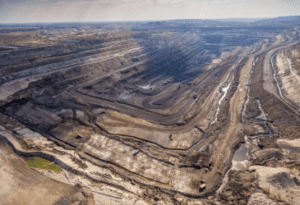

British-based Ferrexpo plc, which controls in Ukraine, in particular, Poltava and Yeristovo mining and processing plants, in January-September 2021 increased total production of pellets by 0.3% compared to the same period in 2020, to 8.158 million tonnes.

According to a press release from the company on Wednesday, total production, including pellets and salable concentrate, rose 3% to 8.393 million tonnes over the period.

At the same time, total production of pellets with 65% iron content amounted to 7.829 million tonnes (a decrease of 0.3%). Pellets with 62% iron content were not produced. Production of direct reduction (DR) pellets with 67% iron content amounted to 330,000 tonnes (up by 76%).

Over the nine months of 2021, the company also produced 234,000 tonnes of salable concentrate with 67% iron content, while in 2020 it did not produce salable concentrate.

In the third quarter of 2021, total pellet production fell 9% quarter on quarter (qoq), but increased 2% versus Q3 2020, to 2.596 million tonnes. In particular, 2.401 million tonnes of pellets with 65% iron content were produced (a decrease by 13% versus the second quarter of 2021 and by 5% versus the third quarter of last year), no pellets with 62% grade were produced, production of DR pellets with 67% iron content amounted to 195,000 tonnes (an increase of 130% compared to the previous quarter).

The company also produced 85,000 tonnes of salable concentrate with 67% iron content in the third quarter of 2021 (an increase of 0.2% compared to the second quarter).

Total production, including production of pellets and commercial concentrate, in the third quarter of this year decreased by 9% compared to the second quarter of 2021, but increased by 6% compared to the third quarter of 2020, to 2.680 million tonnes.

The press release explains that the 2% increase in iron ore pellet output in Q3 2021 versus Q3 2020 reflects strong production performance following pelletiser upgrade work completed in previous quarters. Production volumes are 9% lower on a quarter on quarter basis as a result of pelletiser upgrade work completed during the quarter, and planned pelletiser maintenance in September 2021.

In addition, upgrade work on the group’s fourth pelletiser line completed during September 2021.

Production of iron ore concentrate with a high iron content (65% and above) in the third quarter was in line with the previous quarter.

In addition, it clarifies that the proportion of direct reduction pellets with higher iron content (67% Fe) increased to 8% of total pellet production during the third quarter from 3% in the previous quarter, reflecting the group’s continuing expansion into this market.

In turn, continued production of commercial high grade concentrate (67% Fe) at 85,000 tonnes in the third quarter reflects the group’s recent investment in in its concentrate stockyard project.

Interim Group Chief Executive Officer Jim North pointed to the group’s continued progress towards improving product quality and output following the completion of the pelletizer upgrade.

“Through continued investment in the group’s concentrator and pelletiser facilities, we are creating a platform for future growth in product volumes, whilst simultaneously increasing the overall grade of our production,” North is cited in the press release.

British-based Ferrexpo plc, which controls in Ukraine, in particular, Poltava and Yeristovo mining and processing plants (Poltava GOK and Yeristovo GOK), in January-July of this year, according to recent data, increased production of pellets by 2.9% compared to the same period last year, to 6.563 million tonnes.

A representative of the company informed Interfax-Ukraine that in July production of pellets amounted to 1 million tonnes.

According to an announcement on the London Stock Exchange, on September 17, 2021, a general meeting of shareholders will take place, the only issue at which is the re-election of Vitaliy Lisovenko to the company’s board of directors.

At the same time, it is explained that at the annual general meeting of the company on May 27, 2021, independent non-executive director Lisovenko did not receive the required number of votes for reappointment to the board of directors. In the event that the candidacy of the independent director is approved by a majority of votes of all voting shareholders at the second general meeting, the director will be re-elected before the next annual general meeting.

The second vote will take place at 11:00 on Friday, September 17, 2021, the shareholders can participate in person at the meeting or online.

As of August 23, 2021, the issued share capital of the company consisted of 588,624,142 ordinary shares with one vote each.

Ferrexpo in 2020 increased its total pellet production by 7% compared to 2019, to 11.218 million tonnes. Concentrate output increased by 5.9%, to 14 million tonnes.

Ferrexpo is an iron ore company with assets in Ukraine.

Ferrexpo owns 100% of shares in Poltava GOK, 100% in Yeristovo GOK and 99.9% in Belanovo GOK.

Ferrexpo mining company with assets in Ukraine in January-June 2021 received $661.426 million in net profit, which is 2.65 times higher than in 2020 ($249.908 million).

According to the half year report of the company posted on the London Stock Exchange on Wednesday, its revenue for the reporting period grew by 74.3%, to $1.353 billion from $775.831 million.

EBITDA jumped 2.47 times, to $868 million from $352 million in the first half of 2020.

Ferrexpo’s capital investment in the first half of this year was $142 million, up from $96 million in the first half of last year.

Interim dividends amounted to 39.6 cents per share (in the first half of 2020 they were 13.2 cents).

Ferrexpo, a mining company with assets in Ukraine, has launched a pilot project of a 5 MW solar battery complex at the operating industrial site of Poltava Mining and Processing Plant (Poltava GOK) without a feed-in tariff, the company said.

“This is a pilot project, after which the company will move to a full-scale replacement of conventional electricity with renewable energy from the sun as part of the program of decarbonization of manufactured products. Ferrexpo plans to build a power plant for the production of renewable energy with a capacity of 250-1,000 MW in the medium term,” the document says.

According to the report, almost 10,000 photovoltaic panel of Jinko Solar were used in the implemented project, the panels are installed on the dumps of the quarries in order to rationalize the use of the area.

The cost, according to the press release, was “several million U.S. dollars.” The company financed it without using any state compensation programs, subsidies, grants or a feed-in tariff.

“We have achieved a market return on this project without any feed-in tariffs from the state, which should be an example for other enterprises building renewable energy generation facilities,” Ferrexpo said.

According to chairman of the board of Poltava GOK Viktor Lotous, the solar plant will generate 6.5-7 million kWh of electricity per year and supply it for consumption by the group’s enterprises at the operating industrial site.

“The launch of its own generation reduces the negative consequences of monopolization of the energy market for Ferrexpo due to the restriction of competition and the risks of an increase in the tariff for electricity transmission,” he said.

Ferrexpo owns 100% of shares in Poltava GOK, 100% in Yeristovo GOK and 99.9% in Belanovo GOK.

In 2020, the company increased its net profit by 57.5%, to $ 635.3 million with an increase in revenue by 12.8%, to $ 1.700 billion. Last year, Ferrexpo increased its total production of pellets by 7%, to 11.22 million tonnes, concentrate output increased by 5.9%, to 14 million tonnes.

In the first half of this year, Ferrexpo cut pellet production by 0.6%, to 5.563 million tonnes, but total production, which also includes commercial concentrate, rose by 2%, to 5.712 million tonnes.

The Board of Directors of Ferrexpo with assets in Ukraine has approved the early repayment of its outstanding pre-export finance facility (PXF facility) the agreement on which was signed in 2018. As at December 31, 2020, the group had $257 million of debt drawn on its PXF facility.

The company said on Wednesday that repayment is to take place today, while earlier repayment was scheduled to take place quarterly between 2020 and 2022.

Early repayment of this facility reflects the strong performance of the group’s operations, including recent growth in both the group’s production volumes and product quality, following the recent completion of investments throughout the group’s operations, representing prudent cash management practice.

British-based Ferrexpo Plc, which in Ukraine, in particular, controls Poltava and Yeristovo ore mining and processing plants (Poltava GOK and Yeristovo GOK), intends to increase production of direct reduction (DR) pellets which are higher grade (67% Fe) in 2021.

In 2020, the group increased production of high grade (65% Fe or above) iron ore pellets to 99% of total output, up from 96% in 2019, according to an annual report released by the company on the London Stock Exchange on Wednesday.

In addition to this, the group has also started production of direct reduction (DR) pellets, which have a higher grade (67% Fe) and less impurities than other types of iron ore pellets.

“DR pellets are expected to represent the future of global steel production, as steelmakers transition to the production of carbon-free Green Steel, with DR pellets the primary source of virgin iron utilized in this process. The Group continues to develop its offering of DR pellets, production of which is possible through the Group’s existing production facilities, with two trial cargoes in 2020, and a further four trial cargoes planned for 2021,” the group said in the report.

The group also continues to utilize sunflower husks as a biofuel in its pelletiser, as a substitute for natural gas. This project has been in place since 2015, and usage has steadily increased as the Group optimizes the usage of husks in its pelletisers. In 2020, the Group successfully increased usage to 25% of the total energy consumed in the pelletiser (2019: 22%).

In 2020, the company increased its processing activities in the beneficiation plant increased by 4% to 30 million tonnes in 2020, following the implementation of new processing capacity in the second half of 2020.

Expectations for processing in 2021 are for a further increase as operations realize a full year at the plant’s newly expanded processing capacity. The Group is also progressing construction of its concentrate stockyard, press filtration and medium-and fine-crushing projects, which are collectively expected to provide additional operational flexibility in processing.

According to the report, the cost of production in 2020 decreased by 13%, to $41.5 per tonne from $47.8 per tonne. The decrease in costs was mainly attributable to falling commodity prices, in particular oil prices, lower electricity prices and the weakening of hryvnia.

The company’s gross debt as of December 31, 2020 was $266 million, up from $412 million at the end of 2019.

Ferrexpo sold pellets and concentrate in 2020, in particular, in Austria for $356.461 million (in 2019 for $331.964 million), in Germany for $145.311 (in 2019 for $168.875 million), in Japan for $78.786 million ($161.186 million), to China for $908.949 million ($347.892 million), to Turkey for $82.514 million ($62.717 million), to the United States for $34.236 million (there were no supplies in 2019).

The company’s annual meeting is scheduled for May 27, 2021.