The debt of the Ukrainian population for housing and communal services in the second quarter of 2025 amounted to UAH 106.645 billion.

According to data from the State Statistics Service (SSS), Ukrainians paid a total of UAH 64.341 billion for housing and communal services in April-June 2025, which is 25% more than the amount charged – UAH 51.46 billion.

The debt for the reporting period for the supply of heat and hot water amounts to UAH 35.165 billion, the supply and distribution of natural gas – UAH 32.321 billion, the supply of electricity – UAH 17.066 billion, centralized water supply and sanitation – UAH 10.155 billion, management of apartment buildings – UAH 8.836 billion, and household waste management – UAH 3.101 billion.

The highest level of debt for housing services was recorded in Dnipropetrovsk (UAH 8.699 billion), Donetsk (UAH 4.308 billion), Poltava (UAH 3.303 billion), Kyiv (UAH 2.031 billion), Kharkiv (UAH 1.521 billion), Odesa (UAH 1.48 billion), Lviv (UAH 1.09 billion) regions and Kyiv (UAH 2.342 billion).

The data does not include territories temporarily occupied by the Russian Federation and parts of territories where hostilities are (were) ongoing.

Indebtedness of the population of Ukraine on payment for housing and communal services in the second quarter of 2025 amounted to 106.645 billion UAH.

According to the State Statistics Service (Gosstat), in April-June 2025 Ukrainians paid a total of UAH 64.341 billion for housing and communal services, which is 25% more than the accrued amount of UAH 51.46 billion.

The arrears for the reporting period for heat and hot water supply amount to UAH 35.165 billion, natural gas supply and distribution – UAH 32.321 billion, electricity supply – UAH 17.066 billion, centralized water supply and drainage – UAH 10.155 billion, apartment building management – UAH 8.836 billion, household waste management – UAH 3.101 billion.

The highest level of arrears for housing services was recorded in Dnipropetrovsk (UAH 8.699 billion), Donetsk (UAH 4.308 billion), Poltava (UAH 3.303 billion), Kyiv (UAH 2.031 billion), Kharkiv (UAH 1.521 billion), Odessa (UAH 1.48 billion), Lviv (UAH 1.09 billion) regions and Kyiv (UAH 2.342 billion).

The data are given without taking into account the territories temporarily occupied by the Russian Federation and part of the territories where hostilities are (were) being (were) conducted.

The International Monetary Fund’s four-year extended EFF financing program for Ukraine also envisions the country receiving $80 billion from multilateral and bilateral donors during this period, including $20 billion in grants and $60 billion in concessional loans, as well as another $20 billion in debt flow relief, said Gavin Gray, head of the Fund mission.

At a press conference on Friday, after announcing the decision to approve the $15.6 billion EFF program, he recalled two announcements made last week: from a group of official Ukrainian creditors about their willingness to defer the country’s debt payments for the program period and about Ukraine’s intention to agree the same with the holders of Eurobonds and other external commercial debts.

A draft law on writing off debts on consumer loans granted for the purchase of movable and immovable property that was destroyed by the war will be submitted to the Verkhovna Rada within a week, Danila Getmantsev, head of the relevant parliamentary committee, said.

“On behalf of the president, we agreed with the head of the National Bank and the prime minister on the development of a bill to write off debt on consumer loans for the purchase of movable and immovable property that was destroyed during the hostilities. We will submit the bill to VR within the next week,” he wrote in a telegram on Sunday.

“A person should not pay a debt for a non-existent object,” Getmantsev added.

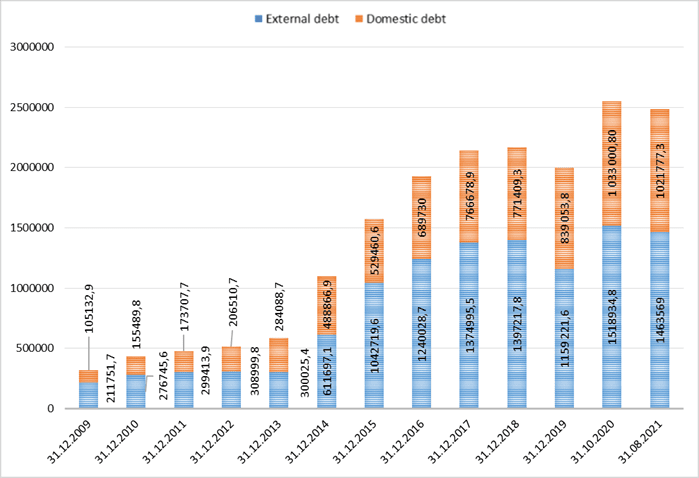

INTERNAL AND EXTERNAL DEBT OF UKRAINE IN 2009-2021

The arrears of the population of Ukraine on payment for housing and communal services decreased by 7.6% in May 2021 versus April and amounted to UAH 61.6 billion (excluding electricity).

According to the State Statistics Service, in general, in May, Ukrainians paid UAH 17.1 billion for housing services, which amounted to 146.2% of the amount charged for that month.

The debt for the supplied electricity in May amounted to UAH 7.3 billion.

The highest level of payment for housing services was recorded in Ternopil (177.9% of the amount accrued, due to the repayment of debts of previous periods), Cherkasy (153.9%), Donetsk (153.4%) regions and Kyiv (170.3%).

The lowest level of payment is in Kirovograd, Volyn and Kherson regions (113% to 120% of the amount of charges).

According to the State Statistics Service, from the beginning of 2021, some 22,700 agreements have been concluded with the population on the repayment of restructured debt for housing services for a total of UAH 187.1 million. The amount of payments made, taking into account long-term contracts, amounted to UAH 106.2 million.