In October 2025, Ukrainian metallurgical companies increased steel production by 7.3% compared to October 2024, from 604,000 tons to 648,000 tons, but reduced it by 5.9% compared to September 2025 (689 thousand tons), according to data from the World Steel Association (Worldsteel).

According to the association’s report, Ukraine ranked 21st among 70 steel-producing countries in October.

In January-October 2025, Ukrainian steel companies produced 6.172 million tons of steel, which is 4.9% less than in the same period of 2024 (6.487 million tons). Ukraine ranks 22nd in the world in terms of this indicator.

In 2024, Ukraine produced 7.575 million tons of steel, increasing production by 21.6% compared to 2023 (6.228 million tons) and ranked 20th among 71 countries. In 2023, steel production in the country decreased by 0.6% compared to 2022, to 6.228 million tons, and Ukraine ranked 22nd in the global ranking.

At the end of 2022, Ukraine produced 6.263 million tons of steel, which is 70.7% less than in 2021, and ranked 23rd among 64 countries covered by Worldsteel.

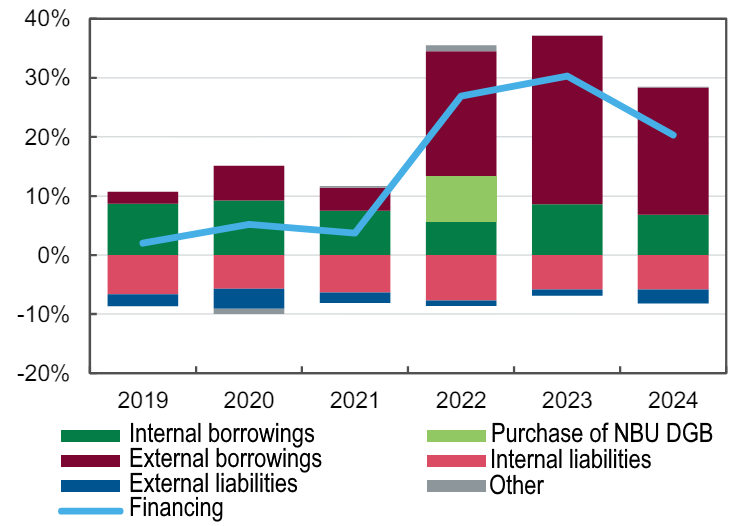

Earlier, the Experts Club analytical center released a video analysis of the world’s leading steel producers from 2001 to 2024 – https://youtube.com/shorts/VgUU9MEMosE?si=c5yD04gmNtJoFblB

Ingulets Mining and Processing Plant (Ingulets, Kryvyi Rih, Dnipropetrovsk region), part of the Metinvest Group, increased its net loss by 14.8 times to UAH 1 billion 489.657 million in January-September this year, compared to UAH 100.479 million in the same period last year.

According to the company’s interim report, which is available to the Interfax-Ukraine agency, the loss in the third quarter amounted to UAH 631.343 million.

In the first nine months of this year, the company’s revenue fell sharply due to downtime, to UAH 25.453 million from UAH 7 billion 793.635 million.

Undistributed profit at the end of September 2025 amounted to UAH 12 billion 200.491 million.

The main factors influencing this were restrictions on demand, including due to the loss of metallurgical plants in eastern Ukraine, logistical complications, a decline in sales prices, and the suspension of the concentrate production cycle in the second half of 2024 due to the lack of organizational and technical conditions for the company’s economic activities in wartime.

There was no commercial concentrate production in the first nine months of 2025. In the second quarter of 2025, the technological process was partially resumed as part of ore mining for shipment to the Central Mining and Processing Plant. In the third quarter of 2025, the work was extended.

Ore production for the first nine months of 2025 amounted to 86,745 thousand tons.

Ingulets GOK ended 2024 with a net loss of UAH 1 billion 317.997 million, compared to UAH 167.236 million in 2023. The plant ended 2022 with a net loss of UAH 851.259 million, while in 2021 it received UAH 20 billion 446.101 million in net profit. In 2020, Ingulets GOK reduced its net profit by 75.3% compared to the previous year, to UAH 1.5 billion.

The company specializes in the extraction and processing of iron-bearing quartzites from the Ingulets deposit, located in the southern part of the Kryvyi Rih iron ore basin. It produces iron ore concentrate. The company’s production capacity is 14 million tons of iron ore concentrate per year.

Metіnvest B.V. (Netherlands) owns 100% of the shares of PJSC “Ingulets GOK”.

The authorized capital of PJSC “Ingulets GOK” is UAH 689.906 million, with a share par value of UAH 0.25.

Ingulets GOK is part of the Metinvest Group, whose main shareholders are PJSC System Capital Management (SCM, Donetsk, 71.24%) and the Smart Holding group of companies (23.76%). The managing company of the Metinvest Group is Metinvest Holding LLC.

Almost all member companies of the European Business Association (EBA) complain about a shortage of personnel: 74% consider this problem to be significant, 21% report a partial shortage, and only 5% did not experience a shortage of personnel in 2025, according to a study of the Ukrainian labor market by the EBA.

“It is most difficult to fill vacancies for workers and technical specialists due to staff turnover and low motivation to work offline. There is also an acute shortage of narrow-profile specialists with knowledge of English, who are needed by international companies,” according to the results of the study published by the association’s press service.

It is emphasized that, in addition to them, it is difficult to find sales managers and middle managers, as their work requires constant presence, and booking opportunities are limited.

In addition, 46% of companies noted that the departure of young professionals aged 18-22 had a definite or significant impact on their activities. 42% did not feel any impact, while 12% noted that they did not yet have enough data to assess the situation.

In addition to the labor shortage, key trends in the labor market include inflated salary expectations on the part of candidates, the impact of mobilization, difficulties in booking workers, and staff turnover.

Among the companies surveyed, 46% noted that all employees are currently working from within Ukraine, compared to 35% of companies last year. At the same time, 47% have up to 10% of employees working from abroad, and only 5% of companies have more than 10% of such employees. The rest (approximately 2%) do not have accurate information.

Most employers (63%) do not plan to require employees to return to the office in the near future, 37% are considering this possibility, but 12% of them do not plan to bring back all categories of employees.

As for companies’ plans, most have a clear vision for development in 2026.

“The main focus of business is on increasing salary levels – this is planned by 94% of companies. In particular, 28% of companies anticipate growth in the range of 11-15%, 23% – 5-10%, 10% expect growth of 16-20%, and 6% of companies do not intend to raise salaries in 2026,” according to the EBA.

As for other plans, 36% intend to increase the number of employees next year, 55% do not plan any changes, and 9% plan to reduce their workforce. 17% of companies reported a redistribution of functions towards multifunctionality.

During 2025, most companies (83%) actively recruited new employees. Another 3% opened vacancies exclusively for internal candidates, and only 14% of respondents did not change their headcount.

In addition, 25% are planning to increase their budgets for staff training and development, 18% of respondents are planning to enter new markets and search for partners, 6% may change management or open new regional offices, 5% will reduce training costs in 2026, and 3% are planning to close offices.

The survey was conducted from October 2 to November 1, 2025, with 126 human resources professionals participating (41% department heads, 33% middle managers, 22% top management, and 4% junior staff). Among the respondents, 56% represent large businesses, 32% represent medium-sized businesses, and 12% represent small businesses. 58% of companies are international, and 42% are Ukrainian.

PJSC Centravіs Production Ukraine (Nikopol, Dnipropetrovsk region), part of the Centravіs Ltd. holding, reduced its net profit by 2.5 times compared to the same period last year, to UAH 158.111 million from UAH 398.888 million, based on the results of its operations in January-September of this year.

According to the company’s interim report, which is available to Interfax-Ukraine, the company increased its net income by 1.4% to UAH 3 billion 961.714 million in the first nine months of this year.

The uncovered loss at the end of September 2025 amounted to UAH 888.623 million.

In order to ensure the necessary volume of pipe billets, the company diversifies its purchases by purchasing pipe billets from foreign manufacturers. About 70% of pipe billets are purchased abroad. The company continues to cooperate with Ukrainian pipe billet manufacturers, whose production facilities are located in the Dnipropetrovsk and Zaporizhzhia regions.

In the first nine months of 2025, the company produced 9,974 thousand tons of pipes.

The company is export-oriented, with exports accounting for 96% of sales in the first nine months of 2025. The largest markets for its products are Germany, Italy, and the United States. In addition, pipe products are also sold in the Middle East, Asia, and Australia. In the first nine months of 2025, 9,919 thousand tons of pipes were sold, of which 9.9 thousand tons were exported.

An additional incentive for the company’s pipe exports is the temporary measures to liberalize trade and abolish customs tariffs and quotas by European countries and the US. In particular, in 2023, the EU and the US extended the suspension of customs tariffs and quotas on Ukrainian goods exported to European and American markets until June 1, 2024. In May 2024, this suspension was extended until June 5, 2025.

The company constantly monitors liquidity and credit portfolio management. The company pays all current loan payments in accordance with the repayment terms specified in the current agreements. On April 15, 2025, the company signed an agreement with its main creditor, Ukreximbank, on the long-term restructuring of its loan portfolio, namely the extension of long-term lines of €19,369,180 and $3,740,450 until February 22, 2031 (before the signing, the term was until February 22, 2026), and a short-term line of EUR 9 million was extended until March 3, 2028 (before the signing, only short-term extensions were carried out). This event has a significant positive impact on the company’s liquidity and solvency, allowing it to reduce its current debt burden and ensure stable cash flows.

In addition, to meet the company’s operational needs, on May 5, 2025, a general credit agreement was signed with the commercial bank Pivdenny for a total amount of short-term lending of UAH 50 million secured by a VAT declaration, which allowed the company to optimize cash flows and improve working capital. In July 2025, the company entered into an additional agreement with the bank to reduce the interest rate on short-term loans in national currency from 19% to 18% per annum, which has a positive impact on liquidity indicators.

As of September 30, 2025, the company applied for a VAT refund in the amount of UAH 57.834 million (as of December 31, 2024 – UAH 83.925 million), which was received from the state budget after the reporting date. Based on the results of the audits, the tax authorities did not confirm the VAT refund in the total amount of UAH 23.806 million. The company is challenging the results of the VAT audit in court.

In 2024, the company received a net profit of UAH 310.045 million, while it ended 2023 with a loss of UAH 384.664 million. At the same time, it increased its net income by 3.7% to UAH 5 billion 226.606 million. The company produced 14,017 thousand tons of pipes (in 2023 – 12,412 thousand tons), with exports accounting for 90.1% in 2024.

With regard to environmental protection, the board of directors considered issues related to reducing the harmfulness of production by improving production technologies, in particular, the transition to azote-free pipe pickling. In accordance with the requirements of Directive 2003/87/EC, a decision was made to implement a system for monitoring, reporting, and verifying greenhouse gas emissions and quarterly CBAM reporting.

According to the report, the profit in the current and previous reporting periods was mainly due to the forgiveness of debt on accrued interest under a loan agreement with a related non-resident entity, Centravis Finance Ltd.

On September 24, 2025, the sole shareholder of the company, Centravis SA (Switzerland), decided to increase the authorized capital by issuing additional shares worth UAH 4,335,171 thousand without a public offering.

The shares were valued by Uvecon Consulting Company LLC. Participants in the share placement must submit an application for the purchase of shares to the authorized person between February 28 and April 28, 2026.

Sentravis was founded in 2000 and is one of the ten largest manufacturers of seamless stainless steel pipes in the world. Its main production facilities are located in Nikopol (Dnipropetrovsk region). In 2023, a branch of the company was opened in Uzhhorod.

The company’s main activity is the production and sale of seamless stainless steel pipes. As of September 30, 2025, the company employed 1,428 people (as of September 30, 2024, 1,541 people).

Centravіs Ltd. was established on the basis of Nikopol Stainless Steel Pipe Plant CJSC and the service and trading companies of YUVIS Production and Commercial Enterprise LLC. Its shareholders are members of the Atanasov family. Centravis Ltd. owns 100% of the shares of PJSC “Centravis Production Ukraine.”

According to the NDU for the third quarter of 2025, Centravis SA (Centravis AG) (Centravis Ltd) (Switzerland) owns 100% of the shares of PJSC “Centravis Production Ukraine”.

According to the company’s information, as of September 30, 2025, the ultimate beneficial owners of the company are Yuriy Atanasov, who owns 66.7% of the shares, Konstantin Atanasov with 16.65%, and Kateryna Atanasova-Milovanova with 16.65%. The 6,668 shares in the authorized capital of UVIS Group Limited, which belonged to Vasyl Atanasov, who died on September 18, 2023, were inherited by Yuriy Atanasov.

The authorized capital currently amounts to UAH 202.560 million, with a nominal value of UAH 1 per share.

The first dealership center of the new premium brand of electric and hybrid cars Avatr, which enters the Ukrainian market, was opened on Stolichnoye highway in Kiev by the official distributor of the new brand – Atlant Motors Ukraine LLC (part of the Atlant Motors group of companies), the press service of the company reported.

The official presentation of the brand took place on November 20. “Atlant Motors Ukraine” will provide a full cycle – from car sales to service, warranty of the manufacturer and sale of original spare parts.

“Atlant Motors Ukraine” informs about plans to expand the network of official dealer centers in different regions of Ukraine. In particular, by the end of this year there will be official dealers in Odessa, Kiev, Kharkov, and in 2026 AVATR brand showrooms will be opened in Lviv and Dnipro.

At the official opening three models of the brand were presented, in particular Avatr 07 – urban mid-size hybrid or electric SUV. The car is offered in two variants: all-electric (BEV) and series hybrid (REEV). The REEV version is equipped with a hybrid setup based on a 1.5-liter turbo engine and electric motors with a total output of up to 492 hp.

Atlant Motors Group of Companies has been operating in the Ukrainian market for more than 20 years and represents, in particular, the Renault brand in Kharkov and Kharkov region. The group also includes Atlant Motors Energy (Kharkiv) – one of the largest suppliers of electric cars from China to Ukraine, which, according to YouControl data, has net income of UAH 619.9 million in 2024 and UAH 1.28 billion in January-September 2025.