Thailand is tightening controls on foreigners who attempt to circumvent the ban on direct land ownership by using Thai nominee owners or specially created companies. Authorities are moving toward systematic inspections of land transactions, corporate structures, sources of financing, and actual control over real estate.

According to market operators, special inspection committees are being established in every province of the country, comprising representatives from land authorities, the police, the tax service, and other agencies. Their task is to identify schemes in which a foreign buyer effectively controls a land plot but formally registers it in the name of a Thai individual or a company with Thai shareholders.

Legal consultants in Thailand also note that starting in 2026, controls will be tightened regarding company registration and land transactions. The Department of Business Development requires confirmation of the actual source of funds and investment declarations when establishing or amending companies, while the Department of Land Resources cross-checks corporate data against land titles.

The focus is on so-called nominee structures, where Thai citizens or companies act as nominal owners of land on behalf of a foreigner. Thai law generally prohibits foreigners from directly owning land, although foreigners may own condominium units within established quotas, enter into long-term land leases, or own a building separately from the land.

The new checks will apply not only to future transactions but also to existing arrangements. Authorities intend to analyze the source of funds, the composition of shareholders, the family and business ties of the parties, the actual use of the land, as well as signs that the Thai nominee owner has no independent economic interest in the property.

For foreign buyers, this means a sharp increase in legal risks. The use of Thai nominee shareholders or fictitious structures may lead to criminal prosecution, liquidation of the company, forced sale of the land, and loss of control over the asset. Lawyers advise investors to review old ownership structures and bring them into compliance with the law in advance.

This is particularly important for Thailand’s real estate market amid growing foreign demand. In recent years, foreign buyers—including investors from Russia, China, Europe, and the Middle East—have shown strong interest in properties in Phuket, Bangkok, Pattaya, Samui, and other tourist destinations. Part of the demand has been for villas and land plots, where legal restrictions are significantly stricter than in the apartment segment.

Tighter controls could cool some villa and land transactions, especially if they were based on informal agreements with nominal owners. At the same time, this could increase demand for more transparent formats—such as purchasing condominium units within the foreign quota, long-term land leases, officially structured investments, and projects with legally verified ownership models.

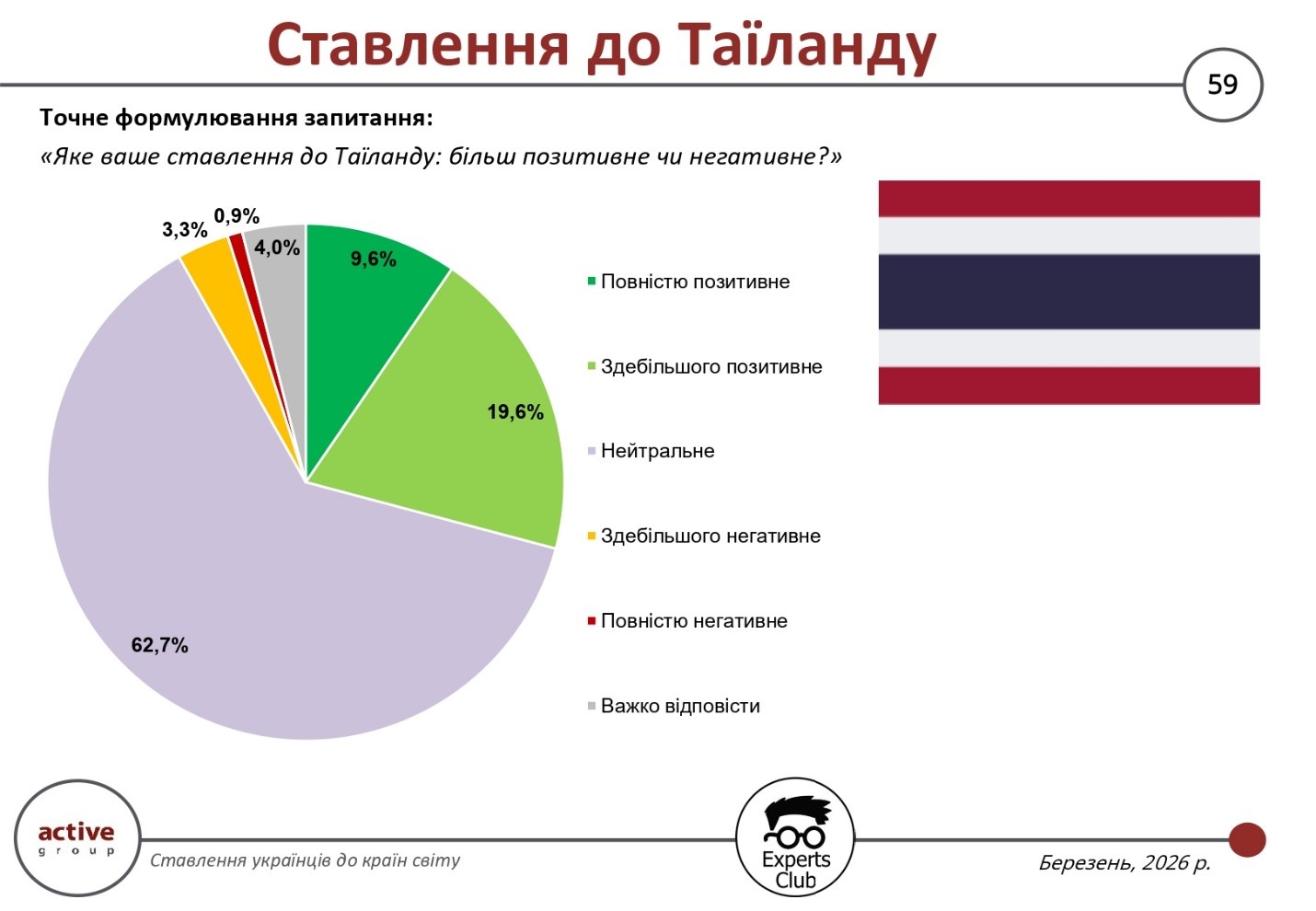

According to a survey conducted in March 2026 by the research firm Active Group in collaboration with the Experts Club information and analytical center, perceptions of Thailand within Ukrainian society are characterized by a high degree of neutrality and a moderately positive overall balance. The share of positive assessments stands at 29.2%, forming the basis of a cautiously favorable attitude; however, the dominant category is neutral responses—62.7%.

The structure of positive perceptions demonstrates that emotional engagement with Thailand is limited. Only 9.6% of respondents expressed a “completely positive” attitude, while 19.6% chose the “mostly positive” option. This indicates the presence of a generally positive backdrop, which, however, lacks a deep or lasting emotional foundation.

The key feature is the dominance of neutrality. The 62.7% figure means that for most Ukrainians, Thailand remains a country without a clearly formed image. This situation is typically associated with limited information exchange, a lack of active political or economic interaction, and the country’s weak presence in the Ukrainian media landscape.

Negative assessments are minimal—only 4.2% overall. Of these, 3.3% represent a “mostly negative” attitude and 0.9% a “completely negative” one. This indicates the absence of systemic factors shaping a negative image of the country and confirms the generally neutral-positive nature of perceptions.

Another 4.0% of respondents were undecided. Combined with the high proportion of neutral responses, this creates a significant segment of the audience that is sensitive to informational influences and potentially open to a change in attitude.

In summary, Thailand appears in the perception of Ukrainians as a country without a clearly defined emotional profile: with a low level of negativity, moderate positivity, and a dominant neutrality. This means that the country’s image in Ukraine is more of a “blank slate” that can change depending on the intensity of communication, cultural presence, and the development of bilateral contacts.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, Thailand ranks 47th in total trade volume with Ukraine, which amounts to $368.4 million. At the same time, imports from Thailand exceed exports of Ukrainian goods by more than five times, resulting in a negative bilateral trade balance of $250.6 million.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, EXPERTS CLUB, Pozniy, SOCIOLOGY, SURVEY, THAILAND, UKRAINE, URAKIN

The real estate markets of Vietnam, Thailand, Cambodia, and Bali will be in different phases of the cycle by 2026, but they share one common factor—the significant role of foreign demand. That said, the degree of dependence on foreign buyers, the supply structure, and price levels vary significantly across these markets.

Vietnam currently appears to be the most balanced of these markets. Here, the recovery is driven primarily by domestic demand, while foreigners play an important but not dominant role. In Hanoi, the average price of new apartments has already reached about $3,800 per square meter, while in the coastal city of Da Nang, the primary market stands at $2,200–2,300 per square meter. Foreigners can only purchase housing in approved commercial projects, cannot directly own land, and their share is limited by quotas, specifically to 30% of the apartments in a single condominium.

This is precisely why Vietnam remains largely a market for local buyers, while foreign demand is concentrated in the premium segment and in the largest cities. Among the key foreign groups in the market, citizens of South Korea, China, Singapore, Japan, and some overseas Vietnamese are typically cited. Russians are present mainly in resort locations, primarily in Nha Trang, while Ukrainians are also found among renters and individual buyers, but their share in publicly available statistics is not disclosed and remains niche.

Thailand, on the other hand, is much more dependent on external demand, especially in the condominium segment. According to REIC, in 2025, foreigners completed 14,899 condominium transactions, which is 2.2% more than the previous year. They accounted for 14.7% of all property transfers by volume and 25% by value. Chinese buyers retained the top spot among foreign buyers, Myanmar moved up to second place, and Russia remained among the largest groups.

In terms of prices, Thailand is significantly more expensive than Vietnam, especially in the capital and major resort areas. In Bangkok, the average price of condominiums in early 2026 was estimated at approximately $4,200–4,300 per square meter, and in central districts, the price was even higher. In Phuket, the median price of condominiums as of 2025 was about 144,000 baht per square meter, which corresponds to approximately $4,000 per square meter at the current exchange rate. The law allows foreigners to own units in condominiums but not the land, with the foreign quota in a project limited to 49% of the total area.

In Thailand, the role of foreigners is already directly influencing market dynamics in Bangkok, Pattaya, and especially Phuket. Russians remain one of the most prominent groups of buyers in resort regions, while Ukrainians, although not officially in the top 10, are considered by market estimates to be among the most active second-tier buyers and are primarily active in resort real estate.

Cambodia appears to be a riskier market, but also one more dependent on foreign capital. Following a boom and subsequent downturn, the market in Phnom Penh and Sihanoukville is recovering more slowly than in Thailand or Vietnam. In Phnom Penh, prices for condominiums in the business district are around $2,746 per square meter, and the market as a whole remains under pressure due to a high supply base and slower absorption.

The Cambodian market has historically been closely tied to Chinese capital, especially in Sihanoukville, and this dependence persists. Foreigners can purchase apartments but not land, making condominiums the primary vehicle for foreign investors. At the same time, there is virtually no comprehensive, up-to-date official breakdown of homebuyers by nationality available to the public. According to market reviews, the largest foreign groups remain the Chinese, as well as investors from South Korea, Singapore, and Malaysia. The presence of Russians and Ukrainians in this market remains limited and has no significant impact on the overall demand structure.

Bali occupies a special place among this quartet, as it is not a separate country but Indonesia’s most internationalized resort market. The driver here is not so much local demand as it is tourism, short-term rentals, digital nomads, and relocation. In 2025, Bali welcomed 6.33 million foreign tourists, a 9.7% increase from 2024, with Australia remaining the largest source market by visitor numbers.

Prices in Bali depend heavily on the property type and location. According to market surveys, the average selling price in 2025 was approximately $1,970 per square meter, and by early 2026, the average price in the villa market had risen to about $2,210 per square meter. At the same time, in the central areas of Badung, prices often exceeded $3,000 per square meter, and the average cost of villas, according to some surveys, rose from approximately $321,000 to $484,000 per property over 12 months. For foreigners, the primary option remains long-term leasehold, as direct land ownership is restricted.

Foreigners play a key role in Bali, but statistics on the nationalities of homebuyers here are less transparent than in Thailand. Based on tourism and market trends, Australians, British, Americans, and Russians are the most prominent. Since 2022, the market has also seen growing interest from Ukrainian citizens, primarily in the rental, relocation, and some investment purchase segments. However, as in Cambodia, there is no complete official breakdown by buyer nationality available to the public.

If we compare these four markets based on their market models, Vietnam currently appears to be the most internally stable and less dependent on foreigners. Thailand is the most transparent and institutionally developed market for foreign buyers, where the influence of foreign capital is already well-documented by statistics. Cambodia remains a more speculative market dependent on specific external groups. Bali, on the other hand, is a story of global mobility, tourism, and rental yields, where foreign demand effectively drives a significant portion of price dynamics.

In terms of price levels, capital cities and resorts also fall into different tiers. Bangkok and select projects in Phuket remain the most expensive in this group, followed by Hanoi. Da Nang and Phnom Penh fall within the mid-range price bracket, while in Bali the spread is particularly wide: from relatively affordable properties outside premium zones to expensive villas in Chang, Seminyak, and Bukit.

For an investor from Ukraine, this quartet looks like this: Thailand and Bali are the most straightforward markets for a resort strategy and rental income, but also the most dependent on external market conditions; Vietnam is more complex from a legal standpoint but has a strong domestic market; Cambodia is a potentially more profitable but also riskier market. At the same time, Ukrainians are already present in the Thai and Balinese markets, while in Vietnam they primarily operate as a niche group in resort locations.

Source: https://expertsclub.eu

Thailand’s real estate market in 2026 is showing steady growth, largely due to the return of foreign buyers and the recovery of tourist traffic. After a downturn during the pandemic years, the sector has once again become one of the key drivers of the country’s economy.

The main segment of demand is concentrated in Bangkok, Pattaya, and Phuket. At the same time, it is the resort regions that are of primary interest to foreign investors, who are focused on both renting and purchasing homes for their own use.

According to regulators and developers, apartment prices in Bangkok average between $3,000 and $5,500 per square meter, depending on location and project class. In resort regions, the price range is wider: in Pattaya—from $1,500 to $3,500 per square meter, in Phuket—from $2,500 to $6,000 per square meter, though premium seaside projects can significantly exceed these levels.

Thai legislation restricts foreign participation but makes the market one of the most accessible in Asia: foreigners can own units in condominiums (up to 49% of the project’s total area) but cannot directly own land. This has shaped a market model where condominiums have become the primary product for foreign buyers.

Foreigners play a key role in Thailand’s market. According to the country’s Land Department, foreigners accounted for about 13% of all condominium transactions in 2024–2025, though their share is significantly higher in certain projects and locations.

Chinese citizens remain the largest group of foreign buyers, accounting for up to 40–50% of all transactions involving foreigners. They are followed by buyers from Russia, Myanmar, India, and European countries. In recent years, Russians have consistently ranked among the top three foreign buyers, particularly in Phuket and Pattaya.

Ukrainians are also present in the Thai market, primarily in the resort real estate and rental segments; however, their share is significantly lower and remains niche.

Thus, Thailand remains one of the real estate markets in Asia most dependent on foreign demand, where foreign capital largely determines price dynamics, especially in tourist regions.

Thailand’s residential real estate market ended 2025 with a decline in the number of transactions and their value, but demand from foreigners for condominiums remained stable and partially offset the weakness of domestic buyers.

According to the Real Estate Information Center (REIC), in 2025, 316,214 transactions for the transfer of ownership of housing were registered in the country, which is 9.1% less than a year earlier, and the total value decreased by 11.8% to 864.913 billion baht.

In the fourth quarter, the authorities implemented short-term stimulus measures, reducing registration fees and easing LTV parameters for mortgages, which supported transactions at the end of the year.

REIC reports that in the fourth quarter of 2025, foreigners made 3,888 condominium purchases (year-on-year growth), and 14,899 units for the year, which is 2.2% more than in 2024. At the same time, the value of such transactions decreased by 10.7% over the year to 60.921 billion baht, indicating a shift in demand to a more affordable segment.

China remained the largest group of buyers, but its figures declined: REIC indicates that in 2025, Chinese citizens completed 4,940 transactions (about 33% of the total number of foreign transactions), while the value of these transactions decreased more significantly.

REIC published the most detailed breakdown by nationality for specific periods of 2025. According to REIC, in the first four months of 2025 (January-April), the top 10 countries by number of condominium purchases were as follows: China – 1,728, Myanmar – 566, Russia – 365, Taiwan – 225, France – 205, USA – 185, UK – 175, Germany – 144, Singapore – 103, Australia – 76.

In terms of transaction value for the same period, the top ten were: China – 7,097 million baht, Myanmar – 1,850 million, Russia – 1,246 million, Taiwan – 1,045 million, followed by the US, UK, France, Singapore, India, and Germany.

At the end of the first half of 2025, REIC reported a high concentration of transactions in Bangkok and Chonburi (more than 80%), with China, Myanmar, and Russia remaining among the leaders in terms of the number of purchases.

Separately, REIC noted the growing role of Russians and Taiwanese in the demand structure, while Ukrainian buyers did not make it into the top 10 in the REIC tables published for 2025. However, experts rank Ukrainian citizens among the top 20 most active buyers of Thai real estate.

REIC expects a scenario of “stability” for 2026 – transaction indicators may remain close to the 2025 level, without significant growth.

http://relocation.com.ua/thailands-housing-market-in-2025-supported-by-foreigners/

Thailand is considering reducing the visa-free stay period from 60 to 30 days for citizens of Russia, Ukraine, and 91 other countries, according to local media reports. The initiative is explained by the desire to close loopholes in the visa regime and reduce cases of abuse, including when visa-free entry is used for non-tourist purposes.

Under current rules, citizens of 93 countries and territories can enter Thailand without a visa for up to 60 days, with the possibility of extending their stay. This regime has been extended and has been in effect since July 15, 2024.

The Thai authorities have publicly stated that there have been cases of abuse of visa concessions and that the relevant committee must evaluate the measures and possible adjustments. As of February 11, 2026, there is no official decision on the transfer of visa-free travel to 30 days in the government announcement.

If the period is indeed reduced to 30 days for the entire list, this will also affect Ukrainian citizens.

Source: https://open4business.com.ua/tayiland-mozhe-posylyty-pravyla-bezvizovogo-perebuvannya/