On June 1, 2024, the Tchaikovsky National Music Academy of Ukraine hosted an artistic event dedicated to the 214th anniversary of the Argentine May Revolution and the 78th anniversary of the Day of the Italian Republic, dedicated to the Argentine composer Astor Piazzolla.

This joint project was initiated and supported by the Embassy of the Argentine Republic in Ukraine, the Embassy of Italy and the Italian Cultural Institute in Ukraine in cooperation with the Tchaikovsky National Music Academy of Ukraine.

The artistic event of the friendly states of Italy and Argentina was a great manifestation of solidarity with the Ukrainian people and a significant example of cultural diplomacy.

At the beginning of the concert, the anthems of Italy, Argentina and Ukraine were performed by the Orchestra of Folk Instruments under the direction of Honored Artist of Ukraine Andriy Ivanysh.

Ambassador Extraordinary and Plenipotentiary of the Argentine Republic to Ukraine Ms. Elena Leticia Teresa Mukusinski, Ambassador Extraordinary and Plenipotentiary of the Italian Republic to Ukraine Mr. Pier Francesco Zazzo and Acting Minister of Culture and Information Policy of Ukraine Mr. Rostyslav Karandieiev delivered welcoming speeches.

In her speech, Ambassador Extraordinary and Plenipotentiary of the Argentine Republic to Ukraine, Ms. Elena Leticia Teresa Mukusinski, elaborated on the common history of Argentina and Italy in organizing this cultural event.

Between 1847 and 1957, Argentina received about 3 million Italian immigrants and it is estimated that 60% of the population of

Argentina are of Italian descent. Argentina is the Latin American country with the largest number of Italian immigrants, ranking second in the Americas after the United States.

In addition, Argentina has the largest Italian community on its territory, followed by Germany, Switzerland, Brazil and France. 15% of Italians who have settled abroad live in Argentina.

In fact, General Manuel Belgrano, a national hero who played one of the most important roles in the process of Argentina’s independence when the First National Government was formed in May 1810 and became the creator of the Argentine flag, was the son of an Italian immigrant from the province of Imperia in the Liguria region.

The list of Argentine presidents of Italian descent is no less significant: Bartolomé Mitre, Carlos Pellegrini, Arturo Frondisi, Arturo Illia, Mauricio Macri, and our current president, Javier Milei.

And the number of famous people, artists, scientists, scholars and athletes is countless, including Pope Francis, Juan Manuel Fangio, Clorindo Testa and, among others, our dear Astor Piazzolla,” the diplomat said.

The Ambassador also expressed her deep admiration for the courage and resilience of the Ukrainian nation: “As you know, Argentina has voted against Russia’s large-scale invasion of Ukraine in all UN General Assembly resolutions and international forums. We are participating in two working groups of President Zelenskyy’s “Formula for Peace”.”

For his part, the Ambassador of the Republic of Italy to Ukraine, Pier Francesco Zazzo, noted in his speech that Astor Piazzolla “was not only considered one of the greatest composers of the twentieth century for his unique tango works, which also contains elements of jazz and classical music, but he was also a descendant of an Italian family in Argentina, and his compositions intertwine Italian roots with the Argentine soul, symbolizing the unbreakable friendship between two nations united by a passion for music and culture.”

A musical gift for the guests was a performance by the world-famous Italian bandoneon player Mario Stefano Pietrodarki accompanied by the Academy’s string quintet and orchestra of accordionists under the direction of artistic director and conductor Joseph Franz.

Maestro Pietrodarki captivated the audience with his virtuoso playing and unsurpassed style of performance, performing works by the legendary Argentine musician and composer Astor Piazzolla, as well as by no less legendary Italian composers Ennio Morricone, Nino Rota, and Niccolo Piovani.

Argentina recognized Ukraine on December 5, 1991. On January 6, 1992, Ukraine and Argentina established diplomatic relations. The Argentine Embassy in Ukraine was opened in May 1993.

Italy recognized Ukraine’s independence on December 28, 1991. Diplomatic relations with the Italian Republic were established on January 29, 1992.

The Swiss government has allocated CHF 58.7 million (EUR 60.6 million at the NBU exchange rate – IF-U) to continue supporting Ukraine in the field of digitalization and e-government over the next four years.

The decision was made by the Federal Council at a meeting on June 7, the Swiss government’s press service reports.

“Thus, Switzerland promotes democratic reforms in Ukraine through digitalization and at the same time increases the transparency of public services. Both areas are crucial for Ukraine’s recovery,” the statement said.

Switzerland will provide a total of 58.7 million Swiss francs in the period 2024-2028. The funding will come from the regular budget for international cooperation and will focus in particular on projects in regions directly affected by the war and important for the country’s future recovery. Some of the key areas will include health, education, and humanitarian demining.

It is noted that Switzerland will announce its support in the field of digitalization and e-government at the next Ukraine Recovery Conference, which will be held on June 11 and 12, 2024 in Berlin.

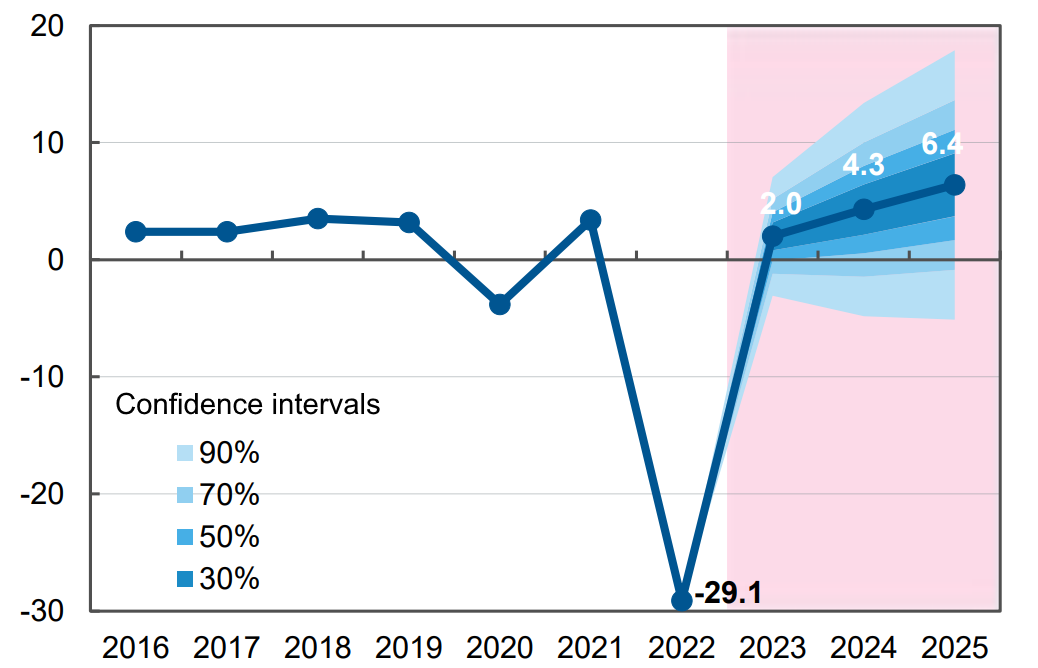

Forecast of dynamics of changes in ukrainian GDP in % for 2022-2025 in relation to previous period

Source: Open4Business.com.ua and experts.news

At the request of the Ukrainian government, Japan has provided Ukraine with a series of vehicles, the Japanese Embassy reports.

“At the request of the Ukrainian government, the Ministry of Defense of Japan and the Japan Self-Defense Forces provided Ukraine with a series of vehicles under a decision made in May 2023. The batch of 101 vehicles arrived in Poland on June 5 and was then handed over to Ukraine,” the X social media post reads.

The embassy emphasized that Japan would continue to support Ukraine.

In turn, the Ministry of Defense in X expressed gratitude to Japan for its support and informed that the aid includes Toyota HMV and Mitsubishi Type 73 Kogata SUVs, as well as PC-065B tracked engineering vehicles.

Since the full-scale invasion, the Pokrovske community has become a real humanitarian hub, receiving various types of assistance from representatives of both Ukrainian organizations and international foundations on a daily basis. All of them are united by a common goal – to help civilians in confronting the enemy.

An equally important component of this cooperation is the openness to interaction of the Pokrovske MCA leaders, who work daily to “cover” all the needs of the community.

Recently, the town was visited by representatives of the Volunteer Coordination Headquarters (Kyiv), a charity organization that works closely with European countries on humanitarian aid.

“The winner is the one who destroys the enemy’s strategic plan. Therefore, all attention is focused on Donetsk region, because it is the “most important” region. Since 2022, we have been actively helping our defenders and the frontline communities of Donetsk Oblast, whose residents suffer from shelling every day,” said Oleksandr Kuzniak, the foundation’s chairman.

During the visit to Pokrovsk, the volunteer philanthropists met with the heads of the military administration, including Natalia Ivanio, deputy head of the Pokrovsk MVA, and discussed the needs of the community.

They brought power tools that will be useful for the city’s utility workers.

“We come to Donetsk region at least once a month. We form a truck with humanitarian cargo according to the needs that the military and community leaders send us. This is not the first time we have been in Pokrovsk, and we are working closely with Sergey Dobryak, who is always open to cooperation, especially in humanitarian issues. We plan to continue to support the Pokrovsk community, which is located in close proximity to the front line. It is extremely important today,” added Mr. Kuzniak.

In her turn, Natalia Ivanio, Deputy Head of the Pokrovske MVA, thanked the benefactors for their help and active social position.