According to The Serbian Economist, a contract has been signed in neighboring Romania for the design and construction of a pedestrian suspension bridge across the Rebra River valley near the commune of Parva in Bistrița-Năsăud County, Transylvania.

The future bridge will be approximately 620 m long. It will span the Rebra Valley and connect two mountain slopes near the entrance to the Rodna Mountains National Park. According to Romanian media reports, the bridge will be 200–300 m above the valley.

The project could become one of the highest pedestrian suspension bridges in Europe and one of Romania’s new tourist attractions.

The project is funded, in part, by European funds under the Nord-Vest 2021–2027 regional program.

In addition to the bridge itself, the project includes the development of tourism infrastructure, specifically access to the site and landscaping of the surrounding area. In particular, Romanian publications mention the reconstruction of Dealul Tisei Street.

https://t.me/relocationrs/3055

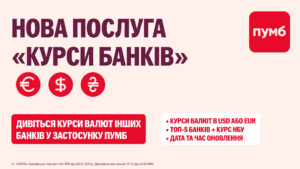

PUMB continues to expand its digital services in the mobile app and is launching a new feature for customers—“Bank Exchange Rates”. From now on, users can view currency exchange rates from other banks directly in the PUMB app and make financial decisions more quickly.

The new service allows users to access up-to-date information about the currency market in one place without having to visit third-party websites or open other banks’ apps.

Now, it takes just a few clicks in the PUMB app to compare exchange rates and assess the current market situation.

All the information you need—on a single screen

The “Bank Exchange Rates” service provides information on:

– exchange rates for USD and EUR;

– exchange rates from Ukraine’s top 5 banks;

– the official NBU exchange rate;

– the date and time of the last data update;

– the information source—kurs.com.ua.

This allows customers to quickly compare offers from different banks and get a sense of the current market situation.

Where to find the new service

The new service is available in the PUMB app under the following sections:

– “Payments”;

– “Currency Market.”

After navigating to these sections, the “Exchange Rates in Banking Apps” screen opens, displaying up-to-date information on market exchange rates.

More Convenience for Customers

FUIB continues to develop the app’s currency features so that customers can access as much useful information and services as possible in one place.

Now exchange rates from other banks are available directly in the PUMB app.

No searching. No redirects. No extra tabs.

Just open the app—and all the information you need is right at your fingertips.

PUMB—the bank that’s always in your best interest!

According to Fixygen, PJSC “Insurance Company ‘Peremoha’” will hold a general meeting of shareholders virtually on June 26, 2026, as reported in the SMIDA system on June 10.

Details of the agenda are provided in the issuer’s announcement.

PJSC “Insurance Company “Peremoha” previously operated under the name PJSC “Insurance Company “Mir.” The company is registered in Kyiv and specializes in property and casualty insurance.

According to previously published data, the company’s ownership structure included LLC “ABC Finance” with a 79.9% stake and Volodymyr Babko with a 13.299% stake.

PJSC “Electrometallurgical Plant ‘Dniprospetsstal’” (Zaporizhzhia) and Zaporizhzhia Electric Power Supply LLC have reached a settlement agreement to repay the consumer’s electricity debt in the amount of 89,986,568 thousand UAH for the period from January 1 to February 5, 2026.

According to court documents in Case No. 908/1091/26, copies of which are available to the “Interfax-Ukraine” agency, on May 4, 2026, the Commercial Court of Zaporizhzhia Oblast received a statement of claim from ‘Zaporizhzhiaelektropostachannya’ LLC against “Dniprospetsstal” with the participation of JSC “Zaporizhzhiaoblenergo,” seeking recovery of debt for consumed electricity in the amount of 89,986,568 thousand UAH, of which 85.398 million UAH is principal debt plus 3% per annum and the inflation index.

Following a series of hearings, at the court session on June 3, representatives of the parties to the case supported a joint statement by the parties approving the settlement agreement dated May 26, concluded between Zaporizhzhia Electric Power Supply LLC and Dniprospetsstal PJSC. The court granted the motion to approve the settlement agreement, under which the defendant acknowledges that its debt for electricity consumed during the period from January 1 to February 5, 2026, amounts to 87,986,568 thousand UAH and undertakes to repay it in several installments.

Within three calendar days of the lifting of the provisional measures ordered by the Commercial Court’s ruling of May 19, 2026, in Case No. 908/1091/26, the defendant shall pay the plaintiff 50 million UAH.

Payment of the remaining principal debt in the amount of 37,986,568 thousand UAH will be made according to the following schedule: 18,993,284 thousand UAH by June 30, 2026; a similar installment by July 30, 2026.

On this basis, the court, by a ruling dated June 3 and published on June 8 of this year, closed the case.

In another case, No. 908/1844/25, the Zaporizhzhia Regional Commercial Court, by a ruling dated June 11 of this year and published on June 12, partially granted the motion “Dniprospetsstal” to defer enforcement of the decision regarding the recovery, in favor of the Zaporizhzhia City Council, of lost revenue from the use of a land plot without title documents for the period from July 14, 2020, to February 28, 2025, in the amount of 3,661,675 thousand UAH, taking into account the outstanding balance as of June 11, 2026, in the amount of 3,138,578 thousand UAH.

The company must repay the debt within five months, making equal monthly payments of 627,715 thousand UAH.

As previously reported, in the first quarter of 2026, “Dniprospeztal” saw its losses increase 3.9-fold compared to the same period in 2025—to 510.751 million UAH. Uncovered losses as of the end of March 2026 amounted to 6 billion 775.516 million UAH.

The company’s net loss in 2025 increased by 22.1% compared to 2024—to 711.015 million UAH from 582.427 million UAH. As of December 31, 2025, the company’s workforce numbered 2,814 thousand people (in 2024—3,147 thousand people).

“Dniprospetsstal” is Ukraine’s sole manufacturer of long products and forgings made from special steel grades: stainless steel, tool steel, high-speed steel, bearing steel, structural steel, as well as heat-resistant nickel-based alloys.

According to the National Securities Commission’s data for the first quarter of 2026, its shares are held by Wenox Holdings Ltd. (47.1128%), Boundryco Ltd. (11.0131%), Gazaro Ltd. – 16.5197%, Crascoda Holdings – 6.6826%, and Middleprime Limited – 9.7901% (all based in Cyprus).

It was previously reported that in May 2008, the international investment and consulting group EastOne sold its approximately 30% stake in Dniprospetsstal, which had previously been held under the group’s mandate. The plant’s new shareholders are linked to VS Energy International, whose beneficiaries include several Russian entrepreneurs.

According to the report, in May 2023, pursuant to a decision by the National Security and Defense Council of Ukraine (NSDC) dated May 12, 2023, personal economic sanctions were imposed on the ultimate beneficial owner of PJSC “Dniprospetsstal.”

The authorized capital of the PJSC amounts to 49.720 million UAH.

COURT, DEBT, DNIPROSPETSSTAL, ELECTRICITY, electricity supply, Zaporizhzhia

Since the start of Russia’s full-scale invasion, the Food and Agriculture Organization of the United Nations (FAO) has allocated $176.7 million to support Ukraine’s agricultural sector, with priorities including demining and training for agribusiness development, according to Shakhnoza Muminova, head of the FAO office in Ukraine.

“From 2022 to the present, FAO, together with its partners, has allocated $176.7 million to support approximately 300,000 families in rural areas and 17,000 farmers,” she told the Interfax-Ukraine news agency on the sidelines of the Agro Ukraine Summit on Wednesday.

According to Muminova, one of the most underfunded yet most critical areas remains the humanitarian demining of agricultural land.

“First and foremost, mine action requires significant funding because it is expensive. Ukraine currently has the world’s largest area of contaminated agricultural land. If this sector is underfunded, demining could drag on for several decades. And we want to return the land to production as soon as possible,” she noted.

The head of the FAO office reported that currently 133,000 square kilometers of Ukraine’s territory require surveying and are at risk of being contaminated with explosive ordnance.

According to her, the FAO’s work in Ukraine focuses on several key areas: supporting families and farmers in rural areas, as well as providing technical support to the government. Particular attention is being paid to surveying potentially contaminated areas and providing vouchers to resume agricultural activities on cleared plots.

Muminova also highlighted the lack of funding for training and agribusiness development programs.

“The Ukrainian agricultural sector is currently experiencing a significant exodus of people due to the hostilities. Many people are leaving, and the agricultural sector is suffering greatly as a result. Therefore, training remains one of the key areas in need of support,” she explained.

According to the FAO representative, the organization plans to provide support to an additional 240,000 households and farmers between 2026 and 2028. To implement this plan, the FAO needs to raise $193 million, but the initiative remains underfunded at this time.

“What strikes me most is that people do not want to leave their homeland, even if it is dangerous,” Muminova added.

The Ostchem nitrogen holding company, which brings together Group DF’s nitrogen business enterprises, has resumed seaborne exports of urea for the first time in seven years, Group DF’s press service reported on Wednesday.

“Ukraine has resumed seaborne exports of urea: for the first time in seven years, products from Ukrainian chemical manufacturers were shipped via sea,” the company emphasized.

According to the statement, a shipment of products manufactured by the Ostchem Group was exported through the port of Chornomorsk to international buyers in the Mediterranean region.

The total volume of the shipment was approximately 21,000 metric tons. The main export destinations were Italy and Turkey.

Among the buyers of Ukrainian urea were the U.S.-based Nitron Group and the South Korean Samsung C&T Corporation.

Group DF noted that the resumption of maritime exports occurred against the backdrop of a gradual stabilization of logistics chains and growing interest from international traders in Ukrainian products. A portion of Ostchem’s products also continues to be sold to European industrial consumers via land-based logistics routes.

The company is also in negotiations regarding new export shipments with a number of international traders and industrial consumers.

As previously reported, in April 2026, the plants of the Ostchem nitrogen holding began production of a new nitrogen fertilizer—AMS30 ammonium nitrate.

Ostchem is the nitrogen holding company of Dmitry Firtash’s Group DF, which brings together the largest producers of mineral fertilizers in Ukraine. Since 2011, it has included “Rivneazot” and Cherkasy-based “Azot,” as well as Severodonetsk-based “Azot” and “Styrol,” which are currently inactive and located in occupied territories.