Vodafone Ukraine (VFU), Ukraine’s second-largest mobile operator, increased its net profit by 12% in January–March 2026 compared to the same period last year, reaching 778 million hryvnia.

According to the company’s press release on Wednesday, revenue grew by 11% to UAH 7.3 billion.

Key drivers remain the growth in data service consumption, the development of the fixed-line business, and increased revenue from equipment sales and other services, Vodafone Ukraine explained.

It is noted that OIBDA increased by 4% to UAH 3.49 billion, while the OIBDA margin decreased to 47.8% from 50.7% in the first quarter of 2025, due to rising electricity costs, network resilience measures, personnel expenses, and increased radio frequency spectrum fees.

The mobile operator noted that the profit growth was driven by improved debt portfolio management.

Average revenue per user (ARPU) in the first quarter of this year increased by 13% to UAH 145.2 per month, with a stable subscriber base. At the same time, there has been an increase in the number of contract subscriptions, VFU added.

According to the press release, investment volume for January–March 2026 amounted to UAH 1.55 billion, which is 2% less than in January–March 2025. Key investment areas include improving the energy resilience of infrastructure—specifically ensuring backup power, expanding the use of generators and batteries—as well as developing and modernizing the mobile network, particularly by expanding 4G coverage.

Investments were also made in the development of fixed-line internet access based on modern technologies (GPON) and in preparing the infrastructure for the rollout of new generations of communication, including 5G.

“The company continues to implement systematic network modernization projects and is introducing technological solutions aimed at improving service quality and adapting the infrastructure to new challenges,” the statement said.

As reported, Vodafone Ukraine increased its revenue by 14% in 2025 compared to the previous year—to 27.8 billion UAH—while its net profit grew by 18%—to 4.18 billion UAH.

You can read English just fine.

Understand emails.

Even watch YouTube without subtitles.

But then a Zoom call starts.

— “Hey everyone, thanks for joining…”

— “Can we quickly align on this?”

— “What are your thoughts?”

And suddenly your mind goes blank.

You start to:

● get nervous;

● be afraid to interrupt;

● get lost because of accents;

● freeze before answering;

● think not about the meaning of the conversation, but about your own mistakes.

It’s especially frustrating when you’re a skilled professional but suddenly feel insecure in English.

And this is much more common than it seems.

Many people think:

“If I know English, that means I’ll be able to speak normally during work calls.”

But Zoom English works differently.

Here, it’s not enough to simply “know the words.”

During live communication, the brain performs a bunch of tasks simultaneously:

● listens;

● translates;

● formulates a response;

● analyzes the reactions of the people you’re talking to;

● keeps track of the context;

● copes with stress.

And all of this happens in real time.

That’s exactly why someone can:

● write excellent English;

● read documentation just fine;

● have a good vocabulary —

but still get lost during calls.

Especially when there are:

● different accents;

● a fast pace;

● interruptions;

● technical delays;

● poor sound quality;

● multiple people speaking at once;

● small talk;

● professional terminology.

Your brain is literally working in overdrive.

That’s why fatigue after English-language calls is a very real thing.

This is one of the most common problems adults face.

A person thinks:

● “I know this…”

● “I learned this phrase…”

● “Why am I silent right now?”

The problem isn’t with knowledge.

The problem is with the speed of accessing it under stress.

During a Zoom call, there is no:

● 30 seconds to think;

● opportunity to translate calmly;

● “preparation” pause.

You have to react immediately.

And that is what scares people the most.

It’s important to realize this.

A language barrier doesn’t mean that a person:

● isn’t smart enough;

● is a poor professional;

● is “weak” in English.

Very often, the opposite is true:

the more responsible a person is, the more nervous they get.

Because they want to:

● sound professional;

● not lose their credibility;

● not look confused;

● not create an awkward pause.

This is especially true for:

● managers;

● IT specialists;

● marketers;

● HR;

● sales teams;

● professionals who work with international clients.

Many people are surprised by this idea.

But the problem for adults is rarely:

● the Present Perfect;

● conditional sentences;

● complex grammar.

Most often, the challenge is:

● reacting quickly;

● listening to different accents;

● not panicking;

● making small talk;

● speaking without long pauses.

And here’s the key point:

You need to practice speaking for calls separately.

Just like:

● presentations;

● negotiations;

● job interviews;

● public speaking.

Yes, you might.

And that’s okay.

In international teams, most people are NOT native speakers.

Everyone:

● has an accent;

● makes mistakes;

● sometimes asks for clarification;

● gets lost.

And this has long been a part of global communication.

This fear is very common.

Especially when:

● someone speaks quickly;

● there’s an unfamiliar accent;

● the microphone is bad;

● the topic is complex.

But the good news is that professionally asking for clarification is a completely normal practice.

In reality, most people think about the following during a call:

● deadlines;

● tasks;

● their own stress;

● a presentation;

● the client.

Not about your grammar or accent.

Moreover, confidence in speaking is often more important than “perfection.”

This is one of the main mistakes.

Before the call, you should:

● write down key points;

● prepare key phrases;

● think through your answers;

● review terminology related to the topic.

Even native speakers often take notes before important calls.

This really helps your brain when you’re stressed.

● Hey everyone, thanks for joining

● Nice to meet you all

● Hope you’re doing well

● Thanks for your time today

● That’s a good question

● Let me think for a second

● From my perspective…

● I’d say that…

● As far as I understand…

These phrases give your brain time to formulate a response.

● Could you repeat that, please?

● Sorry, the audio cut out

● Could you say that a bit slower?

● Just to make sure I understood correctly…

This sounds professional and completely normal.

It’s small talk that often causes the most discomfort.

Especially for people who know “business” English well.

Simple options:

● How’s your week going?

● Hope the weather is better there ????

● Have you been busy lately?

You don’t need to try to sound “really interesting.”

It’s enough to sound natural.

Here’s the paradox:

People with intermediate English sometimes sound more confident than those who know more.

Why?

Because:

● they don’t try to construct complex sentences;

● they speak more simply;

● they don’t overcomplicate things;

● they focus on the content.

For example:

❌ “Regarding the implementation process, we potentially might…”

✅ “I think we should start with…”

Short sentences often sound:

● clearer;

● more professional;

● more confident.

After English-language calls, many people feel:

● exhausted;

● a headache;

● overwhelmed;

● the desire to “stay silent until evening.”

And this isn’t “weakness.”

During a call, the brain is constantly:

● processing a foreign language;

● analyzing context;

● anticipating responses;

● controlling one’s own speech.

It’s especially difficult for introverts and people with high anxiety.

Nothing replaces live speaking.

That’s exactly why people who:

● just watch videos;

● read;

● do exercises —

often still fear Zoom calls.

The brain needs practice reacting in real time.

This is critically important.

Because international calls aren’t just “perfect British English.”

You might encounter:

● Indian accents;

● Polish;

● German;

● French;

● Ukrainian;

● American;

● mixed accents.

And you have to get used to each of these separately.

Not abstract topics from a textbook.

But:

● calls;

● meetings;

● presentations;

● negotiations;

● daily tasks;

● small talk;

● explaining tasks.

This is exactly where <a href=”https://www.english.kh.ua/ukr/corporate/”>our experience shows</a> that adults start making progress much faster when they practice not “English in general,” but specific work situations they actually face every day.

This is an important point.

Many people wait:

● “I’ll learn a few more words”;

● “I’ll brush up on my grammar”;

● “I’m not ready to speak yet.”

But speaking works the other way around.

At first:

● it’s awkward;

● it’s scary;

● it’s slow;

● there are mistakes.

And only then does confidence emerge.

There is no moment when a person suddenly starts speaking “without fear.”

Fear diminishes through repetition.

Just a few years ago, it was possible to avoid international communication.

Now, for many professions, that’s no longer an option.

Zoom English impacts:

● career growth;

● international projects;

● salary;

● confidence;

● the ability to work globally.

And the good news is that this isn’t a “talent.”

It’s a skill.

And skills can be trained.

Even if you’re afraid to speak on calls right now—that doesn’t mean it will always be that way.

The national postal operator Ukrposhta has launched a new queue-free parcel pickup service that involves installing special express pickup lockers inside post offices, according to a company statement released on Wednesday.

According to the press release, the first 120 express pickup kiosks have been installed in Kyiv and the Kyiv region. In total, during the first phase, the new system will be implemented in 400 branches, primarily in cities with populations over one million and regional centers.

Ukrposhta explained that some shipments are automatically routed by the company to be picked up via the new format; once the package arrives, the customer receives an SMS with an access code, opens the corresponding section, and picks up the shipment independently without needing to speak to an operator.

It is noted that these lockers are available directly at the branches and operate during their business hours.

“We have long been looking for a way to separate customer flows: those who come only for a package and those who use other services—from utility payments to international money transfers. Testing is still ongoing, but it is already clear: it is possible to pick up a package at Ukrposhta without waiting in line,” the press release quotes Ukrposhta CEO Ihor Smiliansky as saying.

The company emphasizes that the launch of the new format is part of the national postal operator’s service upgrade.

“Following the completion of 100% automation of sorting processes and the creation of an infrastructure with a potential capacity of up to 3 million shipments per day, the company is gradually transforming the customer experience: expanding the network of parcel lockers, partner pickup points, and new formats for receiving parcels at branches,” Ukrposhta added.

As reported, the state-owned “Ukrposhta” posted a total profit of UAH 106.3 million for January-April, with EBITDA of UAH 122.9 million. The company’s equity reached UAH 2.3 billion without additional budget funding.

In January-March 2026, the company reported a net loss of UAH 204.8 million, which is UAH 1.1 million, or 0.5%, more than in the same period of 2025, while its revenue grew by 1.1% to UAH 13.11842 billion.

The unaudited EBITDA of six solar power plants (SPPs) with a total installed capacity of 105 MW in the Lviv region, which Ukraine’s largest mobile operator Kyivstar acquired for 3.6 billion UAH (or $80.8 million), amounted to UAH 596 million in 2025.

According to Kyivstar’s presentation on the acquisition, the revenue of these six SPPs, commissioned between 2017 and 2025, totaled UAH 682 million last year.

The operator noted that this investment, calculated at $0.77 million per 1 MW, aligns with one of its four priorities—capital investment in real assets that mitigate inflationary and/or currency risk.

“Renewable energy is one of the key areas of Kyivstar’s investment portfolio, as it opens up opportunities for the further use of ‘green’ electricity to cover part of the company’s energy needs,” Kyivstar CEO and President Oleksandr Komarov is quoted as saying in the press release.

The three other priorities listed are investments in infrastructure reconstruction and preventive network protection, the development of a digital ecosystem through adjacent acquisitions, and increasing the market share of fixed broadband through targeted acquisitions.

Taking into account the initial purchase last December of the 13-MW “Sunwin 11” solar power plant for $3 million in the Zhytomyr region, Kyivstar’s total “green” generation capacity has grown to 118 MW, which enables the production of electricity equivalent to approximately 30% of the company’s current annual consumption, according to the press release.

“Electricity from the acquired solar power plant group will be fed into Ukraine’s unified power grid in accordance with current market and regulatory rules, which will allow Kyivstar to partially hedge risks associated with fluctuations in electricity prices,” Kyivstar explained.

The mobile operator noted that these “green” projects also enable it to build a long-term energy consumption model, strengthen the country’s energy sector, and align with sustainable development goals.

Kyivstar’s stock price rose by 2.18% on May 26, the day the purchase of six solar power plants was announced, reaching $14.51 per share.

As reported, in March of this year, Kyivstar received approval from the Antimonopoly Committee of Ukraine (AMCU) to purchase six solar power plants in the Lviv region: Energo-Postach-Plus LLC, Lightful, Sunlight Generation, Ternovytsia Solar, Energy Space, and Ternovytsia Solar Plus.

In the first quarter of 2026, Kyivstar increased its EBITDA by 28.5% to UAH 7.5 billion, while revenue grew by 31.3% to UAH 13.9 billion.

In 2025, the Kyivstar Group increased its EBITDA by 30% to UAH 27 billion, with revenue growing by 30.3% to UAH 48.2 billion. In particular, in the fourth quarter of last year, EBITDA increased by 23.1% to UAH 7.2 billion, with revenue growing by 30.1% to UAH 13.5 billion.

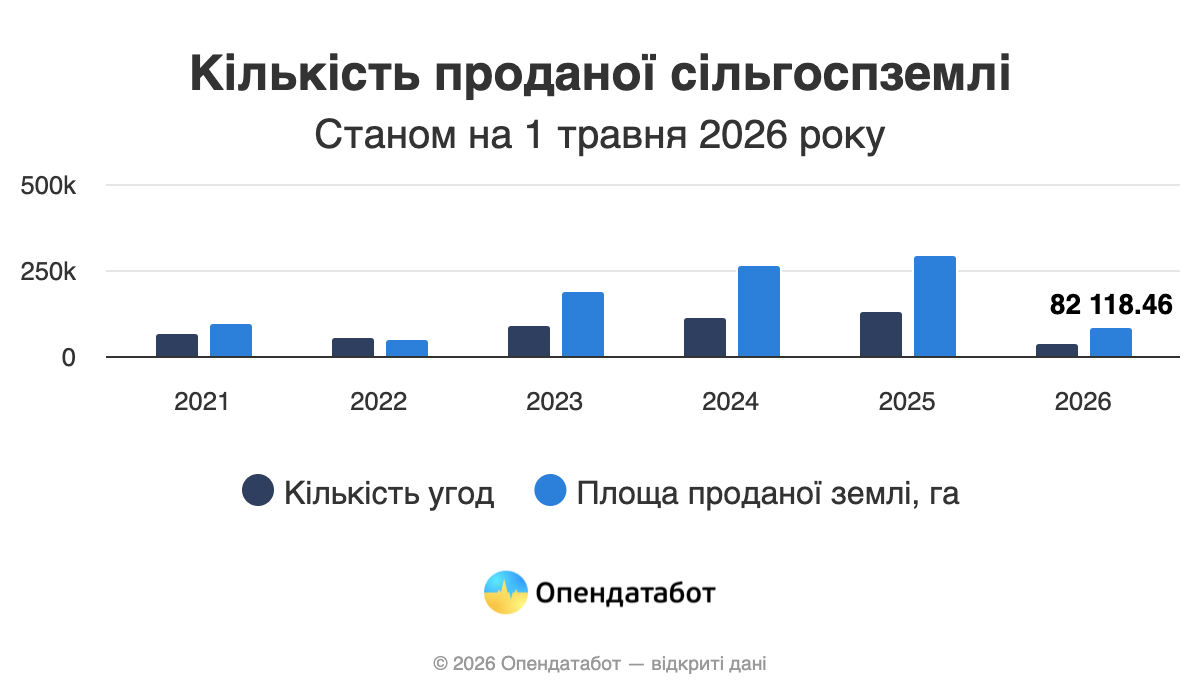

Over half a million transactions and nearly 50 billion UAH—this is the state of the agricultural land market in Ukraine more than four years after the moratorium was lifted, according to the State Service of Ukraine for Geodesy, Cartography, and Cadastre. The average price per hectare of land in Ukraine currently stands at 75,100 UAH. The most expensive land is currently in Ivano-Frankivsk and Kyiv regions, while the most active land purchases this year are taking place in Vinnytsia and Chernihiv regions.

501,619 agricultural land purchase and sale transactions totaling 49.7 billion UAH have been concluded in Ukraine over the past four years since the opening of the land market. The total area of the plots covered by these transactions is 977,200 hectares.

We are tracking the trends on the Land Market in Ukraine page.

Ukrainians concluded a record 131,300 transactions last year. This is 13% more than in 2024. At the same time, the total value of transactions jumped by 43%: from 12.5 billion UAH to 18 billion UAH. While in 2024 a hectare of land cost an average of 47,300 UAH, in 2025 it was already 61,800 UAH. Thus, land prices rose by nearly a third over the course of the year.

The land market continued to rise in price in 2026 as well. In just the first four months, Ukrainians concluded 39,797 transactions totaling 6.17 billion UAH. Although the number of transactions decreased by 5% compared to the same period last year, the cost of land continued to rise rapidly, reaching 75,100 UAH/ha. This is 26% more than a year earlier.

It is worth noting that while prices rose, the area of land sold decreased. While 92,900 hectares were sold in January–April 2025, this year the figure was 82,100 hectares.

January has so far been the most expensive month of 2026—at that time, the average price per hectare reached 95,700 UAH. Buyers were most active in March, when 12,276 deals were concluded.

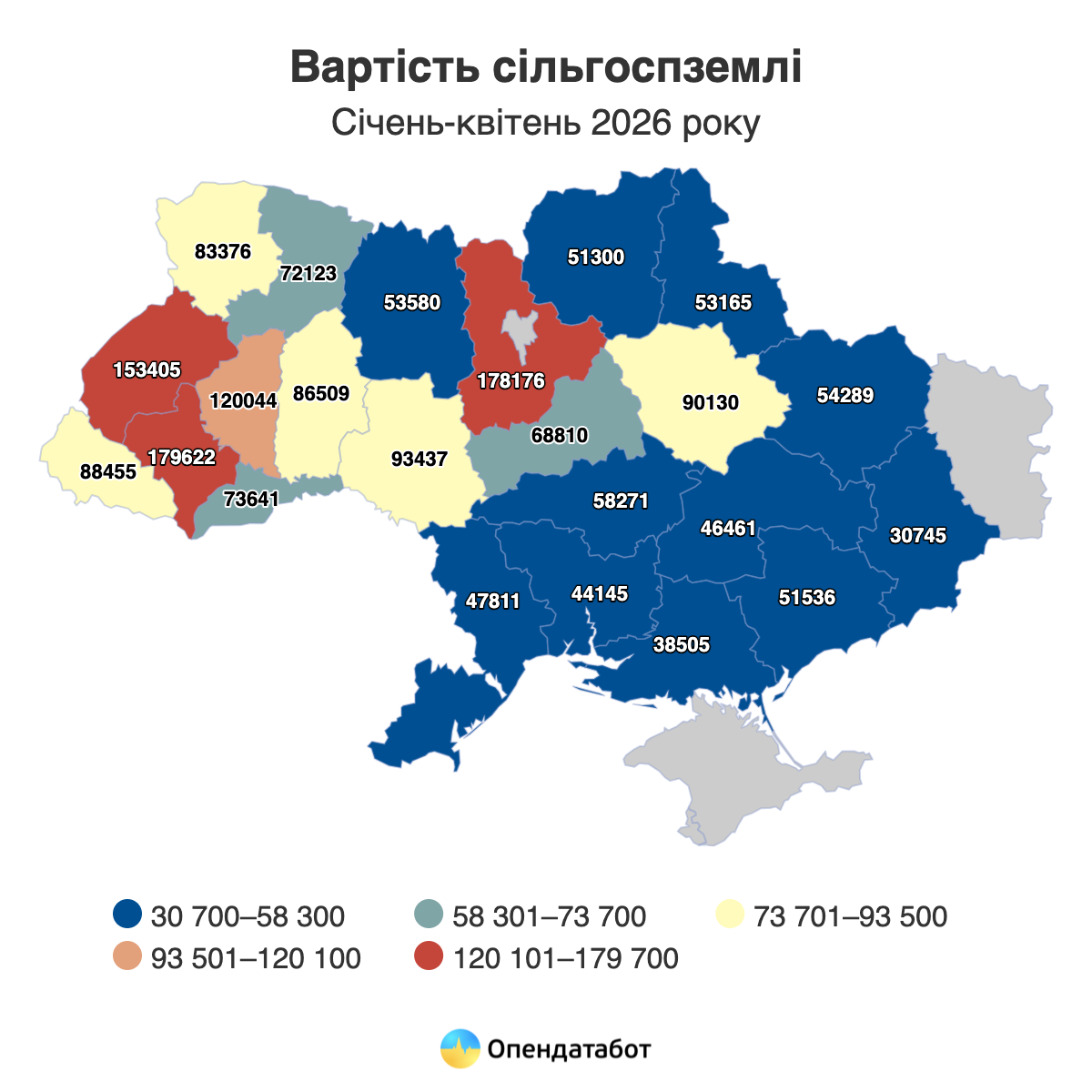

Traditionally, prices vary significantly by region. The most expensive land is currently in Ivano-Frankivsk Oblast, where a hectare costs an average of 179,600 UAH. The price is nearly the same in Kyiv Oblast—178,200 UAH/ha. The top five most expensive regions also include Lviv Oblast (153,400 UAH/ha), Ternopil Oblast (120,000 UAH/ha), and Vinnytsia Oblast (93,400 UAH/ha).

In contrast, the lowest prices are found in the frontline and southern regions. In Donetsk Oblast, a hectare of land costs 30,700 UAH, in Kherson Oblast—38,500 UAH/ha, and in Mykolaiv Oblast—44,100 UAH/ha. The regions with the lowest land prices also include Dnipropetrovsk Oblast (46,500 UAH/ha) and Odesa Oblast (47,800 UAH/ha).

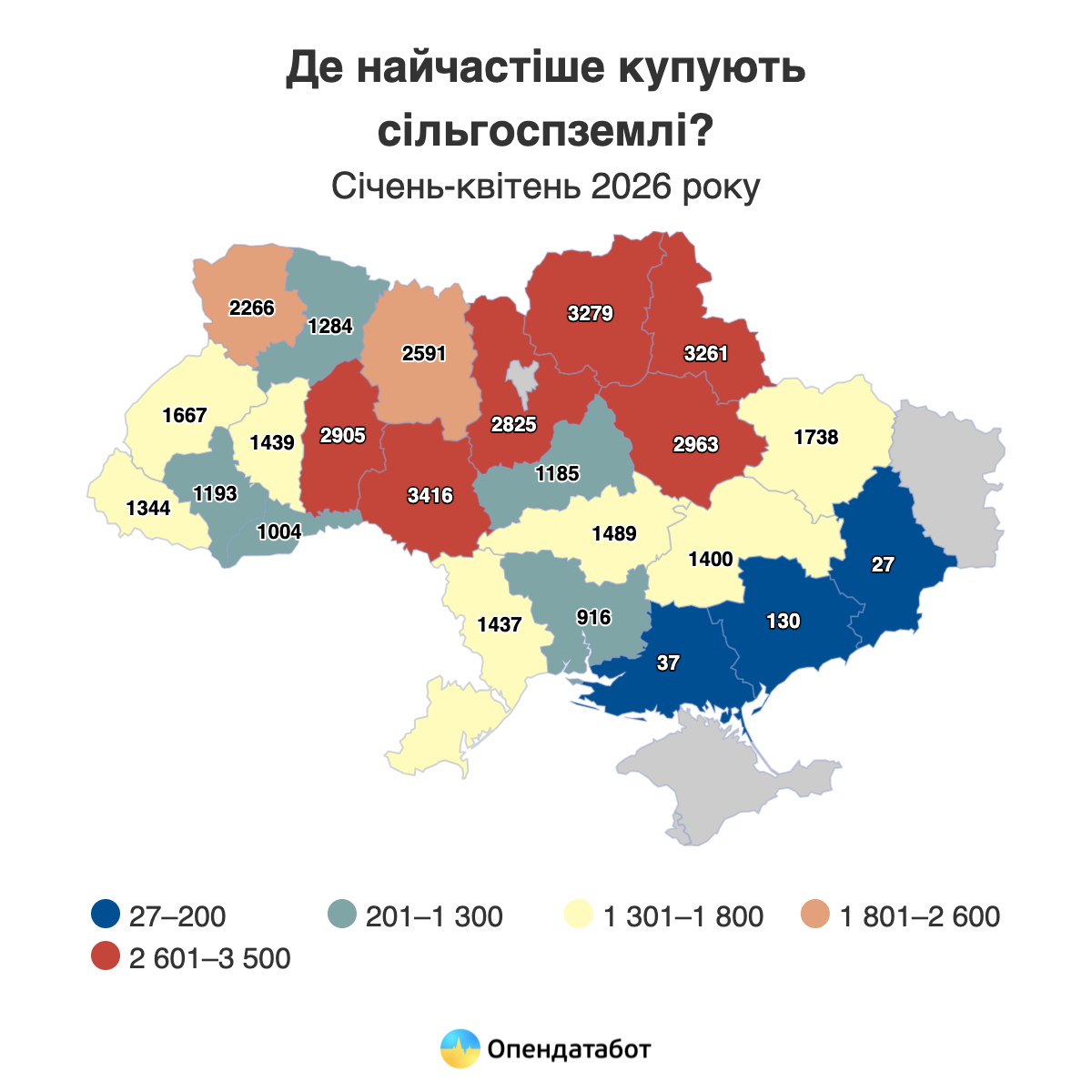

Land is being sold most actively in the central and northern regions of the country. Thus, the highest number of transactions since the beginning of the year was recorded in Vinnytsia Oblast—3,416. Next are Chernihiv (3,279), Sumy (3,261), Poltava (2,963), and Khmelnytskyi (2,905) regions.

https://opendatabot.ua/analytics/landmarket-2026

The spring-summer ban on fishing in rivers and inland waters, which had been in effect since April 1, has ended, the press service of the State Agency for Fisheries (Derzhrybagentstvo) reported on Wednesday.

It is noted that fishing is now permitted in rivers and inland waters, but only with handlines or spinning rods using natural or artificial bait, with a total of no more than seven hooks per angler.

The State Fisheries Agency reminded that the daily catch limit is 3 kg of fish plus one specimen exceeding the minimum size allowed for catch. For example, in inland waters, catfish must be at least 80 cm long, pike—50 cm, and walleye—42 cm; for chub and sabre-tooth, 24 cm; for blue bream, 22 cm; and for tench and roach, 20 cm.

At the same time, weight and quantity restrictions do not apply at all to the catch of species such as sand smelt, silver bream, dwarf American catfish, roundhead, sunfish, tulka, and Amur gudgeon.

It is emphasized that fishing for fish listed in the Red Book of Ukraine remains strictly prohibited. These include: European grayling; Danube and Black Sea salmon; Black Sea vimba; Dnieper roach; ide; podust; golden crucian carp; sterlet; beluga; sturgeon; sevruga; and several other species.

In reservoirs, particularly those of the Dnipro Cascade, as well as in ponds and estuaries, the spawning ban remains in effect. In these areas, fishing is permitted exclusively from the shore and outside of spawning grounds. At the same time, only spinning rods with a single artificial lure or hook-and-line tackle with no more than two hooks per person may be used, the agency added.