The group of the seller in a transaction to acquire Preludium B.V. (the Netherlands), through which MTS Group owns the second largest mobile communications operator in Ukraine, PrJSC VF Ukraine (Vodafone Ukraine), by Azerbaijan’s Bakcell telecom operator will terminate control over Preludium B.V.

According to the decision of the Antimonopoly Committee of Ukraine (AMCU) of October 24, 2019, published on the agency’s website on Tuesday, the parties to the transaction have already agreed on the obligations of the Luxembourg subsidiary of MTS Allegretto Holding Sarl to refrain from competing with Vodafone Ukraine for three years territory of Ukraine.

In addition, PJSC Mobile TeleSystems undertakes not to lure employees (unless otherwise agreed between the parties) and Vodafone Ukraine suppliers.

According to the document, at present Bakcell LLC does not carry out economic activities in Ukraine. He is controlled by an individual a citizen of Azerbaijan and business entities non-residents of Ukraine, forming the Bakcell group.

Bakcell, founded in 1994, is the mobile communications operator and a leading provider of mobile Internet in Azerbaijan. It operates in GSM, UMTS and LTE standards.

Bakcell network consists of more than 7,500 towers, covers 93% of the territory (excluding occupied territories) and 99% of the population of Azerbaijan. The company has more than 3 million subscribers.

According to the results of 2018, Vodafone Ukraine reduced its net profit by 18.1% compared to 2017, to UAH 1.8 billion. The company explained this figure as an increase in costs due to the active deployment of 4G and 3G networks.

Vodafone Ukraine is fully owned by Preludium B.V. It is part of the international MTS Group, which shares are listed on the New York Stock Exchange.

President of Ukraine Volodymyr Zelensky has instructed to eradicate total corruption in the field of state architectural and construction control and urban planning by the end of 2019, a president’s press service reported. Zelensky set the appropriate task to Minister of Development of Communities and Territories Olena Babak during a meeting with the leadership of the Verkhovna Rada and the Cabinet of Ministers in the President’s Office.

The head of state noted the need to switch rendering of the administrative services in construction to an electronic format and introduce automatic registration in the register of approval documents.

As the President’s Office reported, Zelensky commissioned Minister of Justice of Ukraine Denys Maliuska to change the software of real estate and business registers to stop unauthorized access. Besides, by the end of June 2020, Maliuska must ensure the formation of the legislative framework for the operation of an electronic notarial system.

The Cabinet of Ministers of Ukraine has amended the charter of the Energy Efficiency Fund, increasing its charter capital by UAH 1.119 billion, MP Oleksiy Honcharenko has said. “The Cabinet of Ministers has increased the charter capital of the Energy Efficiency Fund by UAH 1.119 billion,” he said on Telegram.

The decision will allow implementing 2,041 thermal modernization projects for multi-apartment buildings, the press service of the Ministry for Community and Territory Development said.

As reported, the national budget of Ukraine for 2019 foresees UAH 1.6 billion for the charter capital of the Energy Efficiency Fund.

The Energy Efficiency Fund intends within five years to finance more than 16,000 projects under the energy modernization program for the associations of co-owners of multi-apartment buildings.

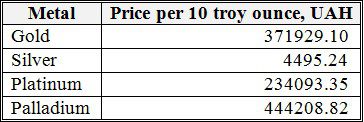

Official rates of banking metals from national bank as of November 06

One troy ounce=31.10 grams

Financing for the Education and Science Ministry of Ukraine increased by 14% in the draft national budget of Ukraine for 2020, prepared by the government for second reading, to UAH 131.483 billion, as compared with 2019, according to bill No. 2000 dated September 15 amended for second reading.

In particular, UAH 44.331 billion will be allocated for the apparatus of the Education and Science Ministry, of which UAH 134.9 million will be spent on management and administration in the spheres of education and science, UAH 107.6 million – on organization of work of the National Agency for Higher Education Quality Assurance, National Agency for Qualification, education ombudsman, state attestation and accreditation and educational institutions, UAH 200 million – on professional (vocational) training of national significance, and UAH 1.162 billion – on research and development at higher education establishments and scientific institutions.

National bank of Ukraine’s official rates as of 06/11/19

Source: National Bank of Ukraine