The number of cars subject to luxury tax decreased threefold over the year

According to the Ministry of Internal Affairs, 504 vehicles subject to luxury tax were imported into the country last year.

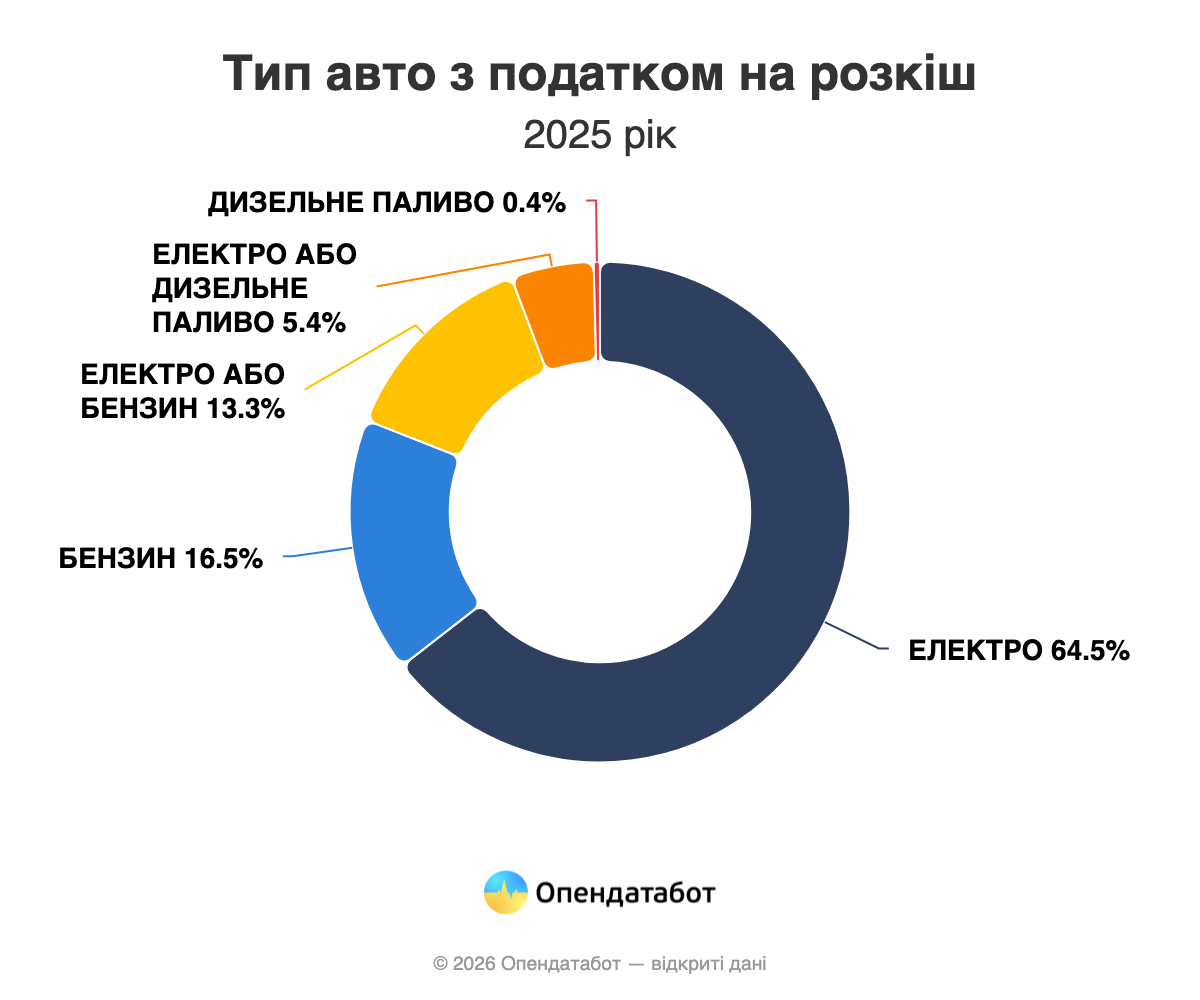

This is the lowest figure in the last five years. Porsche and Mercedes-Benz account for 89% of luxury vehicles, and every second such car is a Porsche Taycan. In total, electric cars account for 65% of all cars subject to luxury tax.

504 cars subject to the “luxury tax” were imported into Ukraine in 2025. This is 3.2 times less than in 2024. Overall, this is the lowest figure in the last five years.

Every second car on the “luxury” list is a Porsche Taycan: 232 cars. Overall, Porsche became the leader in the luxury segment with additional taxation: cars of this brand account for 64% of the total volume. Mercedes-Benz took another quarter of the market with 126 cars. The rest of the premium brands together account for 11% of the market: Audi, Rolls-Royce, Aston Martin, Lamborghini, Maserati, etc.

It is worth noting that, in contrast to overall imports, electric cars dominate the premium segment: 65% of imported luxury cars. Another 18% are hybrids that can run on electricity as well as gasoline or diesel. Pure gasoline cars, the leaders in overall imports, are at the bottom of the list with 17%. Diesel accounts for a symbolic 0.4%.

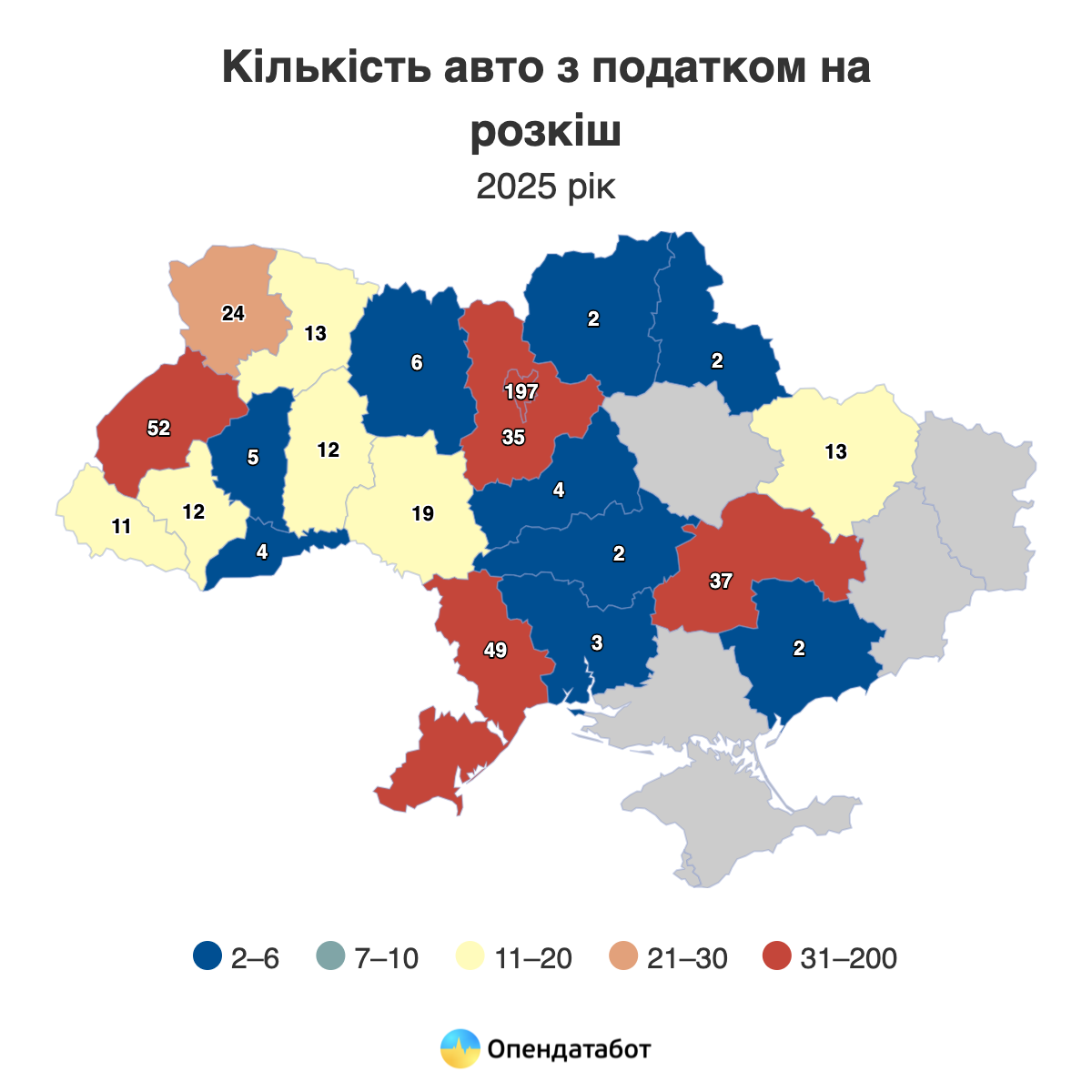

Almost half of all luxury cars are registered in Kyiv and the surrounding region: 236 cars. Another 52 cars are in Lviv region, 49 in Odesa region, and 37 in Dnipropetrovsk region.

Most of the cars in the luxury segment are registered to individuals — 82% or 413 cars. Only 18% of such cars are registered to businesses.

The ultra-premium segment deserves special attention. Last year, 21 Rolls-Royces were imported into Ukraine. Fifteen of them are the electric Spectre model, which costs about $600,000. The registry also includes seven Aston Martins and two Lamborghinis.

It should be noted that the “luxury tax” applies to cars costing more than UAH 3.2 million and less than 5 years old. The tax amount for one such car is UAH 25,000 per year.

https://opendatabot.ua/analytics/luxury-car-fee-2025

CAR, IMPORT, luxury, Porsche Taycan, TAX

At the same time, Ukraine reduced imports of lead and lead products by 5.2 times to $112,000 in January 2026 (in December — $478,000).

Exports of lead and lead products fell by 63.8% to $1,053 thousand (in December — $466 thousand).

At the same time, in 2025, the country increased imports of lead and lead products by 3.3 times — to $7.801 million.

Exports of lead and lead products decreased by 17.8% to $9.377 million.

At the same time, in 2024, the country increased imports of lead and lead products by 2.4 times to $2.391 million.

Exports of lead and lead products decreased by 22.9% to $11.401 million.

In 2023, compared to the previous year, less lead and lead products were imported into Ukraine — $989 thousand (-65.2%).

Exports of lead and lead products increased by 23.5% to $14.778 million.

Lead is currently mainly used in the production of lead-acid batteries for the automotive industry. In addition, lead is used in the manufacture of bullets and certain alloys.

Overall, car imports grew by 17%

According to the Ministry of Internal Affairs, almost half a million cars were imported into Ukraine from abroad in 2025. This is 17% more than in 2024, but still a third less than before the start of the full-scale war. The average age of imported cars is 9 years. One in five imported vehicles was registered in Kyiv. And one in four cars that crossed the border was electric, which is even more than the number of imported diesel cars. Volkswagen retains its leading position, and the Tesla Model Y will remain the most popular car model.

444,860 vehicles were imported into Ukraine last year. This is 17% more than in 2024, but still a third less than in 2021.

Ukraine remains a market for used cars: more than 70% of imports last year were used cars. The average age of imported vehicles remained unchanged over the year at 9 years. By comparison, in 2021, the average age of newly imported cars was 11 years.

Against this backdrop, there were also some real automotive rarities: from a 1967 Honda Monkey moped to a classic 1971 Chevrolet Corvette. Even the electric segment has its “veterans”: the oldest electric car, the Peugeot iOn, is already 15 years old.

On the eve of the return of taxes on the import of electric cars, such cars were in high demand — every fourth car that crossed the border last year. Electric cars even surpassed diesel cars in popularity: 109,309 electric cars versus 94,014 diesel cars. However, gasoline cars still lead the way with 195,059 vehicles.

It is worth noting that of the 504 luxury cars subject to the luxury tax, half were also electric. Volkswagen was the most sought-after car brand, while the Tesla Model Y was the most popular imported car of the year.

However, it is worth noting that Volkswagen leads in 20 regions. The exceptions were the Odesa region, where BMW unexpectedly took the lead, Chernihiv and Donetsk regions, where Renault took the lead, and the Kherson region, where the Spark motorcycle brand became the leader.

If we look exclusively at electric cars, the picture is even clearer — Tesla became the No. 1 brand in 22 regions of the country, yielding only to Volkswagen in the Zakarpattia region and to the Chinese BYD in the Sumy region.

Almost one in five imported vehicles was registered in the capital: 80,425 cars. Lviv region ranks second with 51,730 cars. The top five also includes Kyiv region (28,179), Dnipropetrovsk region (26,311), and Rivne region (23,608).

https://opendatabot.ua/analytics/import-cars-2025

Logistical constraints related to the war are leading to a redistribution of corn imports to the European Union in favor of alternative suppliers, with Ukraine’s share in the 2025/26 season declining significantly, according to a review by S&P Global Commodity Insights (Platts).

According to S&P Global Market Intelligence Global Trade Analytics Suite (GTAS), corn imports to the EU in the 2024/25 marketing year amounted to 18.79 million tons, compared to 19.83 million tons in 2023/24, and GTAS forecasts an increase in imports to 21 million tons in 2025/26.

S&P notes that, on average over five years, Ukraine remained the dominant supplier of corn to the EU, supplying about 9.7 million tons per year (53.5% of imports), but in the 2025/26 marketing year (July-June), the structure of supplies changed: Brazil’s share grew to 40%, the US’s share rose to 28.3%, while Ukraine’s share fell to 22.4%.

Market participants reported delays in receiving contracted Ukrainian corn, which led buyers to switch more actively to Brazil and the US. Market participants cited the EU-Mercosur trade agenda as an additional factor in choosing the origin of products.

Spain, the Netherlands, and Italy remain among the largest corn importers in the EU. According to the European Commission, Spain imported 7.2 million tons in 2024/25 MY (7.6 million tons in 2023/24), the Netherlands imported 3.3 million tons (2.6 million tons), and Italy imported 2.8 million tons (2.1 million tons).

At the same time, Spain, as a price-sensitive market, has recently switched to more competitively priced American corn, while Ukrainian corn was relatively expensive amid high demand from Turkey, the review says.

Platts price benchmarks for February 3: feed corn ex-works Tarragona (Spain) – €213/t with loading between February 3 and March 5, Ukrainian corn – $223/t FOB POC (Odessa-Pivdenny-Chernomorsk ports) with loading between March 3 and 17, Brazilian corn – $210.81/t FOB Santos with loading in August.

The record daily volume of electricity imports to Ukraine in January was 41.987 GWh, the Ministry of Energy reported on Sunday in Telegram.

“This support was made possible by the expansion of transmission capacity: in January, the power limit for imports from the EU was set at 2,450 MW, which is an absolute record since Ukraine joined the ENTSO-E network,” the ministry said.

It is noted that this helped to maintain the system and reduce the deficit amid Russian attacks and severe frosts.

As reported by Ukrainian President Volodymyr Zelenskyy, as of January 16, electricity consumption in Ukraine was 18 GW, while the capacity to provide it was “11 GW or so.”

In 2025, Ukraine increased imports of aluminum and aluminum products by 15.3% to $514.098 million. Aluminum exports grew by 22.9% to $152.919 million.

In December, imports amounted to $43.298 million, while exports amounted to $11.805 million.

This is a continuation of the growing trend: in 2024, imports had already increased by 21.7% compared to 2023.

Aluminum is widely used as a structural material. The main advantages of aluminum are its lightness, malleability, corrosion resistance, high thermal conductivity, and the non-toxicity of its compounds. In particular, these properties have made aluminum extremely popular in the manufacture of cookware, aluminum foil in the food industry, and for packaging. The first three properties have made aluminum the main raw material in the aviation and aerospace industries (recently, it has been replaced by composite materials, primarily carbon fiber). After construction and packaging production—aluminum cans and foil—the largest consumer of metal is the energy sector.

For a more detailed overview of global aluminum production from 1970 to 2024, see the video on the Experts Club YouTube channel.