Державна прикордонна служба України попереджає про можливі технічні перерви в роботі пропускних пунктів на кордоні з Польщею, Словаччиною та Угорщиною 7 березня з 8:00 до 22:00.

“7 березня 2023 року з 8:00 до 22:00 можливі технічні перерви під час пропуску пасажирів на кордоні. Оновлюватимуть інформаційні системи, що використовуються в прикордонному контролі на зовнішніх кордонах”, – таке оголошення розміщено на офіційній сторінці Держприкордонслужби в понеділок із проханням враховувати цю інформацію під час планування поїздки.

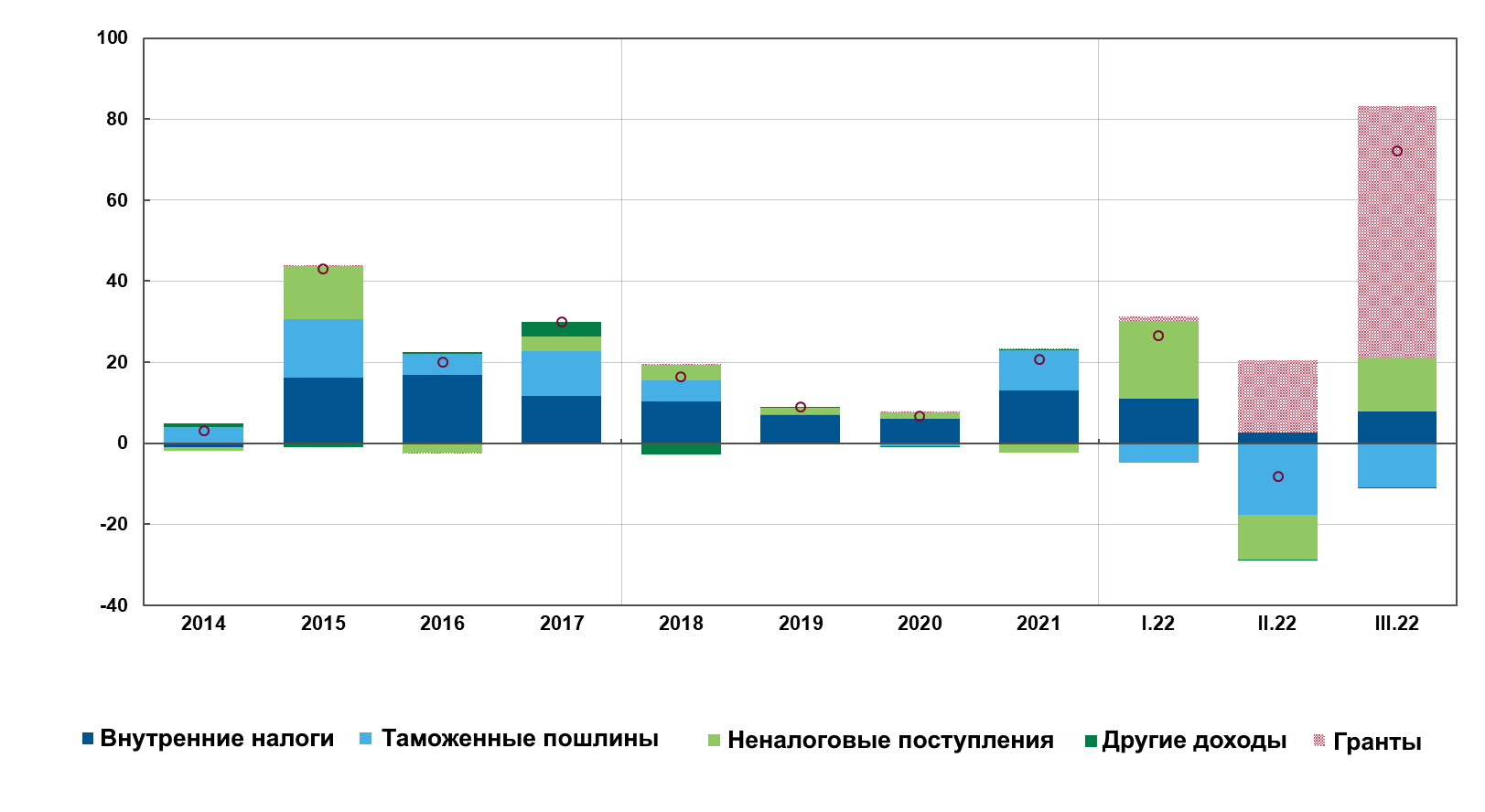

Зміна доходів зведеного бюджету у 2014-2022 році (%)

Джерело: Open4Business.com.ua та experts.news

Кабінет міністрів призначив голову Державної інспекції архітектури та містобудування Семена Кривоноса на посаду директора Національного антикорупційного бюро України (НАБУ).

Таке рішення ухвалено на позачерговому засіданні уряду в понеділок.

Крім Кривоноса, на засіданні розглядали кандидатури Сергія Гупяка та Романа Осипчука, які також були передані в уряд за результатами проведеного конкурсу.

“Отримавши всі необхідні матеріали комісії з відбору, уряд уважно вивчив ці матеріали по кожному кандидату, провів особисте знайомство з кожним кандидатом у рівних умовах”, – зазначив прем’єр-міністр Денис Шмигаль.

Водночас він підкреслив, що із зазначеним призначенням Україна виконала всі сім рекомендацій, висунутих під час набуття країною статусу кандидата в члени Євросоюзу, а також повністю сформувала антикорупційну інфраструктуру.

Згідно з розпорядженням уряду №192 від 6 березня, Кривоноса призначено директором НАБУ строком на сім років.

Український онлайн-рітейлер Rozetka почав роботу в Польщі, повідомив співзасновник Rozetka Владислав Чечоткін.

“Rozetka розпочала роботу в Польщі. Поки що в тестовому режимі: перевіряємо всі процеси, наповнюємо асортиментом сайт, налагоджуємо всі логістичні ланки”, – повідомив він у фейсбук.

Чечоткін зазначив, що в роботі розраховують як на велику українську аудиторію (у Польщі проживають понад 2 млн українців), так і на місцеву.

“Дякую ЗСУ за те, що це в принципі можливо! За те, що через рік після початку повномасштабної війни ми не тільки вистояли, а можемо розвивати бізнес. І всім нашим клієнтам, для яких ми залишилися “щоразу те, що треба”, – зазначив він.

Онлайн-магазин електроніки та побутової техніки Rozetka був заснований 2005 року в Києві Владиславом та Іриною Чечоткіними. У наступні роки компанія трансформувалася в мультикатегоричний онлайн-маркетплейс. У грудні 2022 року відвідуваність Rozetka становила 40 млн осіб на місяць.

ПрАТ “Сентравіс Продакшн Юкрейн” (Centravis Production Ukraine), що входить до холдингу Centravis Ltd., вивело основне виробництво в Нікополі на повну потужність і наприкінці лютого офіційно відкрило свою філію з випуску труб в Ужгороді.

“Зараз виробництво “Сентравіс” працює на повну потужність. Усе обладнання працює, працюють гарячий і холодний цехи”, – написав директор з продажу (chief sales officer, CSO) Артем Атанасов у листі клієнтам минулої п’ятниці.

За його словами, команда логістики компанії постійно контролює найбезпечніші способи доставки готової продукції споживачам. Офіси продажів по всьому світу працюють в Ессені, Мілані, Кракові, Лугано, Х’юстоні та Дубаї.

Також повідомляється, що в Ужгороді 28 лютого відбулося офіційне відкриття нового виробничого майданчика “Сентравіс”, на якому були присутні менеджери з Італії, Німеччини, Польщі, США та ОАЕ, місцева та регіональна влада.

“Цей виробничий майданчик є лише частиною нашої великої команди, оскільки основні потужності “Сентравіса” залишаються в Дніпропетровській області. Ми дуже щасливі, що наше виробництво розвивається і українські нержавіючі безшовні труби користуються попитом в усьому світі”, – наголошується в інформації директора з продажу.

Як повідомлялося, холдинг Centravis Ltd. перереєстрував свою материнську компанію у Швейцарії, змінивши кіпрську дислокацію, що допоможе підвищити кредитний рейтинг і залучити довші та дешевші кошти на розвиток виробництва в Україні.

“Сентравіс” раніше заявив про плани відкрити на Закарпатті спеціалізоване виробництво інструментальних труб для автомобілів.

“Сентравіс” входить до десятки найбільших виробників безшовних нержавіючих труб у світі. У 2022 році компанія реалізувала низку масштабних замовлень для таких світових компаній, як Benteler Automotive, LINSTER Edelstahlhandel, Rohr Mertel, Buhlmann Group, Webco, MRC. На підприємстві працює понад 1400 осіб.

Заснований у 2000 році “Сентравіс” – один з найбільших світових виробників безшовних нержавіючих труб. Його виробничі потужності розташовані в Нікополі (Дніпропетровська обл.).

Холдинг Centravis Ltd. створено на базі ЗАТ “Нікопольський завод нержавіючих труб”, сервісних і торгових компаній ТОВ “Виробничо-комерційне підприємство “ЮВІС”. Його акціонерами є члени сім’ї Атанасових.

У власності Centravis Ltd. перебуває 100% акцій ПрАТ “Сентравіс Продакшн Юкрейн”.

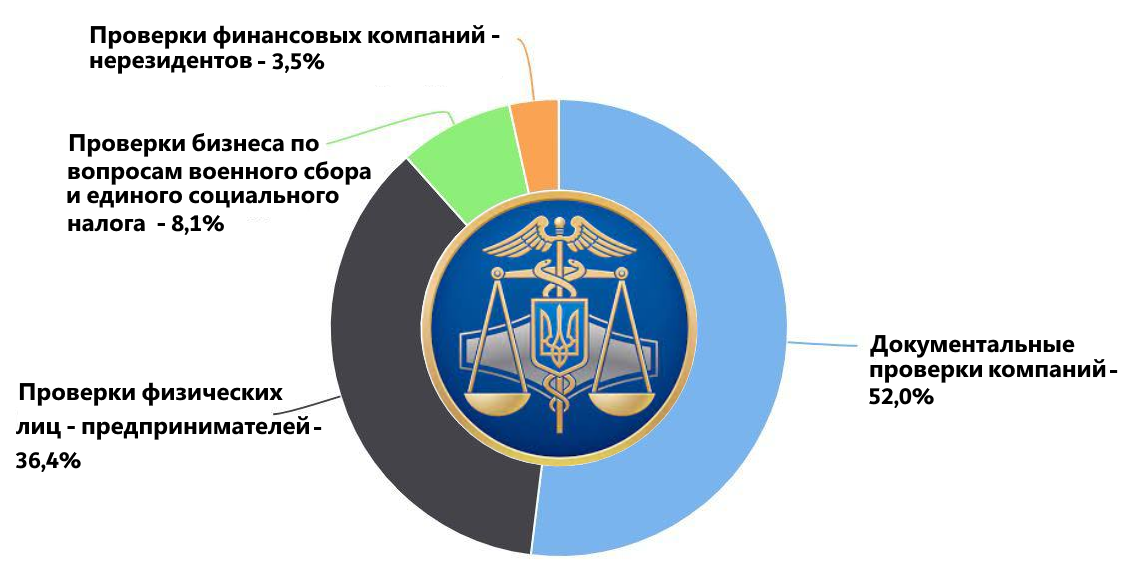

Заплановані перевірки бізнесу державною податковою службою у 2023 р.

Джерело: open4business.com.ua та experts.news