The article presents key macroeconomic indicators of Ukraine and the global economy as of the end of March 2026. The analysis was prepared on the basis of current data from the State Statistics Service of Ukraine (SSSU), the National Bank of Ukraine (NBU), the International Monetary Fund (IMF), the World Bank, as well as leading national statistical agencies (Eurostat, BEA, NBS, ONS, TurkStat, IBGE). Maksym Urakin, PhD in Economics and founder of the Experts Club information and analytical center, presented an overview of current macroeconomic trends that determined the situation in Ukraine and the world at the beginning of 2026.

Macroeconomic indicators of Ukraine

As of the end of March 2026, the Ukrainian economy remained in a mode of managed macrofinancial stabilization, but the first quarter showed a noticeable deterioration in the balance of risks compared with the beginning of the year. After a relatively favorable January, when inflation was declining, reserves were at a historically high level, and the NBU began cautious easing of interest rate policy, the situation became more complicated in February-March. Inflation accelerated again, international reserves declined for the second month in a row, the foreign exchange market required significant interventions by the regulator, and the first quarterly GDP estimate showed a decline.

According to the preliminary estimate of the State Statistics Service, Ukraine’s real GDP in Q1 2026 decreased by 0.6% compared with Q1 2025, and by 0.7% compared with the previous quarter, taking into account the seasonal factor. Nominal GDP amounted to UAH 2,047.2 billion. This became an important signal that economic recovery remains unstable and highly sensitive to energy, military and foreign trade shocks.

In its April Inflation Report, the National Bank worsened its forecast for Ukraine’s real GDP growth in 2026 to 1.3%, taking into account further destruction of infrastructure, larger electricity deficits and the effects of a significant increase in energy prices. This means that even if international support is maintained and the situation on the foreign exchange market remains controlled, the economy is entering 2026 on a lower growth trajectory than previously expected.

“The first quarter of 2026 showed that the Ukrainian economy has still not moved into a classic recovery phase. We have a stabilization model that works thanks to international financial support, budget expenditures, business adaptation and NBU policy. But the decline in GDP in the first quarter indicates that the margin of safety remains limited. Energy destruction, labor shortages, weak exports and military risks are quickly affecting the real sector. Therefore, the main task for 2026 is to gradually restore the productive base of the economy,” Urakin noted.

Inflation dynamics in March also became less favorable. According to the State Statistics Service, as commented on by the NBU, consumer inflation accelerated to 7.9% year-on-year in March 2026. Month-on-month, prices rose by 1.7%. After the January slowdown to 7.4% and the February acceleration to 7.6%, the March figure confirmed that the disinflationary trend had become less stable.

The NBU explained the March acceleration primarily by the increase in prices for raw food products, fuel and certain services. Additional pressure was created by energy risks, rising business costs, the impact of external energy prices and increasing geopolitical tension. At the same time, core inflation remained closer to the forecast trajectory, which allowed the regulator not to move to a sharp tightening of policy, but at the same time limited the room for a further rapid reduction in the rate.

At the end of March, the NBU key policy rate remained at 15.0%. On March 20, the Board of the National Bank decided to keep it unchanged after the January reduction from 15.5% to 15.0%. The regulator explained this by the need to maintain the attractiveness of hryvnia assets, preserve the stability of the foreign exchange market and control inflation expectations.

“March effectively paused the discussion about rapid monetary policy easing. Inflation accelerated, the foreign exchange market remained tense, and external risks increased. Under such conditions, keeping the rate at 15% was a logical decision. Ukraine cannot afford to stimulate the economy at the cost of losing confidence in the hryvnia. In a wartime economy, the stability of expectations is often more important than a short-term reduction in the cost of credit,” Urakin emphasized.

The foreign exchange sector remained controlled but required significant support from the NBU. As of April 1, 2026, Ukraine’s international reserves amounted to almost $52.0 billion. In March, they decreased by 5.0%. This dynamic was caused by the National Bank’s foreign exchange interventions and the country’s debt payments in foreign currency, which were only partially compensated by inflows from international partners and the placement of foreign currency domestic government bonds.

Despite the decline, reserves remained high by historical standards and continued to serve as the main financial safety cushion. At the same time, the very need for large interventions indicated that the private foreign exchange market continued to have a structural currency deficit. Ukraine imports significantly more than it exports, and therefore exchange rate stability is largely supported by external financing and the NBU’s reserves.

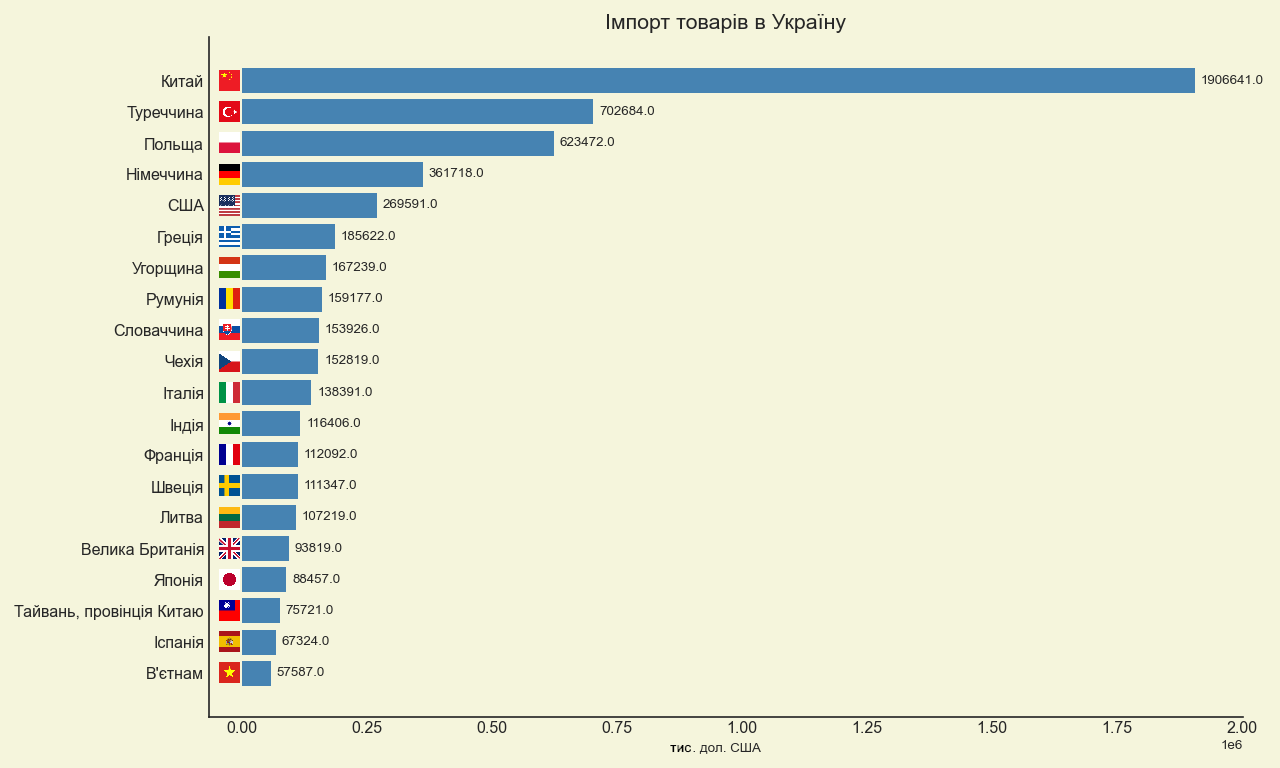

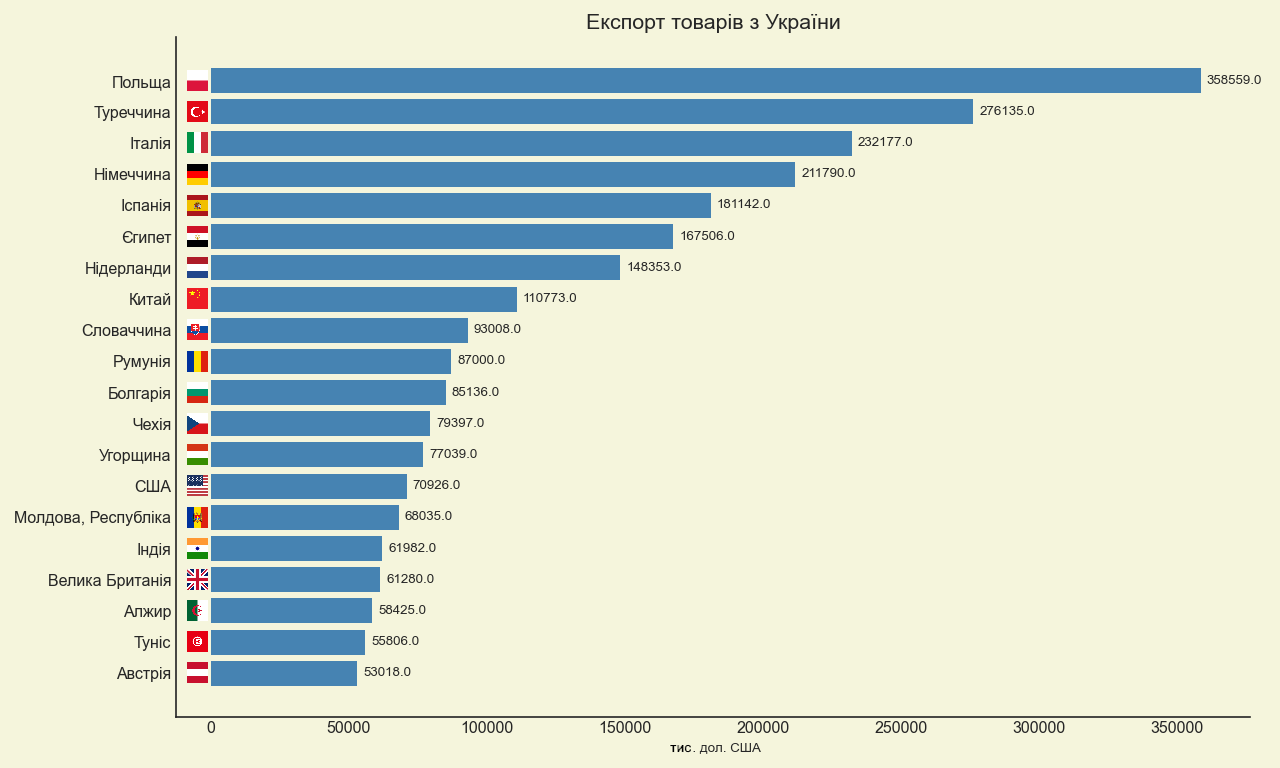

Foreign trade in the first quarter confirmed this problem. According to the State Customs Service, Ukraine’s trade turnover in January-March 2026 amounted to $33.5 billion. Imports reached $23.4 billion, while exports amounted to $10.1 billion. Thus, the goods deficit over three months amounted to about $13.3 billion, and imports were more than twice as high as exports.

In the import structure, machinery, equipment, transport, fuel and energy goods, and chemical industry products played a key role. China, Poland and Turkey remained the largest import trading partners. The export base remained significantly narrower: the main positions were food products, agricultural products, metals and certain machinery products. The main export destinations remained EU countries and Turkey.

“The trade deficit of the first quarter is one of the most important indicators of the vulnerability of the Ukrainian economy. Reserves and external assistance make it possible to pass through this period without a currency crisis, but they do not replace the country’s own export capacity. When imports are more than twice as high as exports, it means that the country is financing a significant part of its needs through external resources. In wartime conditions this is inevitable, but strategically such a model cannot be permanent. Ukraine must increase exports of products with higher added value, develop processing, logistics, energy autonomy and the defense-industrial complex,” Urakin stressed.

The budget situation following the results of the first quarter also remained tense. According to the Ministry of Finance, UAH 734.6 billion was received by the general fund of the state budget in January-March 2026. At the same time, cash expenditures of the general fund for this period amounted to UAH 916.4 billion, which is 7.1% more than in the corresponding period of the previous year. In March, expenditures amounted to UAH 369.1 billion.

Expenditures on security and defense in January-March amounted to UAH 570.9 billion, or 62.3% of all expenditures of the general fund. This confirms that the state budget in 2026 remains primarily a war budget. The largest areas of expenditure included remuneration in the budget sector with accruals, social security, subsidies and transfers to enterprises, payment for goods and services, servicing of public debt and transfers to local budgets.

“The budget of the first quarter of 2026 shows that the state maintains financial manageability, but the price of this manageability is very high. More than 60% of general fund expenditures are directed to security and defense, and this is absolutely understandable in wartime conditions. But such a structure means that the room for classic investment in development is limited. Therefore, international support, the domestic government bond market and the government’s ability to expand its own tax base through the restoration of economic activity remain critically important,” Urakin noted.

Global economy

As of the end of March 2026, the global economy remained resilient, but less predictable than at the beginning of the year. While in January the IMF’s baseline scenario projected global economic growth of 3.3% in 2026, in the April World Economic Outlook the Fund revised its estimates amid new geopolitical tensions in the Middle East. Under the baseline assumption of a limited conflict, the IMF forecast global growth of 3.1% in 2026 and 3.2% in 2027.

The IMF noted that the global economy had once again faced a shock related to war, rising commodity prices, stronger inflation expectations and tighter financial conditions. This meant that the global environment for Ukraine became less favorable: energy prices, risks to trade and the cost of capital again began to play a greater role.

The United States remained one of the main centers of global resilience. In the first quarter of 2026, U.S. real GDP grew by 2.1% year-on-year, according to the BEA estimate. Growth was supported by investment, exports, government spending and consumer spending. At the same time, inflation in the United States accelerated noticeably in March: the consumer price index rose by 3.3% year-on-year after 2.4% in February, while core CPI stood at 2.6%.

The Federal Reserve in March kept the target range for the federal funds rate at 3.5–3.75%. This meant that U.S. monetary policy remained restrictive, while expectations of a rapid rate cut were postponed. For countries with elevated risk, including Ukraine, this meant the preservation of a relatively high cost of global capital.

The eurozone was in a more difficult position. Its economic growth remained weak, while inflation again rose above the ECB’s target. According to Eurostat’s preliminary estimate, annual inflation in the eurozone in March 2026 stood at 2.5%, while the final estimate later showed 2.6%. In February, the figure was 1.9%, meaning that March brought a noticeable acceleration of price pressure. The main factor was energy, while core inflation remained more moderate.

The European Central Bank in March kept key rates unchanged: the deposit rate at 2.0%, the main refinancing operations rate at 2.15%, and the marginal lending facility rate at 2.40%. For Ukraine, the eurozone remains the most important external economic environment due to trade, financial assistance, EU integration, migration flows and logistics corridors. However, the weak growth rate in Europe limits the potential for a rapid increase in Ukrainian exports.

The United Kingdom also entered 2026 with a combination of moderate growth and an elevated inflation background. In March, the British CPI rose to 3.3% year-on-year after 3.0% in February. The Bank of England kept the Bank Rate at 3.75%, reflecting the regulator’s caution in the face of the risk of a new inflation acceleration. For the European region as a whole, this meant that the cycle of rapid monetary easing had not begun.

“The global economy did not enter a recession in the first quarter of 2026, but it became noticeably more nervous. The United States maintains stable growth, but is facing a new inflation acceleration. The eurozone has a weaker economic impulse and again sees inflation above the target. The United Kingdom also remains in a mode of cautious monetary policy. For Ukraine, this means that the external world does not create a catastrophic background, but also does not provide an easy impulse for recovery. Under such conditions, it is impossible to rely only on external demand,” Urakin noted.

The Chinese economy maintained relatively strong dynamics in the first quarter of 2026. According to the National Bureau of Statistics of China, China’s GDP grew by 5.0% year-on-year in Q1, and by 1.3% quarter-on-quarter. Nominal GDP amounted to about 33.4 trillion yuan. At the same time, inflation remained moderate: CPI rose by 1.0% year-on-year in March, and averaged 0.9% in January-March.

China continued to demonstrate a strong manufacturing base and export potential, but structural problems — weaker domestic demand, the real estate market, debt burden and dependence on external markets — remained important constraints. For Ukraine, China remained a key source of imports, primarily machinery, equipment, electronics and industrial goods.

India retained its status as one of the main drivers of global growth. According to the government’s first advance estimate, India’s real GDP in the 2025/26 fiscal year was expected to grow by 7.4%, while nominal GDP was expected to grow by 8.0%. The main driver remained the services sector, as well as domestic demand and public investment. The Indian economy remained one of the most convincing examples of combining high growth with relatively controlled inflation.

Turkey remained an example of an economy with relatively high business activity, but a very difficult inflationary legacy. According to official TurkStat data, in March 2026 consumer prices rose by 1.94% month-on-month and by 30.87% year-on-year. This was lower than in February, when annual inflation was 31.53%, but still remained an extremely high level. At the same time, the Turkish economy grew by 3.6% in 2025, which indicated the preservation of domestic demand despite inflationary risks.

Brazil looked more balanced among large emerging economies. According to IBGE, Brazil’s GDP in 2025 grew by 2.3%, to 12.7 trillion reais at current prices. Growth was observed in the agricultural sector, industry and the services sector. According to the preliminary IPCA-15 indicator, inflation in March 2026 amounted to 0.44% for the month and 3.90% over the last 12 months. This confirmed that Brazil maintained a relatively controlled inflation background, although its economy also felt the impact of high rates and external uncertainty.

“China, India, Turkey and Brazil show different development models of large emerging economies. China maintains scale and manufacturing strength, but has structural imbalances. India demonstrates the highest dynamics among major economies and relies on domestic demand and the services sector. Turkey is growing, but pays for it with high inflation. Brazil is moving more slowly, but more balanced. For Ukraine, it is important to look at these examples practically: in global competition, those countries win that can simultaneously maintain macro-stability, production, exports and domestic investment demand,” Urakin believes.

Conclusions

As of the end of March 2026, Ukraine maintained macrofinancial manageability, but the first quarter demonstrated the fragility of economic stabilization. Real GDP in Q1 decreased by 0.6% year-on-year, inflation accelerated to 7.9% in March, the key policy rate remained at 15.0%, international reserves declined to about $52.0 billion, and the goods deficit in January-March exceeded $13 billion. The budget remained functional, but its structure was fully subordinated to wartime needs: more than 60% of general fund expenditures were directed to security and defense.

The main risks for Ukraine remained wartime losses, destruction of energy infrastructure, weak exports, labor shortages, high budget dependence on external financing and the structural foreign exchange deficit of the private sector. Positive factors included a significant level of international reserves, the NBU’s controlled policy, continued international support, business adaptability and the state’s ability to fulfill key budget obligations.

The global economy in the first quarter of 2026 remained relatively resilient, but less stable than at the beginning of the year. The IMF forecast global growth of 3.1% in 2026, provided that the conflict in the Middle East remained limited. The United States maintained positive dynamics but faced a new inflationary impulse; the eurozone remained weak in terms of growth rates and again saw inflation above the target; China demonstrated 5% growth; India remained the main driver among large economies; Turkey struggled with high inflation; Brazil maintained moderate, more balanced dynamics.

“March 2026 became a moment for Ukraine to test the real strength of its stabilization model. High reserves, international assistance and the NBU’s controlled policy allow the system to be kept in working condition. But the decline in GDP in the first quarter, accelerating inflation and a large trade deficit show that financial stability alone is not enough. The next stage must be the transition from a survival model to a model of productive recovery. This means investment in energy, the defense-industrial complex, processing, logistics, export production, technologies and human capital. Without this, even significant reserves and external assistance will remain only a safety cushion, not a source of long-term development,” Maksym Urakin concluded.

The monthly analytical and statistical product “Economic Monitoring” is available to clients of Interfax-Ukraine.

Head of the “Economic Monitoring” project, PhD in Economics Maksym Urakin

This article presents key macroeconomic indicators for Ukraine and the global economy as of the end of December 2025. The analysis is based on current data from the State Statistics Service of Ukraine (SSSU), the National Bank of Ukraine (NBU), the International Monetary Fund (IMF), the World Bank, as well as leading national statistical agencies (Eurostat, BEA, NBS, ONS, TurkStat, IBGE). Maksym Urakin, Director of Development and Marketing at Interfax-Ukraine, Candidate of Economic Sciences, Doctor of Philosophy in History, and founder of the Experts Club information and analytical center, presented an overview of current macroeconomic trends that shaped the situation in Ukraine and the world at the beginning of 2026.

Ukraine’s Macroeconomic Indicators

As of the end of January 2026, the Ukrainian economy entered the new year with a combination of two opposing trends: on the one hand—a gradual easing of inflationary pressure, record-high international reserves, and a stable situation in the foreign exchange market; on the other—war risks, high budget dependence on external financing, weak exports, and a structural foreign exchange deficit in the private sector.

According to the NBU’s estimates, Ukraine’s real GDP grew by 1.8% in 2025. This meant that the economy maintained positive momentum for the third consecutive year, but the pace of recovery remained moderate. The NBU attributed this trend to resilient domestic demand, accommodative fiscal policy, business adaptability, and measures to maintain macrofinancial stability. At the same time, physical export volumes declined due to low agricultural inventories, weak external demand for mining and metallurgical products, and constraints related to the electricity shortage at the end of the year.

In January 2026, the disinflationary trend continued. According to data from the State Statistics Service (SSU), as commented on by the NBU, consumer inflation slowed to 7.4% year-on-year, while prices rose by 0.7% month-on-month. Core inflation also declined—to 7.0% y/y. The NBU attributed this trend to a reduction in labor market imbalances, the secondary effects of the high harvests of 2025, competition from certain imported goods, and a stable situation in the foreign exchange market. At the same time, the regulator noted the first signs of increasing pressure from raw food products.

According to Maksym Urakin, January 2026 became an important test for the Ukrainian economy following the conclusion of a challenging 2025. The decline in inflation to 7.4% showed that tight monetary conditions, stabilization of the foreign exchange market, and an improvement in the supply of food products had yielded results. However, in his assessment, this result should not be interpreted as a complete normalization.

“At the beginning of 2026, Ukraine experienced a rare combination for a war economy—inflation was falling, the foreign exchange market remained under control, reserves reached a historic high, and the economy did not lose its positive momentum. However, this does not mean that the country has entered a classic recovery phase. We are dealing rather with a stabilization regime in which many indicators look better thanks to external financing, budget expenditures, business adaptation, and NBU policy. If international aid were removed from this framework or a new severe energy or currency shock were to occur, the system’s stability would once again be in serious doubt,” Urakin noted.

The NBU’s January decision on the discount rate was one of the key signals of the start of the year. On January 29, 2026, the National Bank announced the start of a cycle of monetary policy easing and a reduction in the discount rate from 15.5% to 15.0% effective January 30. The regulator attributed this to a sustained decline in inflationary pressures and a reduction in risks associated with external financing. At the same time, the NBU emphasized that inflation expectations remained relatively high, and a return of inflation to the 5% target is expected only on the policy horizon.

This decision did not signify a shift to a soft monetary policy in the full sense. Real yields on hryvnia-denominated instruments remained positive, and continued interest in hryvnia assets was one of the key factors restraining demand for foreign currency. In its January Inflation Report, the NBU noted that maintaining a high rate in previous months had supported demand for hryvnia-denominated assets, and individuals’ investments in government bonds and deposits in the national currency continued to grow.

“Lowering the discount rate to 15% was a cautious and logical step, but it should not be interpreted as a signal of imminent cheapening of money. Ukraine remains in a state of war, with high budgetary needs and a significant private-sector foreign exchange deficit. Therefore, the NBU is effectively trying to navigate a very narrow corridor: on the one hand, not to stifle economic activity with excessively expensive money, and on the other, not to lose control over inflation expectations and the foreign exchange market. In such a situation, every rate cut should not be a political gesture, but the result of a real easing of risks,” Urakin emphasized.

The external sector remained the main pillar of Ukraine’s macrofinancial stability. As of the end of January 2026, Ukraine’s international reserves rose to $57.7 billion, setting a new all-time high. The NBU attributed the increase in reserves to inflows of external financing, which largely offset the National Bank’s net foreign exchange sales and the country’s foreign currency debt payments.

In its January Inflation Report, the NBU also noted that in 2025, Ukraine received $52.4 billion in international financial support, including $32.7 billion from the EU, $12.0 billion from the U.S., and $3.4 billion from Canada. At the beginning of 2026, reserves stood at $57.3 billion, equivalent to 5.8 months of future imports, and the NBU’s forecast projected an increase in international reserves to $65 billion by the end of 2026 and to $71 billion by the end of 2028.

At the same time, foreign trade remained a weak point. According to customs data, Ukraine’s trade turnover in January 2026 amounted to $9.9 billion: imports – $6.7 billion, exports – $3.2 billion. This meant that the trade deficit remained high, and domestic demand for imports continued to significantly exceed foreign exchange earnings from exports.

“Record reserves are a strong stabilizing factor, but they should not create the illusion of self-sufficiency. Ukraine’s balance of payments continues to rely heavily on foreign aid rather than the economy’s export capacity. When imports more than double exports in merchandise trade, it means that the country is financing a significant portion of current consumption and military needs with external resources. This is justified in wartime, but strategically, such a model cannot be permanent. “In 2026, the key task should be to expand the country’s own foreign exchange base through exports, processing, energy resilience, and investments in production,” Urakin emphasized.

The budget situation at the beginning of 2026 also remained relatively under control, but structurally strained. According to aggregated data on budget execution, in January 2026, state budget revenues amounted to approximately 303.8 billion UAH, while expenditures totaled approximately 286.2 billion UAH. This monthly picture did not negate the overall problem of the year: public finances remained dependent on the regularity of external financing, domestic borrowing, and the government’s ability to maintain confidence in hryvnia-denominated instruments.

The Global Economy

The global economy at the end of January 2026 appeared more resilient than expected at the end of 2025, but this resilience was uneven. In its January update to the World Economic Outlook, the IMF projected global economic growth of 3.3% in 2026 and 3.2% in 2027. The Fund attributed this to investments in technology, fiscal and monetary support, more favorable financial conditions, and the resilience of the private sector. At the same time, the IMF warned of risks associated with overoptimistic expectations regarding the technology sector and a potential escalation of geopolitical tensions.

In the U.S., the economy maintained positive momentum, but the pace slowed by the end of 2025. According to a preliminary BEA estimate, U.S. real GDP grew by 1.4% year-over-year in the fourth quarter of 2025 following a stronger third quarter, and by 2.2% for the full year 2025. Growth was driven by consumer spending and investment, while exports and government spending held back the result. Inflation in the U.S. remained moderately above target: the Consumer Price Index rose by 2.7% from December 2024 to December 2025, and core CPI by 2.6%. On January 28, 2026, the Federal Reserve kept the target range for the federal funds rate at 3.5–3.75%.

The eurozone entered early 2026 with inflation nearly at target but with weak economic momentum. According to Eurostat estimates, annual inflation in the Eurozone stood at 2.0% in December 2025, down from 2.1% in November. Services inflation remained the highest component at 3.4%, while the energy component was negative. ECB rates at the start of 2026 remained at the levels set in 2025: the deposit rate at 2.0%, the main refinancing operations rate at 2.15%, and the marginal lending rate at 2.40%.

The United Kingdom remained one of the most controversial major economies in Europe. According to ONS data, the UK’s GDP grew by 1.3% in 2025, driven in part by the services sector. However, inflation accelerated to 3.4% year-on-year in December 2025, remaining significantly above the Bank of England’s target. In December 2025, the Bank of England cut its base rate to 3.75%, but the decision was passed by a narrow 5–4 majority, indicating that disagreements within the regulator regarding the pace of further easing persisted.

“The global economy at the start of 2026 did not appear to be in crisis, but it could not be described as uniformly strong. The U.S. maintained positive momentum, though no longer at an overheated pace; the eurozone was effectively balancing between low inflation and weak growth; the UK experienced slow growth but still faced elevated inflationary pressures. For Ukraine, this means that external demand is unlikely to become a powerful independent driver of recovery. The global environment tends to create moderately favorable financial conditions, but does not guarantee automatic growth in Ukrainian exports,” noted Maksym Urakin.

China ended 2025 with a formally strong result. According to data from the National Bureau of Statistics of China, the country’s GDP grew by 5.0% in 2025, reaching 140.1879 trillion yuan. The primary sector grew by 3.9%, the secondary sector by 4.5%, and the tertiary sector by 5.4%. At the same time, the inflation picture remained weak: in December 2025, the CPI rose by only 0.8% year-on-year, while core inflation rose by 1.2%. This indicated that the Chinese economy maintained its manufacturing and export strength, but domestic consumer demand remained insufficiently robust.

India, by contrast, remained the main growth driver among major economies. According to the government’s first preliminary estimate, India’s real GDP was projected to grow by 7.4% in the 2025/26 fiscal year, following 6.5% in the 2024/25 fiscal year. Nominal GDP was estimated to grow by 8.0%, with the services sector being the main driver of real GVA. At the same time, inflation remained very low: in December 2025, the CPI stood at 1.33% year-on-year, and food inflation was negative.

At the start of 2026, Turkey remained an example of an economy with relatively high growth but a challenging inflationary legacy. According to TurkStat, inflation stood at 30.89% year-on-year in December 2025 and at 30.65% in January 2026. Subsequent official data from the Turkish Ministry of Trade showed that the country’s economy grew by 3.6% in 2025 and by 3.4% year-on-year in the fourth quarter.

Brazil ended 2025 on a cautiously positive note. According to IBGE data, IPCA inflation in 2025 stood at 4.26%, while the December monthly rate was 0.33%. Brazil’s GDP in 2025 grew by 2.3%, reaching 12.7 trillion reais at current prices. Growth was observed in all three major sectors: agriculture, industry, and services.

“China, India, Turkey, and Brazil clearly demonstrate how diverse the dynamics of major emerging economies have become. China has a large scale and a strong manufacturing base, but its price momentum remains weak. India demonstrates the most compelling combination of high growth and low inflation. Turkey maintains its momentum, but the price of this growth is a very high inflation rate. Brazil is moving more moderately but more balanced. “It is important for Ukraine to view these examples not in the abstract, but practically: in global competition, the economies that win are those capable of simultaneously maintaining macro-stability, a manufacturing base, exports, and domestic investment demand,” Urakin believes.

Conclusions

As of the end of January 2026, Ukraine was in a mode of managed macrofinancial stabilization. Inflation was declining, the discount rate had been cautiously reduced to 15%, international reserves had reached a historic high, and the economy maintained positive growth after the end of 2025. At the same time, this stability remained dependent on three key conditions: regular external financing, a controlled situation in the foreign exchange market, and the state’s ability to sustain domestic demand without triggering a new wave of inflation.

The main risks for Ukraine at the start of 2026 remained war-related losses, energy infrastructure deficits, weak exports, high budgetary needs, dependence on international aid, and a structural labor shortage. A positive factor was that the NBU had record reserves and room for cautious policy easing. A negative factor was that the real production and export base had not yet created sufficient domestic resources for self-sustained recovery.

The global economy was not in a phase of deep crisis at that time. The IMF projected global growth of 3.3% in 2026; the U.S. remained stable, the eurozone stayed close to its inflation target, India demonstrated high growth rates, and China remained a large but structurally mixed source of global demand. At the same time, none of these external factors guaranteed Ukraine a rapid recovery without domestic decisions.

“January 2026 showed that Ukraine is entering the new year not from a position of economic breakthrough, but from a position of maintained manageability. This is important because, in the context of war, the very ability to control inflation, the exchange rate, budget needs, and reserves is already a significant achievement. But the next stage will be more challenging: the country needs to transition from a model of survival and stabilization to a model of productive recovery. This means investing in energy, the defense-industrial complex, processing, logistics, export-oriented industries, human capital, and technology. Without this, even record reserves and foreign aid will remain merely a financial cushion, not a source of long-term growth,” concluded Maksym Urakin.

The monthly analytical and statistical product “Economic Monitoring” is available to Interfax-Ukraine clients.

Maksym Urakin, Head of the “Economic Monitoring” project, Director of Development and Marketing at Interfax-Ukraine, Candidate of Economic Sciences, Doctor of Philosophy in History, and founder of the Experts Club information and analytical center

ECONOMY, EXPERTS_CLUB, MACROECONOMICS, MONITORING, Ukrainian_economy, URAKIN

This article presents key macroeconomic indicators for Ukraine and the global economy as of the end of June 2025. The analysis is based on current data from the State Statistics Service of Ukraine (SSSU), the National Bank of Ukraine (NBU), the International Monetary Fund (IMF), the World Bank, and leading national statistical agencies (Eurostat, BEA, NBS, ONS, TurkStat, IBGE). Maksim Urakin, Director of Marketing and Development at Interfax-Ukraine, Candidate of Economic Sciences and founder of the Experts Club information and analytical center, presented an overview of current macroeconomic trends.

Macroeconomic indicators of Ukraine

Ukraine ended the first half of 2025 in a state of moderate but fragile stabilization. After a “flat” start to the year and a weak first quarter, which the NBU assessed as a period of subdued activity, in April-June the economy maintained positive momentum primarily due to domestic consumption and sectors that adapted to military logistics. In its April decision, the NBU kept the policy rate at 15.5%, emphasizing the need to support currency stability and reduce inflation expectations; in its July decision, the regulator confirmed this level, which anchored rates for hryvnia instruments.

Inflation slowed significantly: in June, the annual rate fell to 14.3% y/y (from 15.9% in May), reflecting a combination of tighter monetary policy, currency stability, and price adjustments for certain food groups; the monthly rate was +0.8%. This is the first significant “dip” in annual inflation below 15% this year.

Foreign trade remains the main source of imbalances. In January–May, exports of goods amounted to about $16.95 billion, imports to $31.54 billion, and the negative balance deepened to $14.6 billion (+49% y/y). The key drivers of imports were energy, machinery, and chemicals; exports were structurally biased toward food and raw materials.

Against the backdrop of the trade gap, international reserves remained an important buffer. As of July 1, 2025, they reached $45.1 billion (+1.2% in June) thanks to large inflows from partners (in particular, the EU, Canada, and the World Bank), which exceeded FX interventions and debt payments. This is a historically high level for Ukraine and a critical safety margin for the currency market.

“Current growth is supported by consumption and official financing; without the launch of an investment cycle, it will remain low and unsustainable. International reserves are a stabilization tool, not a source of development; the effect will only appear after they are converted into value-added projects. The trade deficit, in turn, is structural in nature: it should be addressed through logistics, energy modernization, and localization of production, not just exchange rate decisions,” said Maksim Urakin.

The debt burden has increased. As of June 30, 2025, the total public and publicly guaranteed debt was estimated at approximately $184.8 billion (equivalent to UAH 7.697 trillion), adding nearly $3.9 billion in a month. External liabilities structurally prevail, which increases dependence on official financing.

International support remained systemic. On June 30, the IMF completed the eighth review of the EFF program and approved further financing (total payments under the program exceeded $10 billion), while confirming Ukraine’s fulfillment of key criteria and continuation of structural reforms.

“The second quarter showed that the economy has learned to operate in a mode of constant shocks — we see the resilience of small and medium-sized businesses, the flexibility of logistics, and the rapid reorientation of exporters. But the fundamentals remain unchanged: the investment cycle has not been launched, and the trade deficit is structural; it will not disappear without a targeted industrial policy and incentives for localizing production. The discount rate of 15.5% is a compromise between the price of money and currency stability; it works as long as official financing enters the country. If we want to get out of “survival mode,” we need long-term money to restore energy, logistics hubs, and high-tech production. Reserves of over $45 billion are not a reason to relax, but a window of opportunity that must be converted into value-added projects, otherwise exchange rate stability will remain expensive and temporary,” Maksim Urakin emphasized:

Global economy

The world moved unevenly in the first half of 2025. After a technical contraction in the first quarter (-0.5% SAAR, -0.1% q/q), the US entered the second quarter with a recovery in demand: by the end of June, there were already signs of easing price pressure on the PCE index (≈2.5% y/y in May) and stabilization of household spending. Later official estimates show a significant rebound in the second quarter, but as of June 30, the key picture was “cold” demand amid high interest rates.

The eurozone showed a contrast: after a strong Q1 (+0.6% q/q), momentum moderated in April–June; preliminary estimates show Q2 added +0.1% q/q. The factors were weak external conditions, a correction in industry, and cautious consumers, despite easing inflation. The UK remained a positive exception among the G7: +0.7% q/q in Q1 and +0.3% q/q in Q2, although inflation accelerated to 3.6% y/y in June, slowing down the pace of monetary policy easing.

China maintained a pace close to its official target: GDP +5.2% y/y in Q2 (after +5.4% in Q1), but inflation remained sluggish — June CPI +0.1% y/y, reflecting weak domestic consumption and pressure from real estate. Exports and industrial production drove growth, but the question of the sustainability of domestic demand remained open.

Turkey grew by 2.0% y/y in Q1; inflation in June fell to ≈35% y/y, demonstrating the effect of protracted disinflation despite high rates and a cool business cycle.

India remained the most dynamic major economy: in Q4 of fiscal year 2024/25, real GDP grew by 7.4% y/y, and by 6.5% for the year as a whole; inflation in June came close to ≈2% y/y (according to MoSPI publications), creating room for cautious policy easing going forward.

Brazil added +1.4% q/q (2.9% y/y) in Q1 on the back of strong agriculture; the IPCA in June was 5.35% y/y (+0.24% m/m), remaining above the central bank’s target and forcing monetary authorities to act cautiously.

“Global growth in the first half of 2025 is a mosaic of different speeds. The US is balancing between tight rates and the desire not to ”overbrake” demand, Europe is slowly emerging from stagnation, China is holding the bar thanks to exports, but domestic demand has not yet recovered. For Ukraine, this means one simple thing: we should not expect external demand to pull us out of the doldrums on its own. We need targeted industrial programs, support for high value-added exports, and a transparent import substitution policy where it makes economic sense. Then, even amid global turbulence, we will be able to turn record reserves and international support into a long investment cycle and a new economic structure,” Maxim Urakhin concluded.

At the end of June 2025, Ukraine’s economy remains in a state of controlled equilibrium: inflation is slowing, reserves are at historic levels, and monetary policy is predictable. At the same time, a deep trade deficit, high debt burden, and weak investment flows remain key risks that require immediate responses — from tax and customs policy to incentives for localizing production and restoring critical infrastructure.

Head of the Economic Monitoring project, Candidate of Economic Sciences Maksim Urakin

Source: https://interfax.com.ua/news/projects/1113998.html

Industrial production in Ukraine increased by 3.2% in July 2025 compared to July last year. This is the second consecutive month of growth: in June, the indicator rose by 2.9%, while in May and April, a decline was recorded, according to the State Statistics Service.

In January-July 2025, the total volume of industrial production was 3% lower than in the same period of 2024. The decline in the extractive industry was 11.1%, and in the production of coke and petroleum products, 6.3%.

The volume of industrial products sold over seven months reached UAH 2,296.5 billion, of which UAH 406.4 billion was accounted for by exports.

The main industries that showed growth in July compared to last year were:

– pharmaceuticals — +23.6%;

– furniture manufacturing — +22%;

– rubber and plastic products manufacturing — +12.7%;

– electricity, gas, and steam supply — +10.2%;

– woodworking — +8.4%;

– food industry — +3.4%;

– coke production — +2.5%;

– electrical equipment — +1.8%;

– automotive industry — +0.5%;

– oil and gas production — +0.4%.

At the same time, there was a decline in:

– coal mining — by 1.6%;

– metal ore mining — by 7.7%;

– textile manufacturing — by 7.1%;

– computer and electronics manufacturing — by 6%;

– metallurgy — by 0.8%;

– mechanical engineering — by 0.1%.

Interestingly, the mining and quarrying segment recorded growth of 49.1%.

Compared to June 2025, industrial production in July increased by 0.6%.

In 2024, industrial production in Ukraine grew by 4.6%.

According to Maxim Urakhin, co-founder of the Experts Club analytical center, July’s growth shows that Ukraine’s industry is gradually adapting to military conditions and external challenges:

“We are seeing a local recovery in pharmaceuticals, wood processing, and energy. These are the sectors that respond most quickly to domestic demand and the needs of the economy. However, the decline in metallurgy and mining reminds us of structural problems: export-oriented industries continue to suffer from logistics and declining global demand. By the end of the year, industry may show a moderate recovery, but investment in modernization and expansion of export routes is necessary to achieve sustainable growth,” Maxim Urakin noted.

Brazil’s Ministry of Finance has raised its GDP growth forecast for 2025, but expects the economic upturn to slow down as a result of the country’s central bank’s tight monetary policy.

The GDP growth forecast for the current year has been raised to 2.5% from the 2.4% expected in May, and for 2026 it has been lowered to 2.4% from 2.5%.

The forecasts do not take into account the consequences of Washington’s introduction of 50% tariffs on all imports from Brazil, the Ministry of Finance notes. Earlier, US President Donald Trump announced that these tariffs would take effect on August 1.

“The tariffs are unlikely to have a significant impact on GDP growth in 2025, although certain industries may suffer quite severely,” the Ministry of Finance said in a statement.

In the first quarter of this year, Brazil’s GDP increased by 1.4% compared to the previous three months, the highest in three quarters. GDP growth in annual terms was 2.9%.

Earlier, the Experts Club information and analytical center made a video analysis of the prospects for the Ukrainian and global economies. For more details, see the video at https://youtu.be/kQsH3lUvMKo?si=F4IOLdLuVbYmEh5P

In the first half of 2025, the Ukrainian economy demonstrates fragile but positive growth, despite the difficult external environment and high dependence on international financial support. This is stated in an analytical review published by the Experts Club information and analytical center on YouTube.

“We are seeing a cautious but still positive signal: Ukraine’s economy is growing, albeit very slowly. The National Bank forecasts GDP growth of 2.5-3.1% in 2025. This is above the survival line, but not enough for a full recovery,” said Maksym Urakin, PhD in Economics and founder of Experts Club.

“Inflation remains at 12-13%, which continues to reduce the purchasing power of the population. Despite the NBU’s moderate monetary policy, the pressure on households remains,” the economist explained.

The situation in foreign trade also remains alarming. In May 2025, the trade deficit in goods and services reached $4.1 billion. Imports amounted to $7 billion, while exports were only $3.4 billion. Trade in services also has a negative balance – $1.8 billion against $1.3 billion.

“The structure of exports shows changes. Supplies of pharmaceuticals, wood and live animals are growing, but grain exports have fallen by almost a quarter. And this is even before the loss of possible EUR 3.5 billion in revenues due to the end of EU customs privileges,” emphasizes Urakin.

At the same time, Ukraine’s international reserves have increased – as of June 1, they amounted to $44.54 billion. This is more than at the end of 2024, although it is 4.6% less than in April. But the public debt, according to Urakin, remains critically high – $179.2 billion (about 94% of GDP), of which more than $134 billion are external liabilities.

“The reserves are currently sufficient to stabilize the exchange rate and payments. But this is a resource that cannot be exhausted indefinitely. Ukraine remains critically dependent on international assistance – from the IMF, the EU and other partners,” he emphasized.

The global economy, according to the IMF and the World Bank, is expected to show the slowest growth in the last decade in 2025, at 2.3-2.8%. Inflationary pressures, trade disputes, and geopolitical instability are limiting the potential for global recovery. The Bank for International Settlements describes the situation as a “turning point” due to protectionism, declining productivity, and demographic risks.

The United States recorded its first decline in GDP since 2022, down 0.5% year-on-year in the first quarter. The main reasons are weakening consumer demand and declining exports. However, the Atlanta Fed predicts a recovery – 2.5% growth in the second quarter. PCE inflation is 3.1%, core inflation is 2.6%, and the Fed’s key policy rate remains at 5.25-5.5%.

In China, the economy grew by 5.4% in the first quarter. However, the official PMI in June remained below the 50 mark (49.7), indicating instability in the industry. Meanwhile, the private Caixin PMI exceeded 50 for the first time in several months.

The Eurozone is showing signs of stabilization: in the first quarter, GDP grew by 0.6% y-o-y, inflation in June was exactly 2%, i.e. within the ECB’s target. Manufacturing indices are also improving. Germany is still feeling the effects of the last recession. The GDP growth forecast is only 0.3-0.4%, although the manufacturing PMI has exceeded 50 for the first time since 2022. Retail trade, however, remains weak.

The UK surprised with positive dynamics – 0.7% growth in the first quarter, the highest among the G7. Inflation in May was 3.4%, with the Bank of England’s key policy rate at 4.25%.

India continues to lead the way in terms of growth – 7.4% in the first quarter. Inflation was only 2.82%. The central bank cut its key policy rate to 5.5% in response to lower inflationary pressures.

Brazil is expected to grow at 2.1-2.4%, but inflation in May was 5.32%. This forced the regulator to maintain the high Selic rate of 15%.

Japan is showing the first signs of recovery. The PMI in industry reached 50.1, and the composite PMI – 51.4. Inflation in services is 3.3%, and the Bank of Japan may raise rates as early as 2026.

“The global economy is in a turning point. The US and Europe are stagnating, while China is recovering cautiously. Germany and the UK are showing weak but stable growth. India remains the engine of global development. For Ukraine, the main thing is not to lose momentum, maintain access to international financing and adapt to the new conditions of global trade,” summarized Maksym Urakin.

The material was prepared based on the analytical review by Experts Club. Watch the video for more details at the link: https://www.youtube.com/watch?v=kQsH3lUvMKo&t

You can subscribe to the Experts Club YouTube channel here: https://www.youtube.com/@ExpertsClub