

Ø In the dynamics of currency imports by banks, there is a well-established trend of increasing the share of euros in the total volume. From 13% at the beginning of 2024, the share of euros increased to more than 30% in 2025, reflecting the growing demand for euros among households and businesses.

Ø Deviations of cash exchange rates from the official exchange rate remain insignificant, which indicates that the regulator’s currency policy is effectively coordinated with market realities.

Overview of exchange rate dynamics

US dollar exchange rate

Ø In the second half of March, the dollar exchange rate against the hryvnia remained in the range of UAH 41.30-41.80 per dollar.

Ø The lowest value was recorded around March 13, after which the exchange rate gradually recovered.

Ø The spread between the bid and ask rates narrowed to 30-40 kopiykas compared to 50-60 kopiykas in February, indicating high liquidity and stability of the market.

Ø The deviation of market rates from the official NBU exchange rate remained minimal (± UAH 0.3), which is an indicator of the stability of expectations and the NBU’s predictable policy on the foreign exchange market.

Euro exchange rate

USD exchange rate forecast

Ø In the short term (2-4 weeks), the dollar is likely to remain in the range of UAH 41.25-42.00/$. The main factors will be maintaining high cash liquidity, the US Federal Reserve’s restrained policy, and the NBU’s active presence on the interbank market. Narrowing spreads and stable deviations from the official exchange rate give reason to expect low volatility in this market segment.

Ø In the medium term (2-4 months), demand for foreign currency may moderately increase amid higher budget spending, a pickup in business imports, and the seasonal effect of spring asset regrouping. In this case, the dollar could move up to the range of UAH 41.80-42.50/$.

Ø In the longer term (6+ months), a significant depreciation trend may resume with the potential for a shift toward UAH 45.00/$.

This scenario will be influenced by the general inflationary background in Ukraine, fiscal expectations for the exchange rate (budget target is 45 UAH/$), and risks with financing the state’s needs.

Ø However, the global monetary policy factor will remain restraining: if the US Federal Reserve moves to easing, the pressure on the hryvnia will be offset by global stability or even a weakening of the dollar.

Euro exchange rate forecast

In theshort term (2-4 weeks), the euro may consolidate in the range of 44.80-45.70 UAH/€ after the ultra-fast growth recorded in mid-March.

A correction phase or sideways movement is expected, which is typical for markets after a sharp move.

In the medium term (2-4 months), the euro’s dynamics will depend on the ECB’s decisions on interest rates and incentives, the state of the eurozone economy, and global demand for risky assets. In the baseline scenario, the exchange rate may remain in the range of 44.50-46.00 UAH/€. In the event of new positive signals from the EU, a retest of the 46.50 UAH/EUR level is possible.

In the long-term horizon (6+ months), the euro is more stable than the dollar due to structural market expectations, a gradual increase in its role in savings, and its growing role in foreign trade.

The forecast range is 45.00-46.50 UAH/€ with the potential for appreciation in case of sustained macro growth in the euro area.

Recommendations for businesses and investors

1. Diversification remains the basic strategy in a situation where the euro shows increased volatility and the dollar shows signs of structural weakening.

If you have liabilities in euros, it is advisable to gradually increase the share of this currency, but the dollar should be left as a short-term liquidity or hedge instrument.

2. Monthly review of the structure of foreign currency assets is relevant in the context of the NBU’s flexible currency policy, changes in external demand and potential exchange rate dynamics, especially if some assets are denominated in a currency other than the main operating currency.

3. Cautious currency speculation – only if you have the skills. Despite periods of short-term exchange rate volatility, especially in the euro, the current market is more predictable for experienced players, but carries significant risks for beginners.

Speculative strategies are justified only for those who have the resources and time to constantly monitor the market and have access to quick transactions at favorable rates.

4. The hryvnia should be maintained at its functional level. The current situation does not pose a threat of rapid devaluation, but it is not advisable to keep excess hryvnia liquidity. It should be used only to cover short-term expenses and to form reserves for unforeseen events.

5. For the first time in almost a year of currency market reviews, we can recommend considering short-term hryvnia deposits for 1-4 months, a logical tactic for “temporary parking” of free funds without currency risk in the context of banks raising interest rates to ~15% per annum, which are now at least slightly ahead of official inflation. For the same reasons, a short-term “parking” of free hryvnia in government bonds can be considered. Longer-term hryvnia investments are risky given the likely acceleration of inflation and a possible exchange rate shift in the second half of 2025, which is most likely to occur in the fall of this year. Yields on foreign currency deposits remain symbolic and do not cover the risks of liquidity ties.

6. Maximum liquidity is a top priority: in the face of geopolitical and economic turbulence, all foreign currency assets should be available for operational maneuver.

This material was prepared by the company’s analysts and reflects their expert, analytical professional judgment. The information presented in this review is for informational purposes only and cannot be considered as a recommendation for action.

The Company and its analysts make no representations and assume no liability for any consequences arising from the use of this information. All information is provided “as is” without any additional warranties of completeness, obligations of timeliness or updates or additions.

Users of this material should make their own risk assessments and make informed decisions based on their own assessment and analysis of the situation from various available sources that they consider to be sufficiently qualified. We recommend that you consult an independent financial advisor before making any investment decisions.

REFERENCE

KYT Group is an international multi-service product FinTech company that has been successfully operating in the non-banking financial services market for 16 years. One of the company’s flagship activities is currency exchange. KYT Group is one of the largest operators in this segment of the Ukrainian financial market, is among the largest taxpayers, and is one of the industry leaders in terms of asset growth and equity.

More than 90 branches in 16 major cities of Ukraine are located in convenient locations for customers and have modern equipment for the convenience, security and confidentiality of each transaction.

The company’s activities comply with the regulatory requirements of the NBU. KYT Group adheres to EU standards, having a branch in Poland and planning cross-border expansion to European countries.

IC “Express Insurance” (Kiev) in January-February 2025 collected insurance premiums in the amount of UAH 181,6 mln, which is 48,4% more than in the same period of 2024, as reported on the insurer’s website.

The increase in insurance premiums has become possible due to significant growth of new clients and stable increase in the number of concluded contracts in comparison with the previous year.

Thus, premiums under CASCO contracts for this period amounted to UAH 119,1 mln, which is by UAH 21 mln or 21,4% higher than the same indicator of two months of 2024, under CMTPL insurance – UAH 56,9 mln (+ 2,8 times), under other types of insurance – UAH 5,6 mln.

As reported, in January-February 2025, the company made payments in the amount of UAH 67,2 mln.

IC “Express Insurance” was founded in 2008 and is a part of the group of companies “UkrAVTO”. It specializes on automobile insurance. Stable high speed of events settlement in IC is provided by optimal interaction with partner service stations.

Since April, 2012 IC “Express Insurance” is an associated member of the Motor Transport Insurance Bureau of Ukraine.