Boryspil International Airport (Kyiv), the country’s largest airport, in the first nine months of 2018 increased passenger traffic by 19%, to 11.67 million people against 9.768 million in the same period of 2017, the press service of the airport has told Interfax-Ukraine. In November, the airport served 994,200 passengers, which is 33% more than in November 2017.

Some 8.936 million passengers of Boryspil airport travelled on regular flights in the 11 months, while 2.731 million people chose irregular flights.

The share of transfer in the total passenger traffic of the airport in January-November decreased to 27%, while over the 11 months of 2017 it was 28%.

At the same time, the number of transfer passengers increased from 2.72 million last year to 3.192 million in the 11 months of 2018.

PJSC Farmak pharmaceutical company (Kyiv) has opened a new section of tablet production, investment in which amounted to EUR 20 million. Head of the supervisory board of the company Filia Zhebrovska said at the ceremony of opening the site in Kyiv that this project will allow Farmak to double the capacity of production of solid dosage forms to 3 billion tablets per year.

In general, it is planned in 2019 to transfer and master production of about 30 goods at new site TLF-2, including the drugs from the Available Medicines reimbursement program. Zhebrovska noted that the latest technology of pharmaceutical production and the most modern equipment are used on the site. The project has been implemented during two years. Due to the increase in capacity, Farmak will create almost 100 new jobs. “Our state needs investments for economic growth, contributing to the development of production and strengthening Ukraine’s position in the international arena,” she said.

Equipment from the leading European brands Glatt, IMA, Marchesini and others has been installed at Farmak’s new production site, which provides the entire technological cycle of tablet production from accepting and processing raw materials to the final dosage forms.

The opening of the production site brings PJSC Farmak closer to the strategic goal: the increase in exports to 40% by 2023.

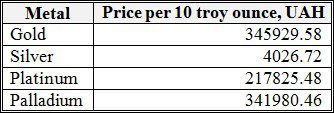

One troy ounce=31.10 grams

The Ukrainian Sea Ports Authority and Port of Antwerp International/APEC (Belgium) have signed a memorandum of understanding. The document provides for a detailed analysis of the strengths and weaknesses of Ukrainian seaports and further interaction in order to attract investment in their development. “Experts from Port Antwerp International will conduct a SWOT-analysis of the situation in Ukrainian seaports and will formulate a plan of partnership assistance in implementation of the development strategy of Ukrainian seaports,” Ukrainian Sea Ports Authority Head Raivis Veckagans said.

He said that trainings for specialists of the Ukrainian authority start this week in the areas of pricing for port services, work within the framework of port landlord model, concession project implementation, as well as the peculiarities of the interaction of environmental services in the port.

Managing director of Port of Antwerp International and the APEC Port Training Center Kristof Waterschoot said that the Black Sea region and, in particular, the seaports of Ukraine are now at the center of attention of international experts.

The Ukrainian authority also said that Port of Antwerp International is acting internationally, not only as a consultant, but also as an investor. In particular, the company invested $10 million in Porto do Aç (Brazil) in 2017 and more than $2 million in the port of San Pedro (West Africa) in 2016.

“Further cooperation with Ukrainian ports will also consider the possibility of Belgian and international experts participation in attracting investments and implementing projects on development of port infrastructure in the seaports of Ukraine,” the authority said.

The volume of state financing of the rocket and space industry of Ukraine in 2019 should amount to UAH 2.13 billion, which is 14% less compared to 2018. These parameters are stipulated in the country’s main financial law for 2019, which has been posted on the Verkhovna Rada’s website. State financing for the space industry from the general fund of the national budget of 2019 will amount to UAH 2.12 billion (99.5% of the budget).

In the total amount of funding for the industry through the general fund, UAH 1.47 billion (69% of the industry budget) should be used for servicing debt obligations on the loan raised under state guarantees for the implementation of the project “Creating the National Satellite Communications System.” In 2018, some UAH 1.55 billion (62.5%) was foreseen for this purpose.

Some UAH 78.5 million is foreseen for carrying out work on state targeted programs and government orders in the space industry in 2019, which is 9.8% less than in 2018, while UAH 344.8 million will be spent on management and testing space vehicles, or 14% less compared to 2018.