Egypt’s largest developers maintained high sales levels in early 2026, despite cooling demand and the real estate market entering a more cautious phase, according to a report by The Board Consulting.

According to the report, the total value of contracts signed by Egypt’s ten largest developers in the first quarter of 2026 amounted to 271 billion Egyptian pounds, or more than $5 billion. This is 6.5% less than the record 290 billion pounds a year earlier, but the figure remains significantly higher than in previous years and confirms the resilience of the market’s largest players.

In physical terms, sales declined more sharply—by approximately 15%—to about 15,500 units. This reflects more cautious buyer behavior amid rising construction costs, currency volatility, changing financing conditions, and general macroeconomic uncertainty.

However, the market has not collapsed but is rather undergoing a structural shift. The main cash flows are concentrated among the largest and financially stable developers, while small and medium-sized developers face pressure due to the cost of capital, competition, and the need to offer long-term installment plans.

East Cairo remains the geographic leader, generating contracts worth 130 billion pounds over the quarter. Demand is driven by new residential complexes, proximity to the New Administrative Capital, and large-scale infrastructure development in the eastern part of the metropolitan area.

For foreign buyers, Egypt remains one of the most affordable major real estate markets in the region. The weakening of the Egyptian pound has made housing relatively cheaper for buyers holding dollars, euros, or Gulf currencies. According to Global Property Guide, real estate prices in Egypt rose by 13.25% year-over-year in October 2025, but in real terms—adjusted for inflation—growth amounted to only 0.67%.

External demand is driven primarily by several groups. The first consists of investors from Gulf countries, primarily the UAE, Saudi Arabia, Kuwait, Qatar, Bahrain, and Oman. Egyptian developers are actively promoting projects in the GCC, and Gulf buyers have high purchasing power and interest in large resort and urban projects. Invest-Gate notes that buyers from Gulf countries and the Egyptian diaspora already account for about one-third of sales under the “real estate export” initiative.

The second group is the Egyptian diaspora. For Egyptians living in Europe, the U.S., the Gulf states, and other regions, real estate in Egypt remains a way to maintain a connection with the country, protect capital from inflation, and acquire housing for their families or for a future return.

The third group consists of buyers from Arab countries experiencing political or economic instability. Among them, citizens of Syria, Iraq, Sudan, and Palestine are frequently mentioned. For some of these buyers, real estate in Egypt is linked not only to investment but also to residency, obtaining resident status, and long-term security.

The fourth group consists of buyers from Russia, Ukraine, and Kazakhstan, primarily in Red Sea resort locations, including Hurghada, El Gouna, and the areas around Sahl Hasheesh. For them, Egypt is attractive due to its low entry barrier, warm climate, tourist demand, and the opportunity to purchase housing at a lower cost than in Turkey, the UAE, or certain European markets.

The fifth group consists of European buyers, including citizens of Germany, the UK, Italy, and other EU countries, who view Egypt as a market for affordable resort real estate, rentals, and seasonal living.

For foreign buyers, an important feature of the market is the long-term installment plans offered by developers. In Egypt, a significant portion of housing is sold off-plan, and buyers often make a 5–10% down payment and pay the remainder over 7–10 years. This mechanism makes the market accessible but simultaneously increases the importance of choosing a reliable developer and conducting a legal review of the contract.

The Egyptian government is also seeking to more actively develop “real estate exports” as a source of foreign exchange revenue. Authorities view the sector as a tool for attracting foreign capital, especially following the $35 billion Ras El-Hekma deal with Abu Dhabi’s ADQ, which became the largest foreign direct investment agreement in the country’s history.

Thus, the Egyptian real estate market is not entering a crisis phase, but rather a phase of weeding out weaker players. Buyers are becoming more cautious, and the volume of transactions is declining, but the largest developers continue to generate billions of dollars in sales. For foreign investors, the main concern now is not just price, but the reliability of the project, currency risks, the legal soundness of the transaction, and the developer’s ability to complete the project on time.

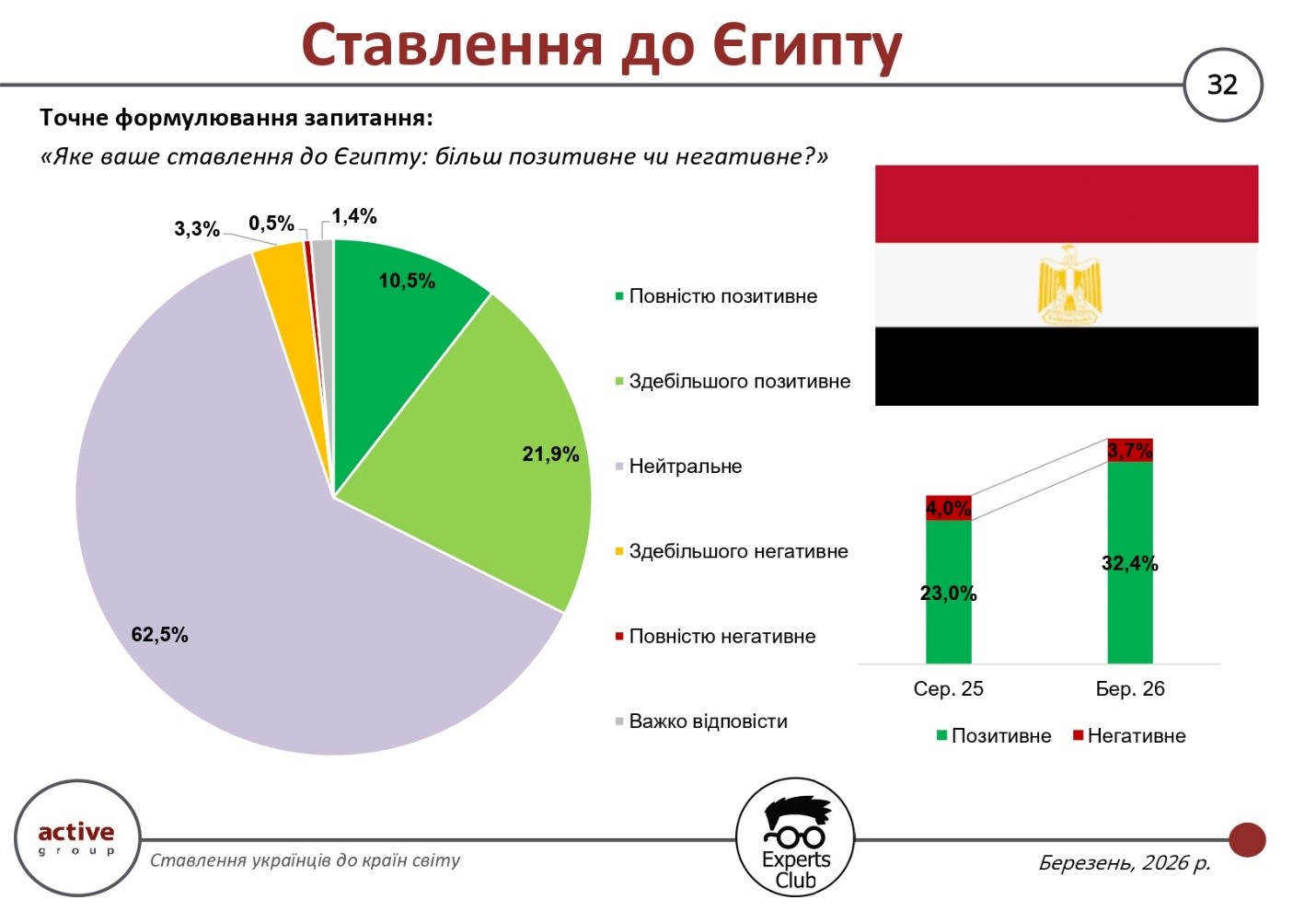

Ukrainians’ attitude toward Egypt remains largely neutral, but trends over the past few months indicate a noticeable improvement in perceptions of the country. According to the results of a sociological survey conducted in March 2026 by the research company Active Group in collaboration with the Experts Club information and analytical center, 32.4% of respondents view Egypt positively, whereas in August 2025 this figure stood at 23.0%. At the same time, the share of negative assessments has decreased slightly—from 4.0% to 3.7%.

The breakdown of responses shows that the largest group remains respondents with a neutral stance—62.5%. This means that for most Ukrainians, Egypt does not belong to the category of countries with a clearly defined emotional image. The positive attitude consists of 10.5% “completely positive” and 21.9% “mostly positive” assessments. The negative segment remains minimal: 3.3% of respondents chose “mostly negative,” 0.5% chose “completely negative,” and another 1.4% were undecided.

Thus, the main feature of attitudes toward Egypt is a combination of very high neutrality with a gradual increase in positive sentiment. This indicates that the country does not yet occupy a prominent place in the Ukrainian information space, yet its image is not negative and has the potential for further improvement. It is also important that the increase in positive assessments is occurring without a rise in critical perception.

“Egypt is a very interesting example of the gap between economic statistics and public perception. Egypt ranks first among Ukraine’s trading partners in terms of trade surplus—over $1.224 billion—meaning it is one of the most profitable markets for us. But in public opinion, we see a predominantly neutral attitude, which means: the country’s economic weight has not yet translated into an equally strong reputational presence,” noted Maksim Urakin, founder of the Experts Club information and analytical center.

From an analytical perspective, this means that Egypt is already an important economic partner for Ukraine, but has not yet become a country with a clearly established positive image in the public consciousness. Given such a significant positive trade balance, the potential for strengthening the bilateral image remains quite high. If economic cooperation is complemented by greater public visibility, humanitarian contacts, and an information presence, some of the current neutrality may eventually shift toward a more pronounced positive perception.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, Egypt ranks 19th in total trade volume with Ukraine, with a figure of $1.82 billion. At the same time, Ukraine has a significant trade surplus with Egypt, as exports of Ukrainian goods exceed imports by more than five times.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, EGYPT, EXPERTS CLUB, Pozniy, SOCIOLOGY, SURVEY, UKRAINE, URAKIN

In 2025, Ukraine imported 123,600 tons of potatoes, which is 2.4 times more than in 2024; the cost of purchasing them increased 2.5 times to $66.29 million, according to the State Customs Service.

Poland (37.1%), Egypt (13.56%), and the Netherlands (11.58%) became the leaders in potato supplies to Ukraine.

In January-December 2025, Ukraine imported 138,410 tons of potatoes, which is 5.3 times (+431.3%) more than in 2024, when 26,050 tons were imported into the country, according to the State Customs Service.

According to published statistics, in monetary terms, potato imports increased 4.9 times (+391.9%) to $74.82 million compared to $15.21 million a year earlier. The main imports came from Poland (38.2%), Egypt (14.1%), and the Netherlands (10.8%).

Potato exports from Ukraine during the same period amounted to 2.38 thousand tons, which is 11.2% less than in 2024 (2.68 thousand tons). At the same time, despite the physical reduction in export volumes, in monetary terms, the sale of Ukrainian potatoes abroad was more profitable and brought in 3.1% ($584 thousand) more revenue than in 2024 ($566 thousand). The main buyers were Moldova (60.2% of all exports), Azerbaijan (35.4%), and Georgia (1.2%).

As reported, Ukraine had a poor potato harvest in the 2024 season due to drought, extremely high temperatures, and a lack of seed material.

Deputy Minister of Economy, Environment, and Agriculture Taras Vysotsky noted in a podcast by the Center for Economic Strategies that the 2025 vegetable harvest in Ukraine is sufficient and even larger than last year, so no shortage is expected in this sector.

Commenting on Ukraine’s potato imports in 2024-2025, Mykola Furdyga, director of the Potato Institute, explained that this record volume of imports was caused by the unusual weather conditions in 2024. Therefore, the state was forced to import potatoes to meet domestic food needs. European countries were eager to supply Ukraine with their products due to their attractive prices. At the same time, potatoes from Egypt did not dominate the market but occupied their traditional niche in the off-season (February-March – IF-U). In addition, Ukraine traditionally imports seed potatoes from leading breeding companies in the European Union.

Furdyga noted that since the beginning of the war, there has been a trend in Ukraine toward reducing potato cultivation in households and expanding production areas for this crop in farms and even in agricultural holdings. He explained this trend by the departure of the population from villages abroad and mobilization.

In the first two months of the new marketing year (2025/2026 MY), which began on July 1, Ukraine exported 1.456 million tons of wheat, which is 28% less than in the same period last season (2.026 million tons), according to APK-Inform.

Egypt became the key importer of Ukrainian wheat, almost doubling its purchases to 699,000 tons and becoming the largest buyer.

At the same time, most other traditional importers reduced their volumes:

Supplies also decreased to:

As of early September, Ukraine had harvested 30.4 million tons of grain crops on an area of 7.2 million hectares, which is about 63% of the total crop.

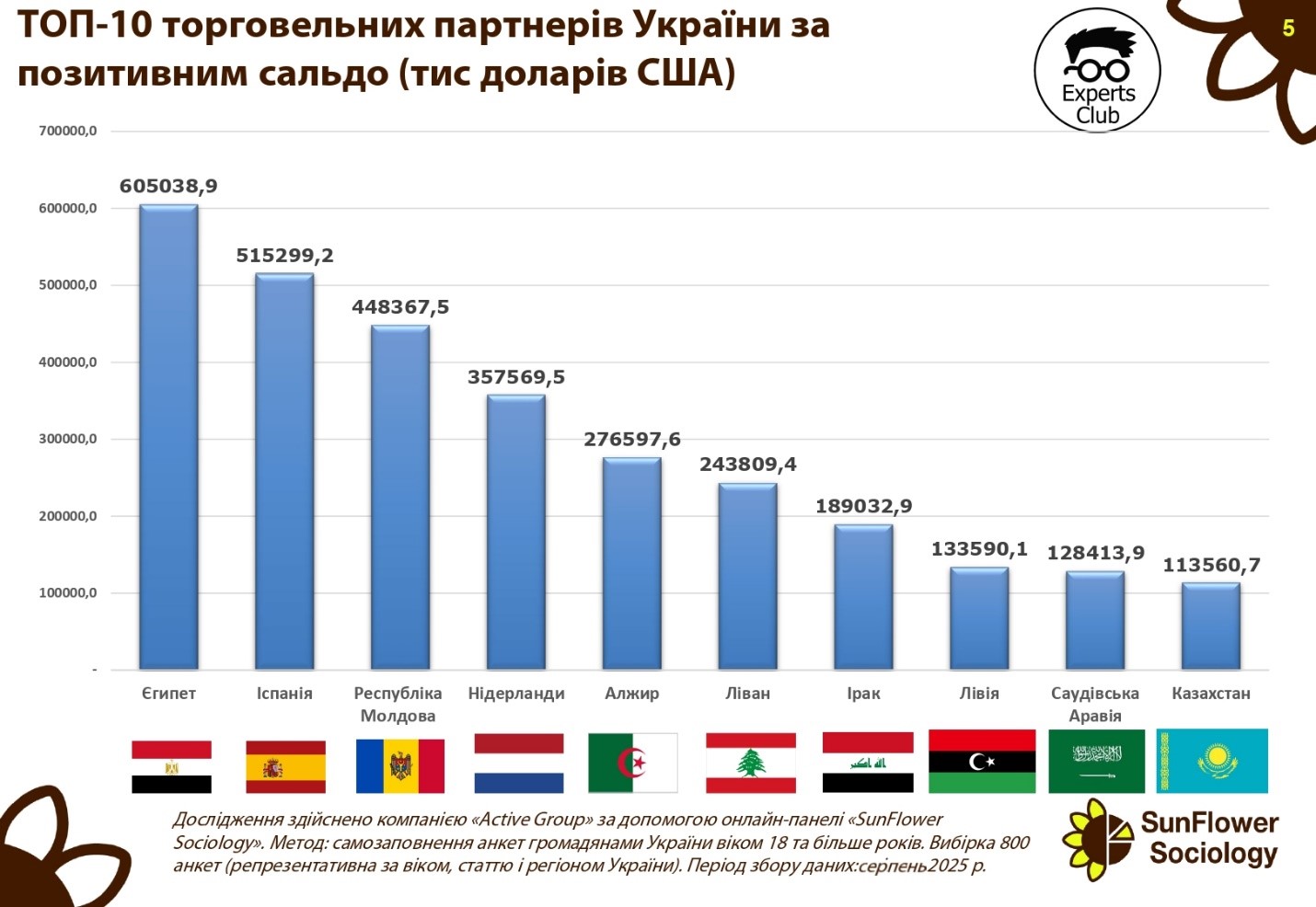

Earlier, the Experts Club information and analytical center presented a study of Ukraine’s main trading partners in the first half of 2025, where Egypt ranked first in terms of positive balance among all of Ukraine’s trading partners.

“Egypt is an extremely important and profitable trading partner for the country, along with a number of other Arab states. Partnerships with these countries provide the country with currency and somewhat correct the extremely negative trend of recent years with Ukraine’s constantly growing trade deficit,” emphasized Maxim Urakin, founder of Experts Club.

Ukraine maintains a significant positive trade balance with a number of key partners, which partially offsets the deficit in relations with China and EU countries.

The largest surplus in the first half of 2025 was recorded in trade with Egypt — $605.0 million. Spain ranks second with a balance of $515.3 million, followed by the Republic of Moldova — $448.4 million. Positive dynamics are also observed in relations with the Netherlands ($357.6 million), Algeria ($276.6 million), and Lebanon ($243.8 million).

Ukraine also has a high trade surplus with Iraq ($189.0 million), Libya ($133.6 million), Saudi Arabia ($128.4 million), and Kazakhstan ($113.6 million).

“The positive trade balance indicates that Ukraine is capable of competing effectively in international markets, especially in the agricultural sector and metallurgy. At the same time, it should be borne in mind that these markets are vulnerable to changes in the global economic situation, price fluctuations, and political factors,” emphasized Maksim Urakin, founder of Experts Club and economist.

According to him, maintaining a positive balance in relations with the countries of the Middle East and North Africa is a key element of Ukraine’s foreign trade strategy.

“Egypt, Spain, and the countries of the Arab world are stable importers of Ukrainian agricultural products. This is a strategic direction that needs to be developed further, as it creates a safety cushion for the economy against the backdrop of significant import costs,” Urakyn emphasized.

Analysts note that consolidating positions in the African and Middle Eastern markets could become a long-term factor in strengthening Ukraine’s foreign economic balance.

Agricultural exports, ALGERIA, ECONOMY, EGYPT, EXPERTS CLUB, FOREIGN TRADE, IRAQ, KAZAKHSTAN, LEBANON, LIBYA, MOLDOVA, NETHERLANDS, positive balance, SAUDI ARABIA, SPAIN, UKRAINE, МАКСИМ УРАКИН