Most Swiss are willing to support an initiative to cap the country’s population at 10 million by 2050, a move that could impact Switzerland’s immigration policy, labor market, and real estate market, according to local media reports.

According to a poll conducted six weeks before the nationwide referendum scheduled for June 14, 2026, 52% of respondents supported the initiative or were inclined to support it, 46% opposed it, and another 2% were undecided. Over 16,000 people participated in the survey.

The “No to 10 Million in Switzerland!” initiative is being promoted by the Swiss People’s Party (SVP). It stipulates that the country’s permanent population should not exceed 10 million people by 2050. Upon reaching an interim threshold of 9.5 million people, the government would be required to implement additional measures to limit immigration, including potentially tightening quotas on work visas and asylum applications. Reuters notes that the proposal also calls for Switzerland to withdraw from the EU agreement on the free movement of citizens.

Supporters of the initiative link the need to limit population growth to the strain on infrastructure, housing shortages, overcrowded public transportation, and rising costs for social and medical services.

The Federal Council and both chambers of parliament recommend rejecting the initiative. Authorities warn that strict restrictions on migration could create legal uncertainty, complicate relations with the European Union, and exacerbate the labor shortage in the economy. Reuters also notes that Switzerland’s population already exceeds 9 million, and the share of foreigners stood at over 27% in 2024.

For the real estate market, the possible adoption of the initiative could have a dual effect. On the one hand, limiting population growth could theoretically reduce long-term pressure on housing demand. On the other hand, stricter immigration rules and a potential reevaluation of relations with the EU could affect Switzerland’s investment appeal, the availability of labor in the construction and service sectors, as well as demand from foreign residents.

According to data from the Swiss State Secretariat for Migration, as of the end of 2024, the largest groups of the country’s permanent foreign population were citizens of Italy—346,981 thousand people, Germany—332,132 thousand, Portugal—263,028, and France—173,353. In total, 1.579 million citizens of EU/EFTA countries and 789,735 citizens of third countries resided permanently in Switzerland.

Ukrainians occupy a distinct place in Switzerland’s migration statistics following the outbreak of full-scale war. According to SEM data, in 2024 the number of individuals with active S protection status rose to 68,070 compared to 66,083 the previous year. This figure can be used as a rough estimate of the number of Ukrainian refugees in the country, although the actual number of Ukrainians in Switzerland may differ due to people holding other types of residence permits.

Ukrainians purchased approximately 6,200 new passenger cars in April 2026, which is 3% more than in April 2025 and 5% more than in March of this year, according to a report by Ukravtoprom on its Telegram channel.

Toyota remains the most popular brand with 750 units sold, which is 7% more than in April 2025 but 17.4% less than sales in March 2025.

Renault took second place with a 19% increase in sales compared to April of last year and a 25.6% increase compared to March of this year, reaching 653 units.

Skoda took third place with an 18% drop in sales compared to April 2025 and a slight decline compared to March 2026, totaling 450 units.

The Chinese brand BYD (one of the sales leaders in the final months of 2025, which had dropped out of the top ten by early 2026) climbed to fourth place from tenth in March of this year—448 units (+53% compared to April of last year).

Next were BMW – 442 units (+45%), Volkswagen – 412 units (-23%), Hyundai – 337 units (+17%), Mazda – 244 units (+230%), Nissan – 216 units (-3%), and Suzuki – 188 units (-30%).

The best-selling model of the month was the Renault Duster compact crossover.

According to Ukravtoprom, over 21,500 new passenger cars were sold in the country from January to April, which is 7% more than last year.

Meanwhile, the information and analytical group AUTO-Consulting reports that the new passenger car market in April totaled 6,170 vehicles, which is 3.8% more than in March and 0.8% more than in April of last year.

“Thus, the Ukrainian auto market continues to move in positive territory and demonstrate positive trends. There is also active competition,” the group’s website states.

According to experts, the top three were also led by Toyota (799 units), Renault (604 units), and Skoda (450 units), followed by BMW (445 units) and BYD (433 units).

“BYD continues to surprise this season. In April, it was already No. 5 on the Ukrainian market again (growth of +123%), following a sharp drop in electric car sales. Nevertheless, BYD is recovering its sales volumes and is even establishing a dealer network across Ukraine,” the post states.

According to information on the website of “BB Cars” (Kyiv region), which was registered in November 2022 in the Bucha district, in March 2026, it announced the signing of an exclusive strategic cooperation agreement with the Chinese company Beijing North Huapeng Materials Sales Co. regarding the development of BYD vehicle distribution in Ukraine.

AUTO-Consulting also notes that another trend in April was a significant increase in Citroën sales (11th place compared to 18th in March and a 50% increase)

At the same time, among the negative results, they note that Mercedes-Benz lost significant ground in April (-22.5% compared to March 2026, down to 117 units).

“But there are objective reasons for this, as one of the Mercedes-Benz dealerships in Kyiv was hit by rocket fire in April, resulting in many cars being burned. Therefore, unfortunately, Mercedes-Benz found itself in a difficult situation,” the post notes.

As reported, according to AUTO-Consulting, Ukrainians purchased 83,443 new passenger cars in 2025, which is 17% more than the previous year, and according to “Ukravtoprom,” the market also grew by 17%—to 81,300 units.

According to its annual report, the Astarta agricultural holding achieved a gross harvest of grain and oilseed crops of approximately 0.6 million tons in 2025, matching the previous year’s result.

“Climate instability, logistical constraints, and rising costs prompted the Company to increase acreage for crops with predictable sales and stable economics, such as corn and sunflower. However, unfavorable weather put significant pressure on crops, reducing productivity,” the company’s report noted.

The holding revised its crop rotation structure in response to climatic and logistical factors. Corn acreage more than doubled—to 12,000 hectares—resulting in a harvest of 94,000 tons of grain (+134% compared to 2024), while sunflower production increased by 32%—to 61,000 tons.

The soybean harvest decreased by 27%—to 122,000 tons (including the 2026 harvest), and the rapeseed harvest by 23%—to 31,000 tons due to weather anomalies. The sugar beet harvest amounted to 1.8 million tons, which is only 2% less than the previous year thanks to a 12.2% increase in yield, which almost completely offset the 13% reduction in acreage. Wheat production fell by 9% to 237,000 tons amid a reduction in acreage and a slight decline in productivity.

Yields for the holding’s main crops generally exceeded the national average. The yield for corn was 7.6 t/ha compared to 7.2 t/ha nationwide, and for wheat, 5.2 t/ha compared to 4.5 t/ha. A gap was also recorded for sunflowers—2.1 t/ha versus 1.9 t/ha—and rapeseed—2.8 t/ha versus 2.7 t/ha—while sugar beet yields stood at 55 t/ha.

In 2026, Astarta plans to expand its corn acreage by 66%, to 20,000 ha, and increase winter rapeseed acreage by 36%, to 15,000 ha, compared to last year. A reduction in acreage is expected for sunflowers by 20% to 23,000 ha, wheat by 15% to 39,000 ha, and sugar beets by 6% to 32,000 ha. The area under soybeans will remain stable at 56,000 hectares, which is 1.7 times less than the peak figure of 70,000 hectares in 2024.

“The condition of winter crops is generally satisfactory, as the insulating snow cover protects the plants from severe cold. Significant moisture reserves also create the potential for higher yields of spring crops,“ the agricultural holding noted.

”Astarta” is a vertically integrated agro-industrial holding operating in seven regions of Ukraine and is the country’s largest sugar producer. The company’s portfolio includes five sugar refineries, agricultural enterprises with a land bank of 214,000 hectares (including 129,000 hectares in Poltava, 42,000 hectares in Khmelnytskyi, and 16,000 hectares in Vinnytsia regions) and dairy farms with 30,000 head of cattle. The holding also operates a soybean processing plant and a bioenergy complex in Poltava Oblast, as well as a network of six grain elevators.

Astarta’s net profit for 2025 fell 4.2-fold to $19.94 million, while consolidated revenue decreased by 23% to $472 million. The agriholding’s EBITDA fell by 37% to $100 million, with a margin of 21%. The company’s net debt doubled over the past year and stood at $226 million at the end of the period.

PZU SA Group has signed a preliminary agreement to acquire 100% of the shares in MetLife Ukraine—the leader of the Ukrainian life insurance market—according to a statement from PZU Ukraine Insurance Company.

It is emphasized that the deal strengthens the PZU Group’s position in Central and Eastern Europe, expands its operations in the life insurance segment, and aligns with its strategy to become a regional leader.

“The acquisition of MetLife Ukraine is an important step in the implementation of our long-term strategy to build a strong international insurance and financial group in Central and Eastern Europe. We are investing in a market leader with an experienced team and a sustainable business model, which strengthens our presence in Ukraine and significantly expands the scale of our operations in the life insurance segment. This decision combines strategic ambitions with solid business fundamentals,” noted PZU CEO Bohdan Benchak.

Furthermore, this aligns with the Group’s strategy of expansion in Central and Eastern Europe, particularly in markets where it already has an established presence. The Ukrainian life insurance market remains relatively underdeveloped compared to other countries in the region, creating significant opportunities for further growth.

From a financial perspective, this transaction is also attractive for the PZU Group. MetLife Ukraine has a strong capital position, high profitability (approximately 20% ROE), and liquidity, which creates potential for dividend payments.

“For PZU Ukraine, the acquisition means a significant increase in scale, access to a sales network that complements PZU Ukraine’s existing network, expanded product capabilities, and an experienced team with a broad customer base,” the statement reads.

According to the information, the PZU Group has responsibly and proactively assessed the risks associated with investing in a country currently in a state of armed conflict. The investment is insured by KUKE (PFR Group), which provides protection against the negative consequences of a potential deterioration in the military or political situation.

“The PZU transaction is yet another foreign investment by a Polish entity in Ukraine that was guaranteed by KUKE this year. The absence of political and force majeure risks, particularly those related to military actions, creates potential for the safe development of our companies,” noted Janusz Władczak, President of KUKE.

Macroeconomic data indicate a high level of resilience in the Ukrainian economy, a gradual stabilization of inflation, and prospects for moderate GDP growth in the medium term, the statement emphasizes.

As previously reported, MetLife Ukraine is part of the leading global corporation MetLife. It has been operating in Ukraine since 2002 and is the leader in the Ukrainian life insurance market.

In the face of widespread destruction of infrastructure and housing stock resulting from military aggression, the use of prefabricated construction technologies is one of the key tools for Ukraine’s reconstruction.

As noted in a market study on prefabricated construction in Ukraine, conducted jointly by Helvetas and the Housing Institute, an analysis of the sector revealed both significant opportunities and substantial barriers to its development. Ukraine’s construction sector is showing signs of recovery following a critical downturn in 2022, when construction volumes fell by 56%. Prefabricated construction technologies are becoming particularly relevant due to shorter construction timelines, energy efficiency, structural mobility, and reduced dependence on logistical and seasonal factors.

There are over 300 companies operating in the prefabricated construction sector in Ukraine, about 3% of which have foreign investment. The market is dominated by prefabricated buildings on metal and wooden frames, as well as modular solutions.

Most market operators are located in the Kyiv (142 legal entities), Lviv (27), Odesa (17), Dnipropetrovsk (17), and Kharkiv (15) regions. Construction using prefabricated technology is the primary activity for 77% of manufacturers; 23% are companies that produce construction materials and focus their efforts on sales rather than on building construction.

At the same time, operators in the western regions of Ukraine are more focused on the production of wooden-frame houses in the private residential sector, as well as on the production/construction of hotel infrastructure facilities. Companies in the central and eastern parts of the country work with various technologies and implement projects of different purposes and scales.

The study identified a significant share of the shadow economy: in the modular production segment, market operators estimate it at 30%, and in the frame construction sector—up to 80% (influenced by the specific technology used to build private properties and cash transactions).

Exports of modular homes from Ukraine significantly exceed imports, indicating the competitiveness of domestic manufacturers in the international market. The main export destinations are EU countries: Norway, the Netherlands, and Germany.

The market shows a trend toward the adoption of eco-friendly technologies, including the use of hemp and straw insulation, CLT panels, and the integration of circular economy principles.

Companies involved in the manufacture of prefabricated and modular buildings based on a wooden frame reported a 70% decline in orders in 2022; at that time, the companies’ revenue was generated by projects that had been financed in 2021. In 2023, companies began to reach 50% of 2021 levels; in 2024, the market landscape began to shift due to orders from international organizations, such as a tender for 3,000 modular homes organized by UNHCR. Overall, the task of providing housing for IDPs became the driving force behind the increase in modular building production.

The standard floor area for a frame-technology residential building is considered to be 80–100 square meters, and for a modular one—30–40 square meters.

At the same time, the development of rapid-assembly construction technologies is hampered by a number of systemic issues, in particular, the legal uncertainty regarding the status of such housing (rapid-assembly structures are most often classified as temporary structures or construction products under current legislation and are not commissioned as real estate properties). The study recommends regulating this status, as well as developing and codifying terminology related to prefabricated construction in legislation, and developing and implementing an updated classification of technologies with corresponding product codes.

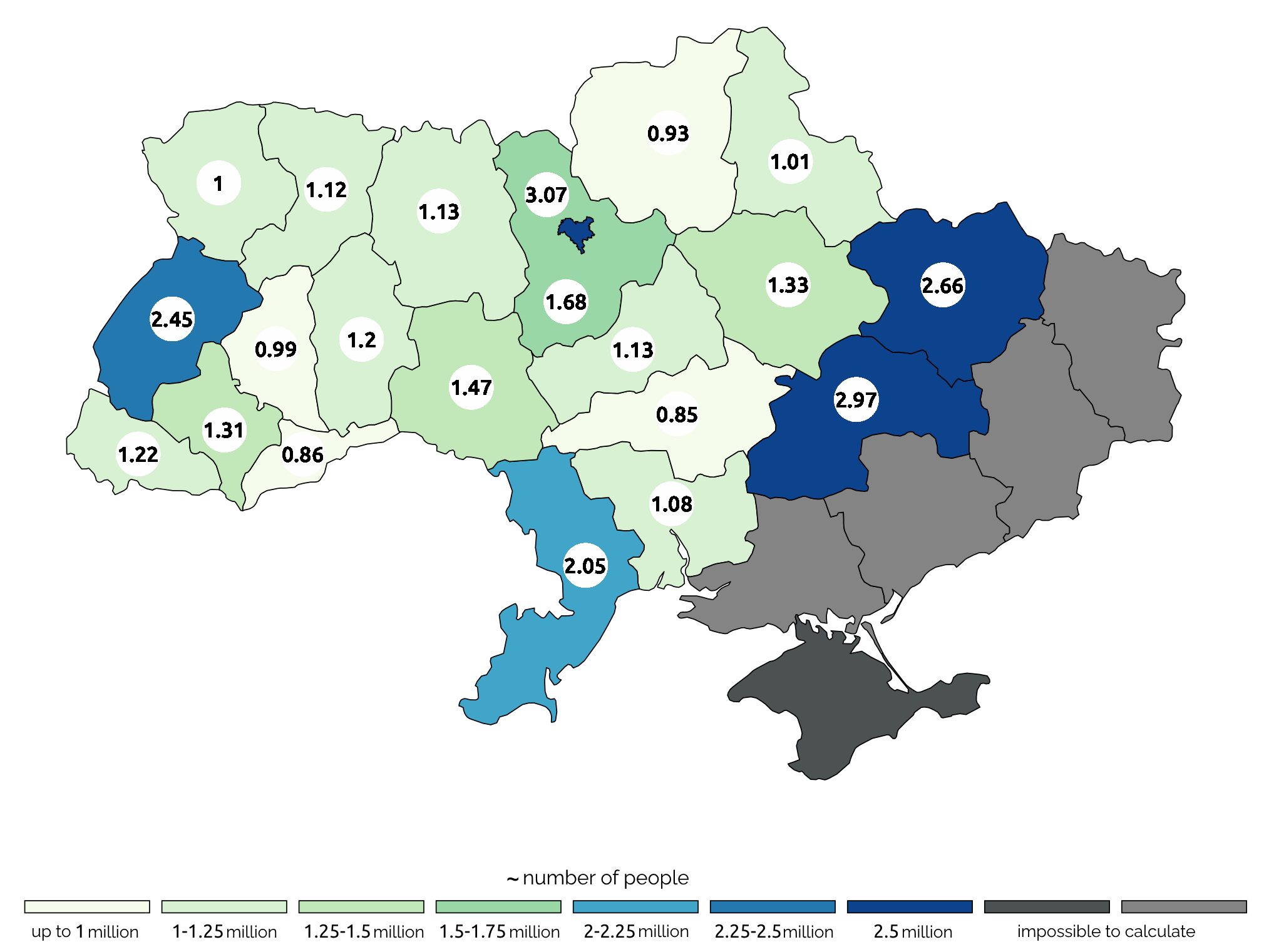

Estimated number of population in regions of Ukraine based on number of active mobile sim cards (mln)