On June 6, the Silpo chain opened a new supermarket in the Kyiv region (village of Myrotske, 4 Shlyakhova St.) in a biker loft style; MOTO FEST by Silpo is scheduled to take place in the store’s parking lot on June 13, the chain’s press service told Interfax-Ukraine.

The new supermarket covers an area of 1,639 square meters and is open from 8:00 a.m. to 11:00 p.m. The “Silpo” sign mimics the outline of a motorcycle: a seat, a wheel with a stand, handlebars, and a headlight that glows at night, with graffiti featuring flames behind it. Interior details include a horse made of metal wire, a motorcycle with wheels made of pineapple rings and a headlight made of a pumpkin, and more. A special place here is occupied by a panel made of leather jackets painted with bikers’ creeds. The sketches and paintings for them were created by artist Oleksii Bondarenko, co-author of the mural “VOLIA.” At the entrance stands a column of rock posters, and the checkout lightboxes are designed in the shape of spiked wheels.

The “Silpo” team announced a motorcycle festival with an extreme riding show for June 13.

Silpo-Food LLC, which operates the Silpo chain, was established in early August 2016. According to information on the website, the chain operates 311 supermarkets in 60 cities across Ukraine and four Le Silpo delicatessens: in Kyiv, Dnipro, Kharkiv, and Odesa.

The founder of the LLC is PJSC “Retail Capital” (100%, Kyiv), a closed-end, non-diversified venture corporate investment fund. The ultimate beneficiary is Volodymyr Kostelman.

Silpo-Food’s revenue for 2025 increased by 13.97% compared to 2024, reaching UAH 106.013 billion, while net profit amounted to UAH 1.205 billion, compared to UAH 154.1 million for the same period the previous year.

It is part of the Fozzy Group, a commercial and industrial group with more than 825 retail outlets throughout the country. The company operates retail chains of various formats: Silpo supermarkets, Fozzy wholesale hypermarkets, Fora neighborhood stores, Thrash! discounters, Bila Romashka pharmacy supermarkets, and others.

According to Serbian Economist, a project to build a large resort on the Albanian coast linked to Jared Kushner and Ivanka Trump has faced protests and environmental criticism due to its proximity to protected natural areas inhabited by flamingos, sea turtles, and other species.

The project in question is a tourism development on Albania’s Adriatic coast, in the area of Vlorë, Sazan Island, and the Vjosa-Narta zone. Thousands of Albanian residents took to the streets in Tirana to protest against a resort complex worth approximately EUR 1.4 billion linked to Jared Kushner’s investment firm, Affinity Partners. The project involves the creation of a luxury tourist complex on one of the most valuable stretches of the Albanian coast.

Environmentalists’ main concerns stem from the fact that construction could impact natural areas near the Narta Lagoon and the Vjosa-Narta region, which is considered a critical habitat for migratory birds and other species. Activists point out that the region is home to pink flamingos, seals, and sea turtles, and that large-scale development could damage coastal ecosystems.

BirdLife International stated that work related to the resort threatens one of Europe’s most important coastal habitats. The organization claims that construction and preparatory work could damage areas critical for biodiversity and migratory birds.

The protests have been dubbed the “flamingo revolution” by Albanian and international media. Protesters are using flamingos as a symbol of the protection of the natural area. According to media reports, the protests intensified after fences and construction equipment appeared on part of the site, as well as following reports of clashes between activists and security guards.

Albanian Prime Minister Edi Rama defends the project, stating that it is important for the development of high-end tourism and attracting foreign investment. According to Reuters and AP, authorities view the development as part of a strategy to transform Albania into a more prominent destination for premium tourism on the Adriatic.

Critics, for their part, point to the need for greater transparency, environmental impact assessments, and public debate. At the heart of the controversy are not only flamingos and sea turtles, but also a broader question: can Albania develop luxury tourism without losing natural areas that are themselves part of the country’s tourist appeal?

The project has also taken on a political dimension due to its connection to the family of U.S. President Donald Trump. Jared Kushner is his son-in-law, and Ivanka Trump has publicly supported the idea of developing a tourism project in Albania. At the same time, international media emphasize that this is a private development project linked to Kushner’s investment firm, not a U.S. government project.

For Albania, the conflict surrounding the resort has become a test for its entire model of tourism development. The country is actively promoting the Adriatic and Ionian coasts as an alternative to the more expensive Mediterranean markets, but the growth in investment is increasing pressure on natural areas, infrastructure, and local communities.

The United Arab Emirates has taken first place globally in terms of real estate market investment attractiveness, ahead of the United States and the United Kingdom, according to data from the Arada UAE Property Investment Index.

The study was conducted by the American Penta Group on behalf of the developer Arada from April 1 to 23, 2026. The survey included 689 investors from 12 key markets who have an annual income of over $100,000 and more than $250,000 in investment assets, and who have already invested or are interested in investing in real estate outside their home country.

According to the index, 56% of global investors expressed serious interest in the UAE real estate market. This is the highest figure among all markets included in the study. The U.S. received 54%, the UK 41%, France 28%, and Spain 27%.

Investor awareness of opportunities in the UAE real estate market reached 51%, which is comparable to the UK and close to the US. Arada notes that this confirms the UAE’s emergence as one of the most recognizable global centers for real estate investment.

Interest in the UAE is particularly high among investors from neighboring and rapidly growing markets. 91% of Indian investors, 92% of Egyptian investors, and 85% of Saudi respondents named the UAE as one of the three most attractive destinations for investment. Among European investors, the UAE has become the top overseas destination for the French (63%), Germans (60%), and Swiss (57%).

Investors cited the potential for high returns as the main factor driving the UAE’s appeal: 38% of respondents selected this criterion. For Australian investors, this figure reached 57%, for Spanish investors—56%, and for British investors—41%.

Security and stability were key factors for 65% of Chinese and 58% of German investors. Another 34% of all respondents cited the ease of purchasing and owning real estate as an important advantage; among investors from Saudi Arabia, this figure was 57%, and from Egypt, 41%.

Arada Group CEO Ahmed Al-Khoshaibi stated that the survey results confirm trends the company observes in its own sales: international investors increasingly note the maturity of regulations, economic stability, and the resilience of the UAE market even amid external challenges.

“The UAE has repeatedly demonstrated its ability to adapt faster than almost any other market in the world,” he noted.

The release of the index coincided with the announcement of major infrastructure investments in the UAE, including the 34-billion-dirham Dubai Metro Gold Line project, the launch of the first commercial air taxi network, and a 6-billion-dirham federal road corridor to improve connectivity between the emirates.

For the real estate market, this signals continued interest from international capital, despite signs of a cooling in certain segments following several years of rapid growth. Investors continue to view the UAE as a market offering a combination of returns, tax efficiency, stable regulation, and a relatively straightforward property ownership process.

Arada is a development company founded in 2017 in the UAE. The company carries out projects in real estate, retail, education, healthcare, fitness, wellness, and the hospitality sector. Arada’s project portfolio exceeds 130 billion dirhams; the company is also expanding its operations in the UK and Australia.

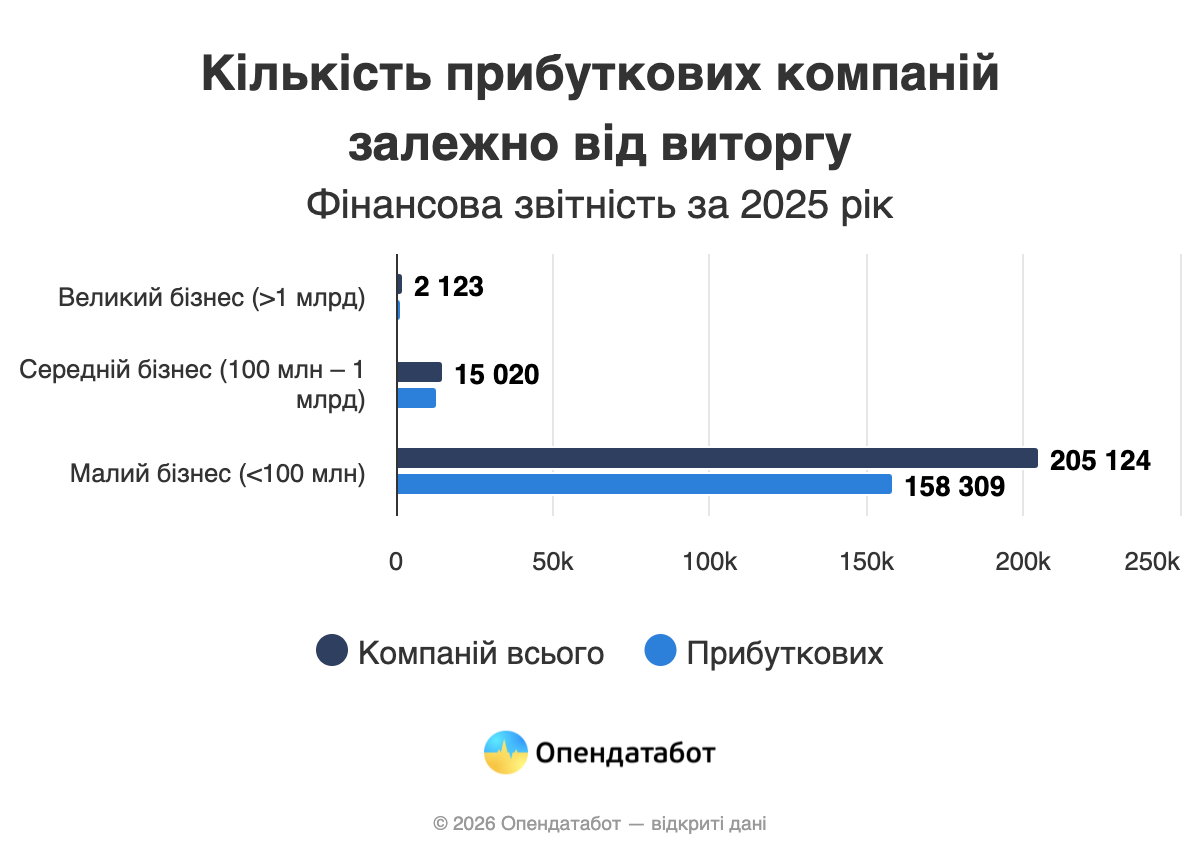

Almost 8 out of 10 Ukrainian companies ended 2025 with a profit, according to financial reporting data. Out of 222,000 businesses, every fifth company turned out to be loss-making. The largest share of profitable companies was among medium-sized businesses, while small businesses proved to be the most profitable: half of such companies earned more than UAH 5 in profit from every UAH 100 of revenue. Ukrhydroenergo, Ukrnafta and Energoatom received the largest net profit last year.

78% of Ukrainian companies included in the analysis of financial statements for 2025 ended the year with a profit: 173,510 enterprises. Another 21%, or 45,752 businesses, recorded losses, while 1% ended the year practically at break-even: 3,005 companies.

We are monitoring companies’ financial statements in Opendatabot.

How did we calculate this? In total, 429,800 companies submitted financial statements. For the analysis, 222,300 companies were selected that did not have non-profit status, had revenue above 0, provided data on net profit and had one of the following legal forms: limited liability company, private enterprise, farm, joint-stock company or subsidiary. Large businesses included companies with revenue from UAH 1 billion, the medium segment included companies with revenue from UAH 100 million to UAH 1 billion, and all companies with revenue below UAH 100 million were grouped as small businesses.

Medium-sized businesses turned out to be the most profitable: 89% of companies. These are enterprises with revenue from UAH 100 million to UAH 1 billion. Large businesses lagged only slightly: among companies with revenue above UAH 1 billion, 86% made a profit. In the small business segment, where annual revenue does not exceed UAH 100 million, the share of profitable enterprises was 77%.

At the same time, if sales profitability is assessed, small businesses have the best indicators: half of such companies have profitability above 5%. By contrast, half of large profitable enterprises operate with profitability below 2.6%. For half of medium-sized companies, this figure does not exceed 3.85%.

Top 10 most profitable companies in Ukraine

Ukrhydroenergo declared the largest net profit in 2025 – UAH 20.91 billion. The top three also included Ukrnafta with UAH 16.05 billion and Energoatom with UAH 11.85 billion in profit.

The top ten companies with the largest net profit also included Gas TSO of Ukraine, Centrenergo, Roshen, UMZ, SCM Finance, Ukrfinzhytlo and D. Trading.

Turkey has started opening some districts that were previously closed for foreigners applying for residence permits, which may support demand for real estate in popular resort locations, primarily in Alanya and other areas of Antalya province, local media report.

This concerns a review of restrictions that in recent years applied to districts with a high concentration of foreign residents. Such zones were closed for first-time residence permit applications, including through the purchase or rental of housing. It was possible to buy real estate there, but it was impossible to obtain a residence permit at an address in a closed district.

After long appeals from businesses, migration authorities lifted some of the strict restrictions in sought-after areas of Alanya. Among the locations that are again being discussed as available for full legalization of foreigners are Mahmutlar, Avsallar and other popular areas of the resort market.

The industry publication Türkiye Today also writes that in June 2026 Turkey effectively returned to broader availability of districts for residence permit applications, with the exception of certain restrictions, particularly in two districts of Istanbul – Fatih and Esenyurt. At the same time, the market is still waiting for additional official clarifications on legal details, including the link between property purchases, address registration and the right to resident status.

Previously, Turkey had a system of closed districts if the share of foreigners in the local population exceeded a set threshold. In 2022-2025, this became one of the factors cooling foreign demand for housing in resort cities, especially in Antalya, Alanya, Mersin and Istanbul.

For the real estate market, the opening of previously closed districts may become an important signal. Foreign buyers often view the purchase of housing in Turkey not only as an investment or resort asset, but also as a basis for long-term residence. Therefore, the ability to register an address and submit documents for a residence permit directly affects the liquidity of such properties.

This change may be especially sensitive for Alanya. In recent years, Mahmutlar, Kestel, Avsallar, Kargicak and other districts actively attracted buyers from Russia, Ukraine, Kazakhstan, Iran, Germany and Middle Eastern countries. After the introduction of restrictions, part of demand shifted to other locations or was postponed.

Restored access to residence permits may support both the primary new-build market and the secondary market, where many apartments were purchased by foreigners in 2020-2023. However, experts expect demand to be more cautious than during the peak relocation period after 2022: buyers have become more attentive to legal risks, housing maintenance costs, the lira exchange rate and the prospects for obtaining documents.

According to the Turkish Statistical Institute, in April 2026 foreigners purchased 1,516 residential properties in Turkey, 1.1% less than a year earlier. The share of foreigners in total sales was 1.2%. In January-April 2026, foreign buyers purchased 5,681 properties, 11.6% less than in the same period of 2025.

The main centers of sales to foreigners in April 2026 remained Antalya and Istanbul. According to specialized Turkish platforms based on TURKSTAT statistics, foreigners bought 453 properties in Antalya, 412 in Istanbul and 120 in Mersin. They were followed by Yalova – 68, Ankara – 53, Bursa – 49, Izmir – 41, Mugla – 27, Kocaeli – 24 and Sakarya – 21.

Among foreign buyers in April 2026, Russian citizens were the leaders, purchasing 263 real estate properties. Chinese citizens ranked second with 110 properties, followed by Iranians with 100. Ukrainians ranked fourth with 78 purchases. They were followed by citizens of Iraq – 65, Germany – 61, Kazakhstan – 54, Azerbaijan – 48, Saudi Arabia – 39 and the United Kingdom – 35.

Thus, Ukrainians remain one of the notable groups of foreign buyers of Turkish real estate, although in April 2026 they were no longer in the top three. For comparison, in January 2026 Ukrainians ranked third among foreigners, purchasing 77 properties and trailing only Russians and Iranians.

According to analysts of the Fixygen.ua project, the cryptocurrency market ended the first week of June lower: Bitcoin fell below $60,000 and updated its lows since autumn 2024, Ethereum declined to the $1,550-1,650 zone, while the largest altcoins remained under pressure due to weak demand for risk.

As of June 8, Bitcoin is trading at around $61,800, Ethereum at around $1,630, and Solana at around $64.7. Despite a local rebound at the beginning of the new week, the market remains in a weak position after one of the toughest weeks of 2026.

The main pressure factor was outflows from cryptocurrency investment products. According to CoinShares, in the week to June 1, digital assets recorded outflows of $1.67 billion, marking the third consecutive week of negative dynamics and the second-largest weekly outflow in 2026. Investors withdrew $1.438 billion from Bitcoin products – the largest weekly BTC outflow since the beginning of the year – and $257 million from Ethereum products.

Pressure continued in early June. According to Farside Investors, U.S. spot Bitcoin ETFs showed net outflows of $483.8 million on June 1, $519.1 million on June 2, and $396.6 million on June 3. Only on June 4 were the funds able to move slightly into positive territory – around $3.2 million.

The weakness of ETFs became a signal that institutional demand for crypto assets remains limited. After strong growth in previous years, investors are taking profits, reducing exposure to high-risk assets and reallocating capital to more understandable themes, primarily shares of companies related to artificial intelligence, data centers and semiconductors.

An additional negative factor was news of the sale of part of its bitcoins by Strategy, the company associated with Michael Saylor. Although the sale volume was small compared with the company’s overall portfolio, the very fact of the first BTC sale in several years was perceived by the market as a psychologically negative signal.

Against this background, Bitcoin lost more than 10% over the week and briefly fell below the important $60,000 level. For some traders, this confirmed that the market had entered a phase of deep correction after a period of high liquidity and strong institutional interest.

Ethereum also came under pressure. Weak flows into ETH ETFs and the overall decline in risk appetite did not allow the largest altcoin to stay above $1,800. During the week, ETH declined to the $1,550 zone, after which it partially recovered.

Altcoins as a whole looked weaker than Bitcoin. Solana, XRP, Cardano and other major tokens declined amid reduced liquidity, growing investor caution and declining interest in riskier market segments. In such periods, capital usually concentrates in BTC and stablecoins, while altcoins face stronger pressure.

The macroeconomic backdrop also did not support the crypto market. Investors continue to assess the outlook for U.S. interest rates, inflation dynamics and the resilience of the stock market. As long as expectations for rate cuts remain uncertain, it is difficult for cryptocurrencies to gain a sustained recovery impulse.

Regulation remains a separate factor. The market is waiting for progress on U.S. bills on the structure of the crypto market and stablecoins, but the lack of quick clarity is reducing interest among some institutional investors. Without regulatory progress, crypto assets remain more dependent on ETF flows and overall market liquidity.

Despite the weak week, there are still no signs of panic comparable to the crises of 2022. The market has become more institutional, while liquidity is partly supported by ETFs, stablecoins and large market makers. However, the current dynamics show that the launch of ETFs has not eliminated the cyclicality of the market and has not protected Bitcoin from sharp corrections.

Next week, the key factors for the crypto market will be flows into Bitcoin and Ethereum ETFs, the dynamics of the U.S. stock market, expectations for Fed rates, news on Strategy and regulatory signals from Washington. For Bitcoin, the nearest important zone remains the $60,000-62,000 range; losing it could increase pressure on the market, while a return above $65,000 could become the first sign of stabilization.

The cryptocurrency market remains one of the most volatile segments of global finance. Bitcoin and Ethereum retain the status of the largest digital assets, but their dynamics are increasingly dependent on institutional flows, ETFs, macroeconomic expectations and competition for capital with other investment themes, primarily the AI sector.