The use of artificial intelligence has already become an everyday practice for most students and employees; however, in the labor market over the coming years, the key competitive advantage will remain not technical but human skills — communication, leadership, emotional intelligence, critical thinking, and the ability to work with people. This was the conclusion reached by participants in the press conference on the topic “Higher education and MBA education in the era of artificial intelligence. Which professions and skills will remain with humans?”, which took place at the Interfax-Ukraine agency on Wednesday.

As Director of the Center for Business Education and Advanced Training of the Institute of Psychology and Entrepreneurship Maria Furman reported, the study, conducted on the basis of cooperation between students and business, covered more than 250 respondents from the fields of law, HR, IT, consulting, marketing, management, foreign economic activity, education, sales, and finance.

“Currently, more than 97% of respondents already use artificial intelligence in work or everyday life, and more than 50% turn to it at least once a day. The most widespread tools turned out to be ChatGPT, Google Gemini, Claude, and Copilot, while the main usage scenarios were explaining complex information, writing and editing texts, generating ideas, translation, data analysis, and preparation of summaries,” she noted during the presentation of the study “The Use of AI in Work and Everyday Life.”

At the same time, according to Furman, the spread of AI does not mean an automatic increase in trust in its answers. She drew attention to the fact that about 30% of daily functions are already being replaced by such tools; however, the largest share of respondents assessed the level of trust in AI answers as moderate — information can be trusted only on condition of verification. More than 50% of respondents always verify generated answers, another 33% do so if the information looks suspicious, and 13% do so when it concerns especially important work. In addition, more than 30% of respondents very often encountered distortion of information, while another 53.6% reported that such cases had happened to them several times.

“According to estimates by the World Economic Forum, by 2030 more than 40% of skills in the world will change, and this means a need for rapid retraining of both current employees and students. She emphasized that higher education must not simply familiarize young people with digital tools, but rebuild approaches to learning in such a way as to prepare specialists capable of working together with AI, rather than mechanically relying on it,” the expert stressed.

According to her, artificial intelligence has already become part of education and business, but its effect lies not in the complete replacement of humans, but in the transformation of their functions.

“That is precisely why analytical thinking, communication, adaptability, people management, emotional intelligence, and creativity are of particular value today,” Furman stressed.

She added that AI will not be able to displace managers, psychologists, HR specialists, communications managers, teachers, mentors, as well as those responsible for strategy and team development, since in these professions human trust, leadership, empathy, and the ability to work with context remain decisive.

For her part, Doctor of Economics, Professor, Vice-Rector for Scientific-Pedagogical and Educational Work of the Institute of Psychology and Entrepreneurship Iraida Zaitseva emphasized that even the most powerful algorithms cannot replace a leader, since they are devoid of consciousness, creativity, and moral reflection. She recalled that a machine can advise cutting staff for the sake of higher profit, but is not capable of assessing the social, ethical, and even geopolitical consequences of such a decision.

“Artificial intelligence is a powerful engine, but only a human should be the pilot who knows where and why they are flying. We teach students not simply to use the tool, but to validate decisions, critically treat the algorithm’s ‘black box,’ and bear personal responsibility for the result. At the institute, AI is allowed to be used as an auxiliary means for structuring material or searching for ideas; however, the student is obliged to indicate the fact of its use, verify sources, and be responsible for the content of the work, otherwise this may be regarded as academic dishonesty,” Zaitseva noted.

CEO of Capolavoro Group (Brazil), lecturer at the Brazilian AMF institute, and investor in technology startups Wesley Lacerda focused attention on the risks of the improper use of artificial intelligence in business. In his assessment, the main danger lies not only in the technology as such, but in the gradual cognitive weakening of a person, when the user becomes accustomed to transferring their own memory, analytical abilities, speech, and even elementary ability to make independent decisions to the machine. In his presentation, he separately named cognitive deterioration, decline of intelligence, weakening of the ability for reflection, and loss of social skills as the main risks of the broad implementation of AI.

“Artificial intelligence should be used as a tool for data analytics, not as a replacement for human thinking. When a person ceases to understand what stands behind the machine’s answer, they lose their own cognitive abilities, and together with them, the ability to make independent decisions,” Lacerda noted during his presentation.

He also drew attention to the fact that the new wave of automation is generating demand first of all for AI analysts, AI engineers, specialists in AI Ops, and algorithmic audit, and not only and not so much simply for IT specialists. However, even in these roles, what remains decisive is the human understanding of what is being done and for what purpose, and not only the ability to write the correct prompt for the machine.

For her part, 3S Agency recruiter Sofia Vorushko emphasized that in the hiring sphere, artificial intelligence creates an illusion of objectivity, but still cannot replace a live recruiter. According to her, candidates are increasingly better prepared for interviews with the help of AI, use correct wording and socially desirable answers; however, the algorithm is not capable of fully reading non-verbal signals, understanding a person’s motivation, their real experience, and their fit with the culture of a specific company. She gave the example of two seemingly identical executive assistant vacancies, for which in practice completely different candidates were needed due to the different management styles of the managers.

“Today the market is evaluating an employee less and less only by hard skills and more and more by soft skills. Communication, resilience, flexibility, adaptability, leadership, and the ability to build relationships are becoming critically important, because they are the hardest to automate,” Vorushko added.

She referred to global estimates according to which 63% of employers call the shortage of soft skills a barrier to business development, 67% of companies are looking for flexibility and adaptability, 61% — leadership and social influence, while demand for social and emotional skills will grow by another 24% by 2030. According to the recruiter, currently 75% of an employee’s long-term success depends specifically on soft skills, while hard skills account for only about 20%.

At the same time, Director of LLC “Formatsiya” Mykola Hoi noted that for a business built on communication with clients, partners, dealers, manufacturers, and suppliers, the direct transfer of decisions to AI is extremely limited. According to him, in his company, which operates in the field of solar energy, about 95% of working time is precisely work with people, and therefore template algorithms are not capable of fully replacing live contact either in sales, in team selection, or in the development of marketing solutions.

“In business, artificial intelligence can be used, but only if its limits are understood very clearly. Founding a business, selecting a team, marketing, sales, work with the client, and rapid decision-making in a changing environment remain the zone of human responsibility, because here what is needed is not templates, but knowledge, experience, and understanding of another person,” Hoi stressed.

He added that the use of AI in HR processes can lead to mistakes if a company tries to assess candidates only by formal features, without giving a person the opportunity to reveal their potential in live communication.

Separately, the participants noted that the Institute of Psychology and Entrepreneurship is focusing on specialties that, in the opinion of the organizers, are least susceptible to automation: personnel management, communicative management, and psychology. The institution reported that the cost of bachelor’s studies is UAH 42 thousand per year, and at the college — UAH 28 thousand per year; cooperation was also announced with partners in the Baltic countries, as well as in Poland, the UAE, and Brazil, where students can undergo internships. Thanks to the ontological approach, which helps develop the personality, and the combination of psychology with up-to-date knowledge from business practitioners, the institute’s students comprehensively develop personal and professional skills. This helps them become high-level managers and not be dependent on technologies. This level of training allows students, starting from the second year, to work in business projects in their professional specialty.

Summing up the discussion, the experts agreed that Ukrainian higher education and MBA programs can no longer ignore artificial intelligence, but also should not make it an end in itself. It is not about a struggle between human and machine, but about a new distribution of roles, in which AI takes over routine, analytical, and technical functions, while strategy, ethics, creativity, empathy, team management, and responsibility for decisions remain with humans. It is precisely these qualities, in the opinion of the event participants, that will determine a specialist’s competitiveness in the next 5–10 years.

AI, EDUCATION, Formatsiya, HR, INSTITUTE OF PSYCHOLOGY AND ENTREPRENEURSHIP, IRAIDA ZÁITSEVA; CAPOLAVORO GROUP, LEARNING, MARIA FURMAN, MYKOLA HOI, RECRUITING, SOFÍA VORUSHKO, WESLEY LACERDA; 3S AGENCY

The Experts Club analytical center has analyzed the latest trends in the metallurgical sector and the data of the industry’s largest association, the World Steel Association. In 2026, according to the World Steel Association, the global steel market will move from a phase of prolonged adjustment to weak growth: global demand will increase by 0.3%, to 1.724 billion tons, and in 2027 it will accelerate to 1.762 billion tons, or by 2.2%. The association itself believes that the market is passing through the bottom of the 2025–2026 cycle after the structural pressures that had restrained demand since 2022. This means that the global steel industry is gradually emerging from its downturn, but it is doing so very unevenly across regions.

The key conclusion for Ukraine is that the external environment for metallurgy is, on the whole, no longer deteriorating. Worldsteel expects that in 2027 all major developed economies, including the EU, the US, Canada, Japan, and Korea, will already show positive steel demand dynamics. For the EU and the UK, steel consumption is forecast to grow by 1.3% in 2026 and by 3% in 2027, while for the US the figures are 1.7% and 2% respectively. This is important for Ukraine because the European market remains its main external reference point, both in terms of steel product sales and future industrial cooperation.

At the same time, the recovery in global demand will be asymmetric. China, which still determines the global market environment, will continue to reduce steel demand in 2026, though only by 1.5%, and in 2027, according to the association, will move to almost flat dynamics. The main driver of growth among major markets remains India, where demand is expected to increase by 7.4% in 2026 and by 9.2% in 2027. In the developing world excluding China, growth, on the contrary, will slow to 2.5% in 2026 because of the conflict in the Middle East, but will then recover.

For Ukraine, this means that the global market does not promise a sharp price or volume breakthrough, but neither does it create a scenario of a new collapse. In other words, over the next two years the decisive factor for Ukrainian metallurgy will no longer be so much global demand as Ukraine’s own ability to maintain and expand steelmaking, ensure energy supply, logistics, and access to export routes. In this sense, the external market environment is becoming moderately favorable rather than deteriorating, but it is not a saving grace.

Against this background, Ukraine’s own indicator looks restrained. At the end of 2025, the country produced 7.409 million tons of steel, which was 2.2% lower than the 2024 level, and ranked 21st in the world. This figure is significantly lower not only than pre-war levels, but also below the scale that once allowed Ukraine to influence the regional market as one of the major European players.

If the global market is indeed entering a phase of moderate recovery, then the window of opportunity for Ukraine will be determined not so much by whether global demand grows by 0.3% or 2.2%, but by whether the country can restore production volumes at least to a stable double-digit level in millions of tons. Worldsteel’s positive outlook for the EU, growing infrastructure and defense spending in Europe, as well as stabilizing demand in the developed world create the basis for higher consumption of Ukrainian steel in the future. But this opportunity will be realized only if Ukraine restores its own industrial capacity, not automatically.

In a broader sense, the Worldsteel forecast shows that steel is once again becoming an indicator of industrial policy. Where infrastructure investment, railways, defense budgets, and machine-building are growing, demand for metal returns. Ukraine’s post-war recovery strategy should consider metallurgy not as a separate export sector, but as a foundation for construction, machine-building, transport infrastructure, and defense production. Only in this case can even moderate global growth translate into a more tangible internal industrial effect for the country.

The World Steel Association (Worldsteel) brings together steel producers, industry associations, and research institutes from all key steel-producing countries. The association’s members account for around 85% of global steel output.

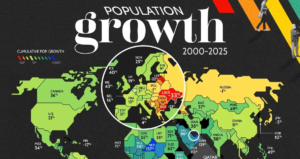

Over the past 25 years, the world’s demographic dynamics have increasingly diverged in two directions: some countries are experiencing explosive population growth, while others are facing steady decline. According to a Visual Capitalist visualization based on UN data, in 2000–2025 the largest population decrease was recorded in Ukraine, while the fastest growth was seen in Qatar. The study is based on the estimates and projections of the UN’s World Population Prospects 2024.

The top 10 countries by population decline in 2000–2025 included Ukraine (-32.5%), the Marshall Islands (-29.4%), Bulgaria (-23.2%), Latvia (-21.6%), Moldova (-18.8%), Lithuania (-17.5%), Puerto Rico (-16.7%), Romania (-16.1%), Serbia (-13.1%), and Albania (-12.8%). The top 10 countries by population growth included Qatar (+423.4%), the UAE (+249.7%), Equatorial Guinea (+166.6%), Niger (+157.0%), Bahrain (+153.9%), Papua New Guinea (+149.6%), Angola (+139.7%), Kuwait (+139.1%), Oman (+129.1%), and Chad (+126.9%). These figures were cited by Visual Capitalist in two April publications.

For Ukraine, this ranking is especially alarming. According to Visual Capitalist, the country lost about one-third of its population over 25 years. The broader demographic background is also confirmed by materials from Our World in Data based on UN data: in 2022–2023 alone, net migration from Ukraine amounted to around 6 million people, which became a direct consequence of the full-scale war.

Experts Club believes that Ukraine’s demographic crisis has already become not only a social issue, but also an economic one. Population decline means a shrinking domestic market, a worsening labor shortage, growing pressure on the pension and healthcare systems, as well as deteriorating long-term conditions for investment. This logic is consistent with UN assessments of the role of declining birth rates, population aging, and migration in shaping new global demographic imbalances.

At the same time, the global picture also shows the opposite pole. The growth leaders — primarily the Gulf countries and a number of African states — increased their populations either through a massive inflow of labor migrants or through high birth rates. The UN notes that global population growth is continuing, but its pace is slowing, and the main contribution to further population increase will come not from Europe, but primarily from Africa and certain migration centers.

For Ukraine, this leads to at least two conclusions. First, without the return of at least part of the citizens who have left, support for families with children, and a stronger labor market policy, the demographic decline will continue to undermine the economy. Second, the problem has long gone beyond statistics: in the coming years, demography may become one of the main constraints on the country’s post-war recovery.

On April 19, early parliamentary elections will take place in Bulgaria — already the eighth since 2021. The vote is taking place against the backdrop of prolonged political instability, declining trust in institutions, protests at the end of 2025, and a new surge of struggle around the issue of corruption. According to the assessment of OSCE/ODIHR, the elections are being held under conditions of ongoing fragmentation of the political field and high polarization.

The information and analytical center Experts Club notes that the current campaign is particularly important for the region, as Bulgaria remains a member of the EU and NATO, controls part of the western coast of the Black Sea, and after joining the eurozone from January 1, 2026, has become even more deeply integrated into the European architecture. At the same time, Sofia currently appears to be one of the most politically vulnerable countries in Southeastern Europe.

The main intrigue of the campaign is whether former president Rumen Radev will be able to transform his personal popularity into a stable parliamentary majority. According to AP, his new coalition Progressive Bulgaria approaches the elections as the favorite and in most polls receives over 30% of the vote, ahead of its closest competitor by almost 10 percentage points. In a fresh survey by Gallup International Balkan, published on April 18, among decided voters Progressive Bulgaria receives 30.7%, GERB-UDF — 20.4%, and the pro-European coalition Continue the Change — Democratic Bulgaria — 10.4%. They are followed by MRF – New Beginning with 10.2% and Vazrazhdane with 6.6%; BSP-United Left is at the threshold with 3.9%.

Thus, the main players in these elections look as follows. First, “Progressive Bulgaria” of Rumen Radev — a new center-left coalition that builds its campaign on the promise to break the “oligarchic model” and relaunch governance of the country. Second, GERB-UDF of Boyko Borisov — a traditionally strong center-right force that has long dominated Bulgarian politics. Third, Continue the Change — Democratic Bulgaria, a centrist and pro-European bloc that focuses on an anti-corruption agenda. MRF — New Beginning, associated with the Turkish minority, and the nationalist Vazrazhdane, which a number of European sources characterize as a Eurosceptic and pro-Russian force, are also highly likely to enter parliament.

Preliminary results as of 12:00, according to the Bulgarian outlet “Dnevnik,” confirm the lead of Radev’s party.

The reason for the current vote was the collapse of the previous governing structure. According to OSCE/ODIHR, after the elections in October 2024, a minority government was formed headed by Rosen Zhelyazkov. Then a decision of the Constitutional Court in March 2025 changed the distribution of mandates, the coalition lost its margin of stability, and in December 2025 the cabinet resigned amid protests and corruption allegations. After unsuccessful attempts to form a new government, the presidential mandate cycle ended in failure, and the country went to new elections.

Even if Radev comes first, this does not automatically mean the emergence of a stable government. He has already ruled out an alliance with Borisov’s GERB and with DPS, and the most logical potential partner in terms of the domestic anti-corruption agenda could be the coalition “Continue the Change — Democratic Bulgaria.” However, this is where the main barrier arises: foreign policy. Radev condemns the war, but has opposed military aid to Ukraine and supported the resumption of dialogue with Moscow, while the pro-European bloc adheres to a much tougher line.

For the region, this makes the Bulgarian elections far more important than a typical domestic political campaign. In the event of a convincing victory for Radev, Sofia will of course not leave the EU and NATO, but may become more cautious and less predictable on issues of support for Ukraine, sanctions policy, and the overall line toward Russia. This is why Western media and analysts view Bulgaria as one of the potential pressure points on European unity following changes in the political landscape of neighboring countries.

A separate risk factor is the information environment. Euronews, citing the Center for the Study of Democracy, writes that Bulgaria remains one of the most vulnerable countries in the EU to malicious information manipulation, and the authorities have even engaged EU mechanisms to counter possible interference and disinformation ahead of the vote. Against this background, special attention is focused on the nationalist party Vazrazhdane, which has already figured in controversies around anti-Western and anti-eurozone narratives.

For the Balkans and the Black Sea region, three main scenarios are possible. The first is Radev’s victory followed by a complex but workable coalition agreement. In this case, Bulgaria may become a more autonomous and less ideologically pro-European actor, which will increase uncertainty for Ukraine and complicate coordination within the EU on security issues. The second is a victory without the ability to form a government. In that case, Bulgaria risks entering again a cycle of short-lived governing formulas and caretaker governments, which will weaken its role in regional projects and in Black Sea policy. The third is a weaker result for the favorite and an attempt by traditional pro-European forces to form an alternative coalition. Such a scenario would appear the most comfortable for Brussels, but for now is not considered the baseline scenario.