This article presents key macroeconomic indicators for Ukraine and the global economy as of the end of December 2025. The analysis is based on current data from the State Statistics Service of Ukraine (SSSU), the National Bank of Ukraine (NBU), the International Monetary Fund (IMF), the World Bank, as well as leading national statistical agencies (Eurostat, BEA, NBS, ONS, TurkStat, IBGE). Maksym Urakin, Director of Development and Marketing at Interfax-Ukraine, Candidate of Economic Sciences, Doctor of Philosophy in History, and founder of the Experts Club information and analytical center, presented an overview of current macroeconomic trends that shaped the situation in Ukraine and the world at the beginning of 2026.

Ukraine’s Macroeconomic Indicators

As of the end of January 2026, the Ukrainian economy entered the new year with a combination of two opposing trends: on the one hand—a gradual easing of inflationary pressure, record-high international reserves, and a stable situation in the foreign exchange market; on the other—war risks, high budget dependence on external financing, weak exports, and a structural foreign exchange deficit in the private sector.

According to the NBU’s estimates, Ukraine’s real GDP grew by 1.8% in 2025. This meant that the economy maintained positive momentum for the third consecutive year, but the pace of recovery remained moderate. The NBU attributed this trend to resilient domestic demand, accommodative fiscal policy, business adaptability, and measures to maintain macrofinancial stability. At the same time, physical export volumes declined due to low agricultural inventories, weak external demand for mining and metallurgical products, and constraints related to the electricity shortage at the end of the year.

In January 2026, the disinflationary trend continued. According to data from the State Statistics Service (SSU), as commented on by the NBU, consumer inflation slowed to 7.4% year-on-year, while prices rose by 0.7% month-on-month. Core inflation also declined—to 7.0% y/y. The NBU attributed this trend to a reduction in labor market imbalances, the secondary effects of the high harvests of 2025, competition from certain imported goods, and a stable situation in the foreign exchange market. At the same time, the regulator noted the first signs of increasing pressure from raw food products.

According to Maksym Urakin, January 2026 became an important test for the Ukrainian economy following the conclusion of a challenging 2025. The decline in inflation to 7.4% showed that tight monetary conditions, stabilization of the foreign exchange market, and an improvement in the supply of food products had yielded results. However, in his assessment, this result should not be interpreted as a complete normalization.

“At the beginning of 2026, Ukraine experienced a rare combination for a war economy—inflation was falling, the foreign exchange market remained under control, reserves reached a historic high, and the economy did not lose its positive momentum. However, this does not mean that the country has entered a classic recovery phase. We are dealing rather with a stabilization regime in which many indicators look better thanks to external financing, budget expenditures, business adaptation, and NBU policy. If international aid were removed from this framework or a new severe energy or currency shock were to occur, the system’s stability would once again be in serious doubt,” Urakin noted.

The NBU’s January decision on the discount rate was one of the key signals of the start of the year. On January 29, 2026, the National Bank announced the start of a cycle of monetary policy easing and a reduction in the discount rate from 15.5% to 15.0% effective January 30. The regulator attributed this to a sustained decline in inflationary pressures and a reduction in risks associated with external financing. At the same time, the NBU emphasized that inflation expectations remained relatively high, and a return of inflation to the 5% target is expected only on the policy horizon.

This decision did not signify a shift to a soft monetary policy in the full sense. Real yields on hryvnia-denominated instruments remained positive, and continued interest in hryvnia assets was one of the key factors restraining demand for foreign currency. In its January Inflation Report, the NBU noted that maintaining a high rate in previous months had supported demand for hryvnia-denominated assets, and individuals’ investments in government bonds and deposits in the national currency continued to grow.

“Lowering the discount rate to 15% was a cautious and logical step, but it should not be interpreted as a signal of imminent cheapening of money. Ukraine remains in a state of war, with high budgetary needs and a significant private-sector foreign exchange deficit. Therefore, the NBU is effectively trying to navigate a very narrow corridor: on the one hand, not to stifle economic activity with excessively expensive money, and on the other, not to lose control over inflation expectations and the foreign exchange market. In such a situation, every rate cut should not be a political gesture, but the result of a real easing of risks,” Urakin emphasized.

The external sector remained the main pillar of Ukraine’s macrofinancial stability. As of the end of January 2026, Ukraine’s international reserves rose to $57.7 billion, setting a new all-time high. The NBU attributed the increase in reserves to inflows of external financing, which largely offset the National Bank’s net foreign exchange sales and the country’s foreign currency debt payments.

In its January Inflation Report, the NBU also noted that in 2025, Ukraine received $52.4 billion in international financial support, including $32.7 billion from the EU, $12.0 billion from the U.S., and $3.4 billion from Canada. At the beginning of 2026, reserves stood at $57.3 billion, equivalent to 5.8 months of future imports, and the NBU’s forecast projected an increase in international reserves to $65 billion by the end of 2026 and to $71 billion by the end of 2028.

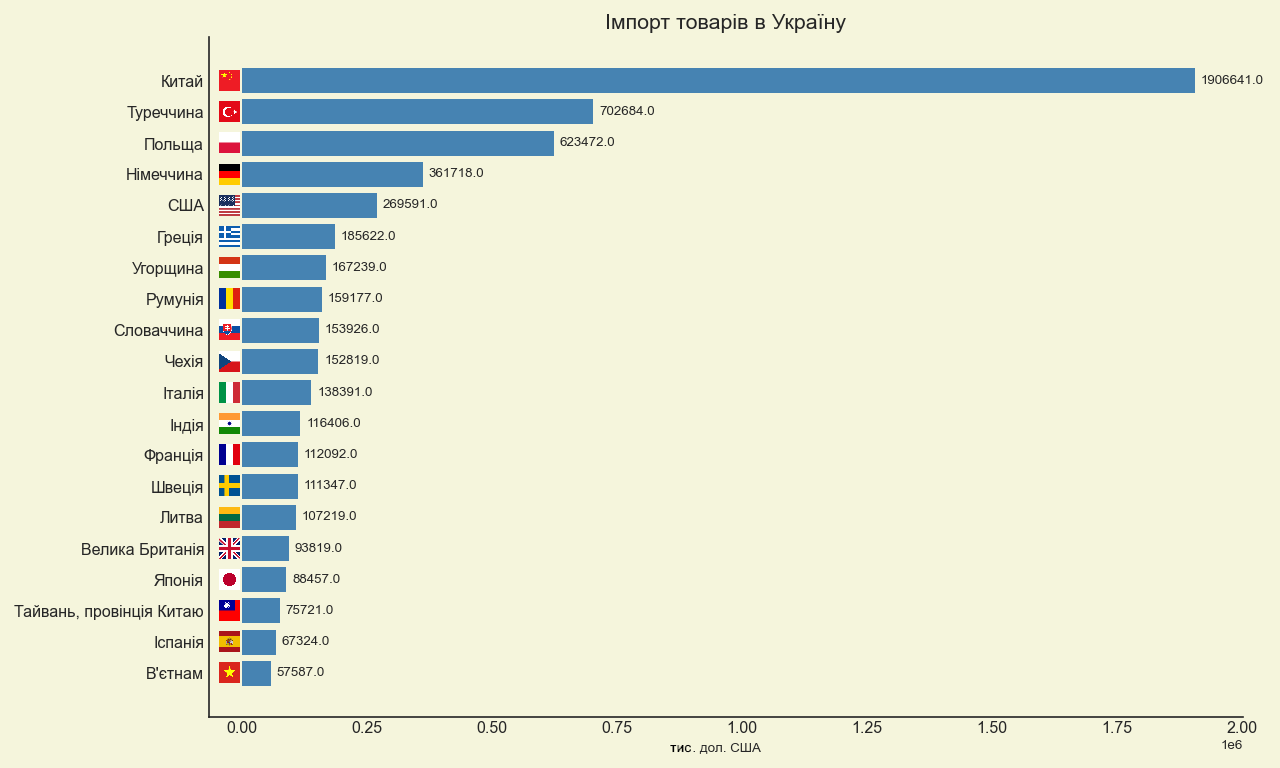

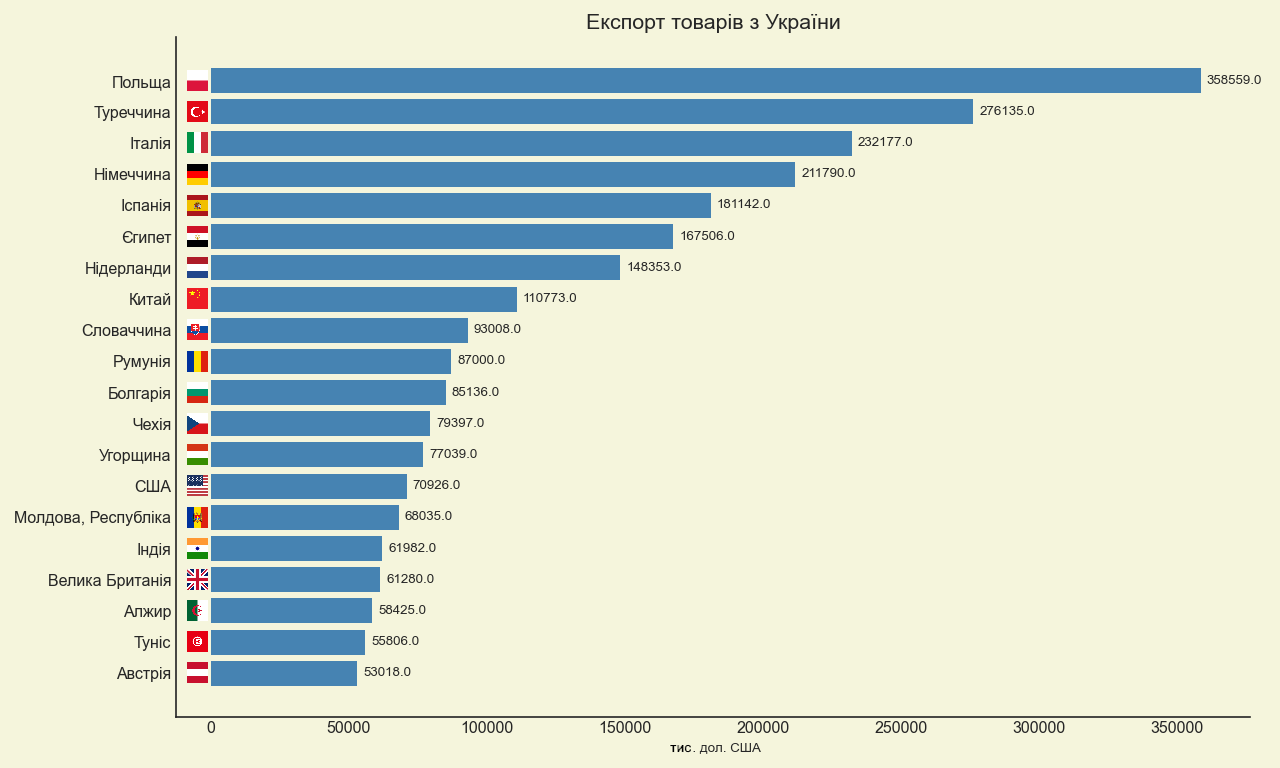

At the same time, foreign trade remained a weak point. According to customs data, Ukraine’s trade turnover in January 2026 amounted to $9.9 billion: imports – $6.7 billion, exports – $3.2 billion. This meant that the trade deficit remained high, and domestic demand for imports continued to significantly exceed foreign exchange earnings from exports.

“Record reserves are a strong stabilizing factor, but they should not create the illusion of self-sufficiency. Ukraine’s balance of payments continues to rely heavily on foreign aid rather than the economy’s export capacity. When imports more than double exports in merchandise trade, it means that the country is financing a significant portion of current consumption and military needs with external resources. This is justified in wartime, but strategically, such a model cannot be permanent. “In 2026, the key task should be to expand the country’s own foreign exchange base through exports, processing, energy resilience, and investments in production,” Urakin emphasized.

The budget situation at the beginning of 2026 also remained relatively under control, but structurally strained. According to aggregated data on budget execution, in January 2026, state budget revenues amounted to approximately 303.8 billion UAH, while expenditures totaled approximately 286.2 billion UAH. This monthly picture did not negate the overall problem of the year: public finances remained dependent on the regularity of external financing, domestic borrowing, and the government’s ability to maintain confidence in hryvnia-denominated instruments.

The Global Economy

The global economy at the end of January 2026 appeared more resilient than expected at the end of 2025, but this resilience was uneven. In its January update to the World Economic Outlook, the IMF projected global economic growth of 3.3% in 2026 and 3.2% in 2027. The Fund attributed this to investments in technology, fiscal and monetary support, more favorable financial conditions, and the resilience of the private sector. At the same time, the IMF warned of risks associated with overoptimistic expectations regarding the technology sector and a potential escalation of geopolitical tensions.

In the U.S., the economy maintained positive momentum, but the pace slowed by the end of 2025. According to a preliminary BEA estimate, U.S. real GDP grew by 1.4% year-over-year in the fourth quarter of 2025 following a stronger third quarter, and by 2.2% for the full year 2025. Growth was driven by consumer spending and investment, while exports and government spending held back the result. Inflation in the U.S. remained moderately above target: the Consumer Price Index rose by 2.7% from December 2024 to December 2025, and core CPI by 2.6%. On January 28, 2026, the Federal Reserve kept the target range for the federal funds rate at 3.5–3.75%.

The eurozone entered early 2026 with inflation nearly at target but with weak economic momentum. According to Eurostat estimates, annual inflation in the Eurozone stood at 2.0% in December 2025, down from 2.1% in November. Services inflation remained the highest component at 3.4%, while the energy component was negative. ECB rates at the start of 2026 remained at the levels set in 2025: the deposit rate at 2.0%, the main refinancing operations rate at 2.15%, and the marginal lending rate at 2.40%.

The United Kingdom remained one of the most controversial major economies in Europe. According to ONS data, the UK’s GDP grew by 1.3% in 2025, driven in part by the services sector. However, inflation accelerated to 3.4% year-on-year in December 2025, remaining significantly above the Bank of England’s target. In December 2025, the Bank of England cut its base rate to 3.75%, but the decision was passed by a narrow 5–4 majority, indicating that disagreements within the regulator regarding the pace of further easing persisted.

“The global economy at the start of 2026 did not appear to be in crisis, but it could not be described as uniformly strong. The U.S. maintained positive momentum, though no longer at an overheated pace; the eurozone was effectively balancing between low inflation and weak growth; the UK experienced slow growth but still faced elevated inflationary pressures. For Ukraine, this means that external demand is unlikely to become a powerful independent driver of recovery. The global environment tends to create moderately favorable financial conditions, but does not guarantee automatic growth in Ukrainian exports,” noted Maksym Urakin.

China ended 2025 with a formally strong result. According to data from the National Bureau of Statistics of China, the country’s GDP grew by 5.0% in 2025, reaching 140.1879 trillion yuan. The primary sector grew by 3.9%, the secondary sector by 4.5%, and the tertiary sector by 5.4%. At the same time, the inflation picture remained weak: in December 2025, the CPI rose by only 0.8% year-on-year, while core inflation rose by 1.2%. This indicated that the Chinese economy maintained its manufacturing and export strength, but domestic consumer demand remained insufficiently robust.

India, by contrast, remained the main growth driver among major economies. According to the government’s first preliminary estimate, India’s real GDP was projected to grow by 7.4% in the 2025/26 fiscal year, following 6.5% in the 2024/25 fiscal year. Nominal GDP was estimated to grow by 8.0%, with the services sector being the main driver of real GVA. At the same time, inflation remained very low: in December 2025, the CPI stood at 1.33% year-on-year, and food inflation was negative.

At the start of 2026, Turkey remained an example of an economy with relatively high growth but a challenging inflationary legacy. According to TurkStat, inflation stood at 30.89% year-on-year in December 2025 and at 30.65% in January 2026. Subsequent official data from the Turkish Ministry of Trade showed that the country’s economy grew by 3.6% in 2025 and by 3.4% year-on-year in the fourth quarter.

Brazil ended 2025 on a cautiously positive note. According to IBGE data, IPCA inflation in 2025 stood at 4.26%, while the December monthly rate was 0.33%. Brazil’s GDP in 2025 grew by 2.3%, reaching 12.7 trillion reais at current prices. Growth was observed in all three major sectors: agriculture, industry, and services.

“China, India, Turkey, and Brazil clearly demonstrate how diverse the dynamics of major emerging economies have become. China has a large scale and a strong manufacturing base, but its price momentum remains weak. India demonstrates the most compelling combination of high growth and low inflation. Turkey maintains its momentum, but the price of this growth is a very high inflation rate. Brazil is moving more moderately but more balanced. “It is important for Ukraine to view these examples not in the abstract, but practically: in global competition, the economies that win are those capable of simultaneously maintaining macro-stability, a manufacturing base, exports, and domestic investment demand,” Urakin believes.

Conclusions

As of the end of January 2026, Ukraine was in a mode of managed macrofinancial stabilization. Inflation was declining, the discount rate had been cautiously reduced to 15%, international reserves had reached a historic high, and the economy maintained positive growth after the end of 2025. At the same time, this stability remained dependent on three key conditions: regular external financing, a controlled situation in the foreign exchange market, and the state’s ability to sustain domestic demand without triggering a new wave of inflation.

The main risks for Ukraine at the start of 2026 remained war-related losses, energy infrastructure deficits, weak exports, high budgetary needs, dependence on international aid, and a structural labor shortage. A positive factor was that the NBU had record reserves and room for cautious policy easing. A negative factor was that the real production and export base had not yet created sufficient domestic resources for self-sustained recovery.

The global economy was not in a phase of deep crisis at that time. The IMF projected global growth of 3.3% in 2026; the U.S. remained stable, the eurozone stayed close to its inflation target, India demonstrated high growth rates, and China remained a large but structurally mixed source of global demand. At the same time, none of these external factors guaranteed Ukraine a rapid recovery without domestic decisions.

“January 2026 showed that Ukraine is entering the new year not from a position of economic breakthrough, but from a position of maintained manageability. This is important because, in the context of war, the very ability to control inflation, the exchange rate, budget needs, and reserves is already a significant achievement. But the next stage will be more challenging: the country needs to transition from a model of survival and stabilization to a model of productive recovery. This means investing in energy, the defense-industrial complex, processing, logistics, export-oriented industries, human capital, and technology. Without this, even record reserves and foreign aid will remain merely a financial cushion, not a source of long-term growth,” concluded Maksym Urakin.

The monthly analytical and statistical product “Economic Monitoring” is available to Interfax-Ukraine clients.

Maksym Urakin, Head of the “Economic Monitoring” project, Director of Development and Marketing at Interfax-Ukraine, Candidate of Economic Sciences, Doctor of Philosophy in History, and founder of the Experts Club information and analytical center

ECONOMY, EXPERTS_CLUB, MACROECONOMICS, MONITORING, Ukrainian_economy, URAKIN