Ukrainian companies increasingly need to move from one-time checks of counterparties to regular monitoring of their condition. In a period of high economic, military and logistical risks, a partner’s financial position can change rapidly, and a delay in updating information may lead to losses.

Dun & Bradstreet tools can be used not only for the initial assessment of a counterparty, but also for the subsequent tracking of changes in its business profile, payment discipline, corporate connections, risks and reputational factors. Such an approach is especially important for companies that work with deferred payments, large batches of goods or long-term contracts.

For Ukrainian businesses, regular monitoring can become part of an internal risk management system. It helps companies respond more quickly to a partner’s problems, revise contract terms, limit credit lines or require additional guarantees.

“In a crisis environment, a counterparty that was reliable yesterday does not necessarily remain so tomorrow. That is why business verification, primarily the verification of foreign businesses, should not be a one-time action, but a continuous process,” said Maksym Urakin, Director of Development and Marketing at Interfax-Ukraine, Head of the D&B-Interfax-Ukraine Business Unit, and PhD in Economics.

He added that the culture of counterparty monitoring should become as routine for Ukrainian companies as accounting or the legal review of a contract.

Dun & Bradstreet is an international company in the field of business data and analytics, founded in 1841. The company provides tools for business identification, counterparty verification, credit and commercial risk assessment, compliance and supply chain analysis. One of D&B’s key tools is the D-U-N-S Number, a unique nine-digit company identifier used in international business practice. In Ukraine, D&B is represented by the Interfax-Ukraine agency. The partnership is aimed at expanding Ukrainian companies’ access to international business data, supporting exports, attracting financing and integrating into global supply chains. Interfax-Ukraine is an independent Ukrainian news agency that has been operating since 1992.

According to Experts.news, Ukraine’s construction industry has shown mixed trends based on preliminary results for the first half of 2026: following growth in 2023–2025, the sector has faced a slowdown in the volume of work, rising construction costs, a labor shortage, and a shift in demand toward housing and infrastructure reconstruction.

The State Statistics Service has not yet released final data for January–June, so a current assessment can be made based on statistics for the first four months, data on housing completions in the first quarter, the “eOselya” and “eVidnovlennia” programs, as well as construction companies’ expectations for the second quarter.

According to the State Statistics Service, the volume of construction work completed in Ukraine in January–April 2026 decreased by 2% compared to the same period in 2025 and amounted to 59.3 billion UAH. At the same time, in April compared to April 2025, construction had already shown a 2.8% increase; specifically, residential construction rose by 5.8%, civil engineering structures by 9.7%, while non-residential construction declined by 7.4%. New construction accounted for 47.8% of the total in April, repairs for 29%, and reconstruction and other work for 23.2%.

By comparison, in 2025, the volume of construction work completed in Ukraine rose by 11.3% to 258.2 billion UAH, but the growth rate was already slowing down at that time, following 17.8% growth in 2024 and 31.8% in 2023. In 2025, residential construction grew by 13.5%, nonresidential construction by 25.4%, and civil engineering by only 3.1%.

“In the first half of 2026, the construction sector effectively transitioned from a phase of rapid post-shock recovery to a phase of selective growth. Housing, renovations, engineering infrastructure, and reconstruction-related projects remain the most resilient. At the same time, commercial non-residential construction remains weaker due to war risks, more expensive financing, and uncertainty for investors,” noted Maksym Urakin, founder of the Experts Club analytical center and candidate of economic sciences.

The residential segment appears more stable than the overall industry trend. In the first quarter of 2026, housing completions in Ukraine decreased by only 0.1% year-over-year, to 2.289 million square meters. During this period, 29,600 apartments were completed, which is 4.3% more than in the first quarter of 2025. The largest volumes of housing completions were recorded in the Lviv, Odesa, Ivano-Frankivsk, Zakarpattia, and Ternopil regions, while in Kyiv, 289,000 square meters of housing—or 4,900 apartments—were completed.

Government programs remain one of the key sources of demand for housing. According to the Ministry of Economy, as of June 22, 2026, 4,104 Ukrainian families had taken advantage of the “eOselya” program since the beginning of the year, receiving preferential mortgage loans totaling nearly 7.7 billion UAH. In just one week in June, 157 loans totaling 313 million UAH were issued, with the majority of new loans going toward first-time home purchases.

The “eVidnovlennia” program plays an even more important role for the construction market. As of June 2026, 206,447 Ukrainian families had received assistance for repairing or purchasing new housing, totaling 103.9 billion UAH. More than 138,000 families received payments to repair damaged homes, nearly 65,000 families received housing certificates for destroyed property, and a separate program for rebuilding on private land is already being funded through tranches.

At the same time, the industry is facing significant price pressure. According to the summary table of price indices for construction and installation work, in April 2026, the construction price index stood at 103.1% compared to March, following 109.4% in March, 101.8% in February, and 101.1% in January. The cumulative figure for the first four months of 2026 was 116.1%, indicating a significant increase in the cost of labor and materials.

Business expectations among construction companies remain cautious. According to a State Statistics Service survey for the second quarter of 2026, the business confidence indicator in construction improved by 1.9 percentage points compared to the first quarter but remained deeply negative at minus 25.7%. The current order volume was estimated at minus 41.5%, and expectations regarding the number of employees stood at minus 9.9%. Companies cited labor shortages, financial constraints, and other factors as the main limiting factors, while their order backlog was estimated to cover an average of six months of work.

At the macro level, the country’s recovery remains the industry’s main long-term driver. According to estimates by the World Bank, the Ukrainian government, the European Commission, and the UN, Ukraine’s needs for recovery and reconstruction over the next ten years are already estimated at nearly $588 billion. Direct losses reached $195 billion, with the housing, transportation, and energy sectors hardest hit. Damages to the housing sector alone are estimated at approximately $61 billion, and about 14% of the housing stock has been damaged or destroyed.

According to Experts Club’s assessment, in the second half of 2026, Ukraine’s construction industry will remain dependent on three key factors: the security situation, access to financing, and the stability of government recovery programs. Residential projects in hinterland regions, the reconstruction of damaged housing, engineering infrastructure, the energy resilience of communities, social housing, and critical infrastructure facilities will have the greatest potential.

“The Ukrainian construction sector cannot be assessed solely based on the current index of completed work. It is no longer just an economic sector, but one of the key tools for survival, the return of people, the recovery of communities, and the country’s future investment attractiveness. But the transition from repairs to large-scale modernization requires long-term financing, insurance against war risks, transparent project pipelines, and skilled personnel,” emphasized Maksym Urakin.

Thus, the first half of 2026 for Ukraine’s construction industry can be preliminarily assessed as a period of stabilization following the rapid growth of previous years. The market is not showing a uniform upturn, but it has significant structural demand related to housing, reconstruction, infrastructure, and future post-war reconstruction. For businesses, this means a shift toward more selective competition—companies with access to financing, qualified personnel, a transparent cost estimation framework, and the ability to work with government and international reconstruction programs will come out on top.

CONSTRUCTION, EXPERTS CLUB, HOUSING, INFRASTRUCTURE, RECONSTRUCTION, URAKIN

The article presents key macroeconomic indicators of Ukraine and the global economy as of the end of March 2026. The analysis was prepared on the basis of current data from the State Statistics Service of Ukraine (SSSU), the National Bank of Ukraine (NBU), the International Monetary Fund (IMF), the World Bank, as well as leading national statistical agencies (Eurostat, BEA, NBS, ONS, TurkStat, IBGE). Maksym Urakin, PhD in Economics and founder of the Experts Club information and analytical center, presented an overview of current macroeconomic trends that determined the situation in Ukraine and the world at the beginning of 2026.

Macroeconomic indicators of Ukraine

As of the end of March 2026, the Ukrainian economy remained in a mode of managed macrofinancial stabilization, but the first quarter showed a noticeable deterioration in the balance of risks compared with the beginning of the year. After a relatively favorable January, when inflation was declining, reserves were at a historically high level, and the NBU began cautious easing of interest rate policy, the situation became more complicated in February-March. Inflation accelerated again, international reserves declined for the second month in a row, the foreign exchange market required significant interventions by the regulator, and the first quarterly GDP estimate showed a decline.

According to the preliminary estimate of the State Statistics Service, Ukraine’s real GDP in Q1 2026 decreased by 0.6% compared with Q1 2025, and by 0.7% compared with the previous quarter, taking into account the seasonal factor. Nominal GDP amounted to UAH 2,047.2 billion. This became an important signal that economic recovery remains unstable and highly sensitive to energy, military and foreign trade shocks.

In its April Inflation Report, the National Bank worsened its forecast for Ukraine’s real GDP growth in 2026 to 1.3%, taking into account further destruction of infrastructure, larger electricity deficits and the effects of a significant increase in energy prices. This means that even if international support is maintained and the situation on the foreign exchange market remains controlled, the economy is entering 2026 on a lower growth trajectory than previously expected.

“The first quarter of 2026 showed that the Ukrainian economy has still not moved into a classic recovery phase. We have a stabilization model that works thanks to international financial support, budget expenditures, business adaptation and NBU policy. But the decline in GDP in the first quarter indicates that the margin of safety remains limited. Energy destruction, labor shortages, weak exports and military risks are quickly affecting the real sector. Therefore, the main task for 2026 is to gradually restore the productive base of the economy,” Urakin noted.

Inflation dynamics in March also became less favorable. According to the State Statistics Service, as commented on by the NBU, consumer inflation accelerated to 7.9% year-on-year in March 2026. Month-on-month, prices rose by 1.7%. After the January slowdown to 7.4% and the February acceleration to 7.6%, the March figure confirmed that the disinflationary trend had become less stable.

The NBU explained the March acceleration primarily by the increase in prices for raw food products, fuel and certain services. Additional pressure was created by energy risks, rising business costs, the impact of external energy prices and increasing geopolitical tension. At the same time, core inflation remained closer to the forecast trajectory, which allowed the regulator not to move to a sharp tightening of policy, but at the same time limited the room for a further rapid reduction in the rate.

At the end of March, the NBU key policy rate remained at 15.0%. On March 20, the Board of the National Bank decided to keep it unchanged after the January reduction from 15.5% to 15.0%. The regulator explained this by the need to maintain the attractiveness of hryvnia assets, preserve the stability of the foreign exchange market and control inflation expectations.

“March effectively paused the discussion about rapid monetary policy easing. Inflation accelerated, the foreign exchange market remained tense, and external risks increased. Under such conditions, keeping the rate at 15% was a logical decision. Ukraine cannot afford to stimulate the economy at the cost of losing confidence in the hryvnia. In a wartime economy, the stability of expectations is often more important than a short-term reduction in the cost of credit,” Urakin emphasized.

The foreign exchange sector remained controlled but required significant support from the NBU. As of April 1, 2026, Ukraine’s international reserves amounted to almost $52.0 billion. In March, they decreased by 5.0%. This dynamic was caused by the National Bank’s foreign exchange interventions and the country’s debt payments in foreign currency, which were only partially compensated by inflows from international partners and the placement of foreign currency domestic government bonds.

Despite the decline, reserves remained high by historical standards and continued to serve as the main financial safety cushion. At the same time, the very need for large interventions indicated that the private foreign exchange market continued to have a structural currency deficit. Ukraine imports significantly more than it exports, and therefore exchange rate stability is largely supported by external financing and the NBU’s reserves.

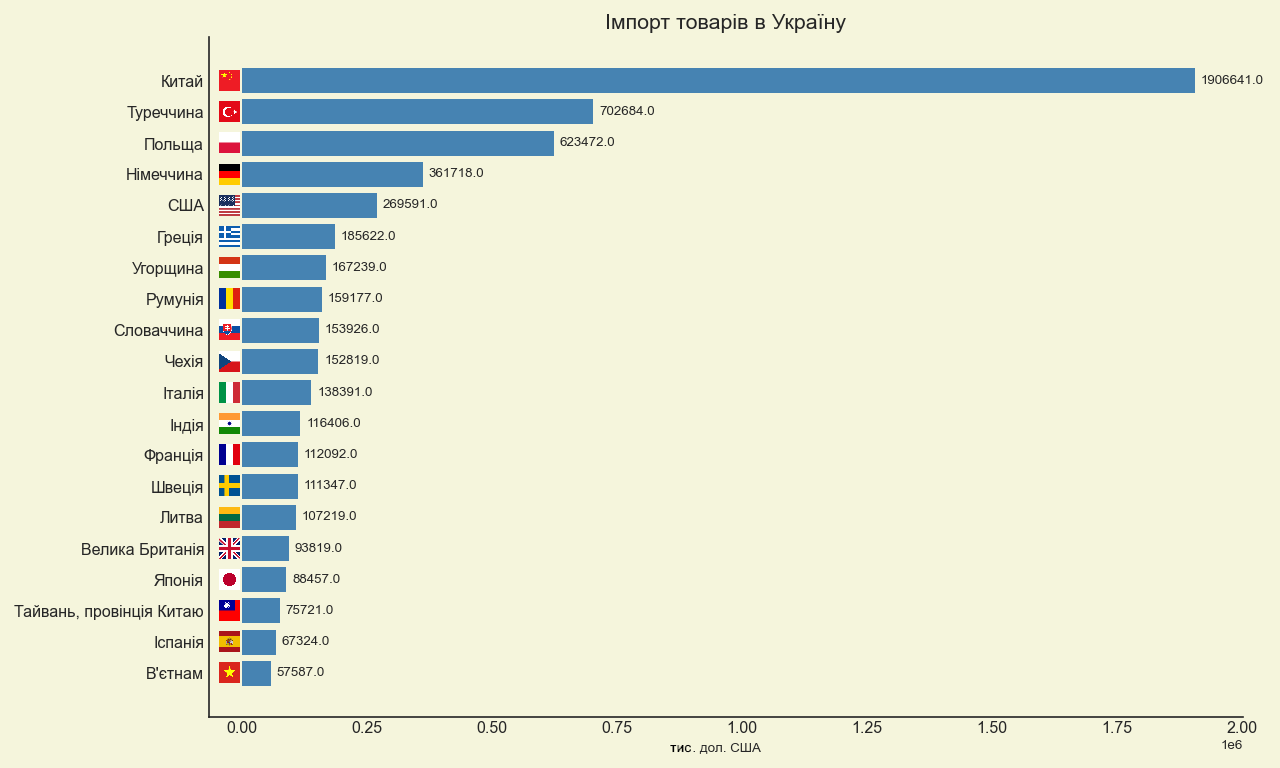

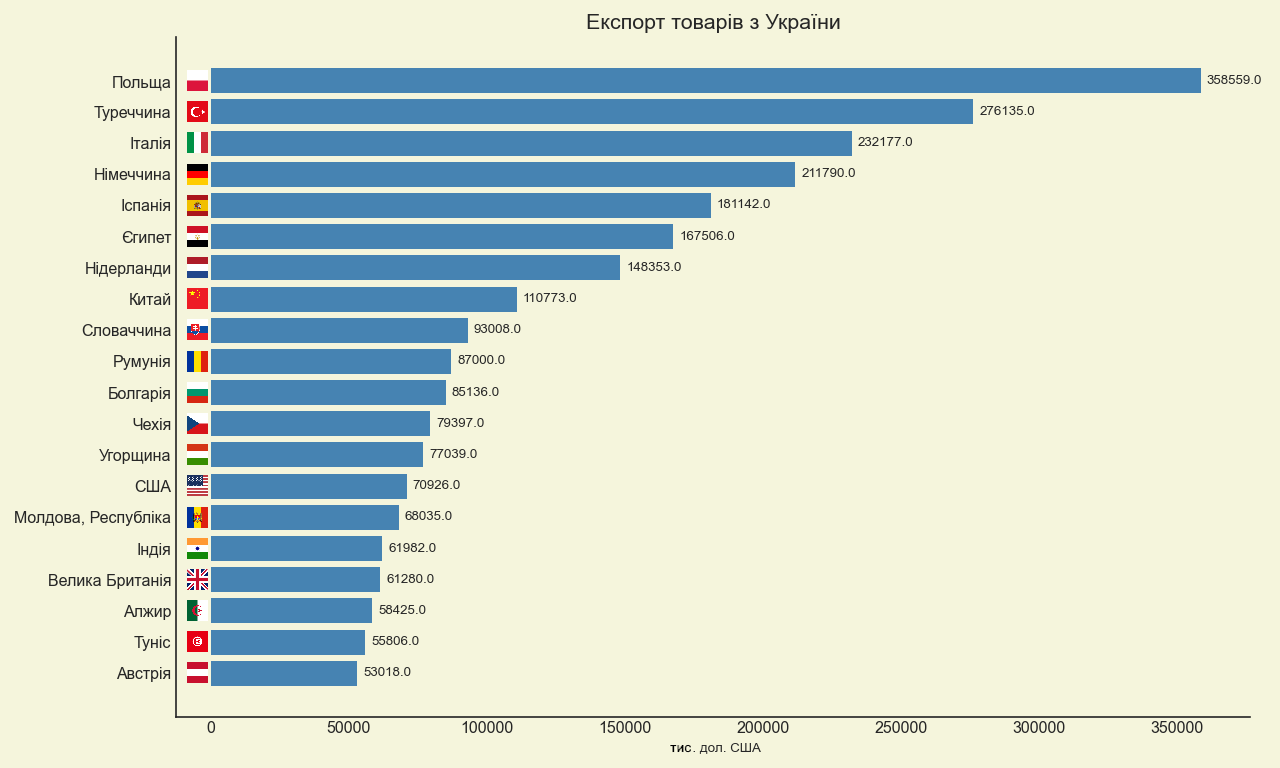

Foreign trade in the first quarter confirmed this problem. According to the State Customs Service, Ukraine’s trade turnover in January-March 2026 amounted to $33.5 billion. Imports reached $23.4 billion, while exports amounted to $10.1 billion. Thus, the goods deficit over three months amounted to about $13.3 billion, and imports were more than twice as high as exports.

In the import structure, machinery, equipment, transport, fuel and energy goods, and chemical industry products played a key role. China, Poland and Turkey remained the largest import trading partners. The export base remained significantly narrower: the main positions were food products, agricultural products, metals and certain machinery products. The main export destinations remained EU countries and Turkey.

“The trade deficit of the first quarter is one of the most important indicators of the vulnerability of the Ukrainian economy. Reserves and external assistance make it possible to pass through this period without a currency crisis, but they do not replace the country’s own export capacity. When imports are more than twice as high as exports, it means that the country is financing a significant part of its needs through external resources. In wartime conditions this is inevitable, but strategically such a model cannot be permanent. Ukraine must increase exports of products with higher added value, develop processing, logistics, energy autonomy and the defense-industrial complex,” Urakin stressed.

The budget situation following the results of the first quarter also remained tense. According to the Ministry of Finance, UAH 734.6 billion was received by the general fund of the state budget in January-March 2026. At the same time, cash expenditures of the general fund for this period amounted to UAH 916.4 billion, which is 7.1% more than in the corresponding period of the previous year. In March, expenditures amounted to UAH 369.1 billion.

Expenditures on security and defense in January-March amounted to UAH 570.9 billion, or 62.3% of all expenditures of the general fund. This confirms that the state budget in 2026 remains primarily a war budget. The largest areas of expenditure included remuneration in the budget sector with accruals, social security, subsidies and transfers to enterprises, payment for goods and services, servicing of public debt and transfers to local budgets.

“The budget of the first quarter of 2026 shows that the state maintains financial manageability, but the price of this manageability is very high. More than 60% of general fund expenditures are directed to security and defense, and this is absolutely understandable in wartime conditions. But such a structure means that the room for classic investment in development is limited. Therefore, international support, the domestic government bond market and the government’s ability to expand its own tax base through the restoration of economic activity remain critically important,” Urakin noted.

Global economy

As of the end of March 2026, the global economy remained resilient, but less predictable than at the beginning of the year. While in January the IMF’s baseline scenario projected global economic growth of 3.3% in 2026, in the April World Economic Outlook the Fund revised its estimates amid new geopolitical tensions in the Middle East. Under the baseline assumption of a limited conflict, the IMF forecast global growth of 3.1% in 2026 and 3.2% in 2027.

The IMF noted that the global economy had once again faced a shock related to war, rising commodity prices, stronger inflation expectations and tighter financial conditions. This meant that the global environment for Ukraine became less favorable: energy prices, risks to trade and the cost of capital again began to play a greater role.

The United States remained one of the main centers of global resilience. In the first quarter of 2026, U.S. real GDP grew by 2.1% year-on-year, according to the BEA estimate. Growth was supported by investment, exports, government spending and consumer spending. At the same time, inflation in the United States accelerated noticeably in March: the consumer price index rose by 3.3% year-on-year after 2.4% in February, while core CPI stood at 2.6%.

The Federal Reserve in March kept the target range for the federal funds rate at 3.5–3.75%. This meant that U.S. monetary policy remained restrictive, while expectations of a rapid rate cut were postponed. For countries with elevated risk, including Ukraine, this meant the preservation of a relatively high cost of global capital.

The eurozone was in a more difficult position. Its economic growth remained weak, while inflation again rose above the ECB’s target. According to Eurostat’s preliminary estimate, annual inflation in the eurozone in March 2026 stood at 2.5%, while the final estimate later showed 2.6%. In February, the figure was 1.9%, meaning that March brought a noticeable acceleration of price pressure. The main factor was energy, while core inflation remained more moderate.

The European Central Bank in March kept key rates unchanged: the deposit rate at 2.0%, the main refinancing operations rate at 2.15%, and the marginal lending facility rate at 2.40%. For Ukraine, the eurozone remains the most important external economic environment due to trade, financial assistance, EU integration, migration flows and logistics corridors. However, the weak growth rate in Europe limits the potential for a rapid increase in Ukrainian exports.

The United Kingdom also entered 2026 with a combination of moderate growth and an elevated inflation background. In March, the British CPI rose to 3.3% year-on-year after 3.0% in February. The Bank of England kept the Bank Rate at 3.75%, reflecting the regulator’s caution in the face of the risk of a new inflation acceleration. For the European region as a whole, this meant that the cycle of rapid monetary easing had not begun.

“The global economy did not enter a recession in the first quarter of 2026, but it became noticeably more nervous. The United States maintains stable growth, but is facing a new inflation acceleration. The eurozone has a weaker economic impulse and again sees inflation above the target. The United Kingdom also remains in a mode of cautious monetary policy. For Ukraine, this means that the external world does not create a catastrophic background, but also does not provide an easy impulse for recovery. Under such conditions, it is impossible to rely only on external demand,” Urakin noted.

The Chinese economy maintained relatively strong dynamics in the first quarter of 2026. According to the National Bureau of Statistics of China, China’s GDP grew by 5.0% year-on-year in Q1, and by 1.3% quarter-on-quarter. Nominal GDP amounted to about 33.4 trillion yuan. At the same time, inflation remained moderate: CPI rose by 1.0% year-on-year in March, and averaged 0.9% in January-March.

China continued to demonstrate a strong manufacturing base and export potential, but structural problems — weaker domestic demand, the real estate market, debt burden and dependence on external markets — remained important constraints. For Ukraine, China remained a key source of imports, primarily machinery, equipment, electronics and industrial goods.

India retained its status as one of the main drivers of global growth. According to the government’s first advance estimate, India’s real GDP in the 2025/26 fiscal year was expected to grow by 7.4%, while nominal GDP was expected to grow by 8.0%. The main driver remained the services sector, as well as domestic demand and public investment. The Indian economy remained one of the most convincing examples of combining high growth with relatively controlled inflation.

Turkey remained an example of an economy with relatively high business activity, but a very difficult inflationary legacy. According to official TurkStat data, in March 2026 consumer prices rose by 1.94% month-on-month and by 30.87% year-on-year. This was lower than in February, when annual inflation was 31.53%, but still remained an extremely high level. At the same time, the Turkish economy grew by 3.6% in 2025, which indicated the preservation of domestic demand despite inflationary risks.

Brazil looked more balanced among large emerging economies. According to IBGE, Brazil’s GDP in 2025 grew by 2.3%, to 12.7 trillion reais at current prices. Growth was observed in the agricultural sector, industry and the services sector. According to the preliminary IPCA-15 indicator, inflation in March 2026 amounted to 0.44% for the month and 3.90% over the last 12 months. This confirmed that Brazil maintained a relatively controlled inflation background, although its economy also felt the impact of high rates and external uncertainty.

“China, India, Turkey and Brazil show different development models of large emerging economies. China maintains scale and manufacturing strength, but has structural imbalances. India demonstrates the highest dynamics among major economies and relies on domestic demand and the services sector. Turkey is growing, but pays for it with high inflation. Brazil is moving more slowly, but more balanced. For Ukraine, it is important to look at these examples practically: in global competition, those countries win that can simultaneously maintain macro-stability, production, exports and domestic investment demand,” Urakin believes.

Conclusions

As of the end of March 2026, Ukraine maintained macrofinancial manageability, but the first quarter demonstrated the fragility of economic stabilization. Real GDP in Q1 decreased by 0.6% year-on-year, inflation accelerated to 7.9% in March, the key policy rate remained at 15.0%, international reserves declined to about $52.0 billion, and the goods deficit in January-March exceeded $13 billion. The budget remained functional, but its structure was fully subordinated to wartime needs: more than 60% of general fund expenditures were directed to security and defense.

The main risks for Ukraine remained wartime losses, destruction of energy infrastructure, weak exports, labor shortages, high budget dependence on external financing and the structural foreign exchange deficit of the private sector. Positive factors included a significant level of international reserves, the NBU’s controlled policy, continued international support, business adaptability and the state’s ability to fulfill key budget obligations.

The global economy in the first quarter of 2026 remained relatively resilient, but less stable than at the beginning of the year. The IMF forecast global growth of 3.1% in 2026, provided that the conflict in the Middle East remained limited. The United States maintained positive dynamics but faced a new inflationary impulse; the eurozone remained weak in terms of growth rates and again saw inflation above the target; China demonstrated 5% growth; India remained the main driver among large economies; Turkey struggled with high inflation; Brazil maintained moderate, more balanced dynamics.

“March 2026 became a moment for Ukraine to test the real strength of its stabilization model. High reserves, international assistance and the NBU’s controlled policy allow the system to be kept in working condition. But the decline in GDP in the first quarter, accelerating inflation and a large trade deficit show that financial stability alone is not enough. The next stage must be the transition from a survival model to a model of productive recovery. This means investment in energy, the defense-industrial complex, processing, logistics, export production, technologies and human capital. Without this, even significant reserves and external assistance will remain only a safety cushion, not a source of long-term development,” Maksym Urakin concluded.

The monthly analytical and statistical product “Economic Monitoring” is available to clients of Interfax-Ukraine.

Head of the “Economic Monitoring” project, PhD in Economics Maksym Urakin

The article presents the key macroeconomic indicators of Ukraine and the global economy as of the end of February 2026. The analysis was prepared on the basis of current data from the State Statistics Service of Ukraine (SSSU), the National Bank of Ukraine (NBU), the International Monetary Fund (IMF), the World Bank, as well as leading national statistical agencies (Eurostat, BEA, NBS, ONS, TurkStat, IBGE). Maksym Urakin, PhD in Economics and founder of the Experts Club information and analytical center, presented an overview of current macroeconomic trends that determined the situation in Ukraine and the world at the beginning of 2026.

Macroeconomic indicators of Ukraine

As of the end of February 2026, the Ukrainian economy maintained a regime of managed macrofinancial stabilization, but compared with January the balance of risks became less comfortable. After the start of the cycle of cautious easing of the NBU’s monetary policy, inflation again accelerated somewhat, international reserves declined from historically high levels, and the foreign exchange market required significant interventions by the regulator. At the same time, the overall macrofinancial situation remained under control thanks to the high level of reserves, external support, continued demand for hryvnia instruments, and the adaptability of business.

The Ukrainian economy ended 2025 with positive but moderate dynamics. According to estimates by the National Bank of Ukraine, real GDP grew by 1.8% in 2025. This meant the preservation of the recovery trend, but the pace of growth was significantly lower than the needs of post-war reconstruction. The main constraints remained the consequences of the war, the shortage of labor, damage to energy infrastructure, weakness of external demand for part of Ukrainian exports, and a high level of uncertainty for investment.

For 2026, the NBU also forecast economic growth of 1.8%. This estimate reflected a cautious scenario: domestic demand and budget expenditures supported economic activity, but energy risks, war losses, and limited export opportunities did not provide grounds to speak of rapid acceleration.

“February 2026 showed that Ukraine is not yet in the phase of full-fledged recovery, but rather in the phase of maintaining macroeconomic manageability. Positive indicators rely to a significant extent on external financing, budget demand, NBU policy, and business adaptation. This creates a stabilization effect, but does not yet form a sufficient internal basis for long-term growth. To move to a new quality of recovery, Ukraine needs not only reserves and partner assistance, but also an increase in production, exports, energy autonomy, and investment in human capital,” Urakin noted.

The inflation picture in February became one of the main signals for macroeconomic policy. According to data from the State Statistics Service, which was commented on by the NBU, consumer inflation in February 2026 accelerated to 7.6% year-on-year, while on a monthly basis prices rose by 1.0%. Core inflation remained at 7.0% y/y. This meant that after the January slowdown, inflationary pressure had not fully disappeared, and some of its components again began to strengthen.

The NBU explained the February dynamics, in particular, by the rise in prices for raw food products, the increase in the cost of certain services, the impact of the energy situation on business costs, and a certain acceleration in fuel prices. At the same time, the regulator noted that the overall inflation trajectory remained close to the forecast. This made it possible not to revise the monetary strategy sharply, but forced caution to be maintained in matters of further rate reductions.

At the end of February, the NBU key policy rate stood at 15.0%. After the reduction at the end of January, the regulator effectively paused, assessing how stable the disinflationary trend was. Such an approach looked logical: the real yield of hryvnia instruments remained an important factor in restraining demand for foreign currency, while the foreign exchange market continued to require the active participation of the National Bank.

“The February acceleration of inflation was not critical, but it clearly showed the limits of rapid monetary easing. Ukraine cannot afford a sharp cheapening of money merely for the sake of short-term economic stimulation, since this could increase demand for foreign currency and destabilize inflation expectations. In the current conditions, the NBU is forced to balance between supporting economic activity and preserving confidence in the hryvnia. That is why every subsequent step to reduce the rate must be very cautious and tied to a real weakening of risks,” Urakin emphasized.

The foreign exchange sector in February remained controlled but tense. As of March 1, 2026, Ukraine’s international reserves amounted to about $54.8 billion. This was 5% less than at the beginning of February, but the level of reserves remained historically high and corresponded to approximately 5.7 months of future imports. The decline in reserves was due primarily to NBU interventions in the foreign exchange market and the state’s debt payments in foreign currency.

In February, the National Bank’s net sale of foreign currency amounted to almost $3 billion. This indicated the preservation of a structural foreign currency deficit in the private sector. External financing inflows partially compensated for this pressure, but did not eliminate the problem itself: the Ukrainian economy imports significantly more goods than it exports, and therefore foreign exchange stability continues to depend substantially on international assistance and NBU reserves.

Foreign trade remained one of the weakest elements of the macroeconomic structure. According to the State Customs Service, in January-February 2026 Ukraine’s trade turnover amounted to $21.3 billion. Imports reached $14.8 billion, while exports amounted to only $6.5 billion. Thus, the trade deficit for the two months exceeded $8 billion. This meant that imports were more than twice as high as exports, while domestic demand for foreign goods, energy resources, equipment, and consumer goods remained significantly higher than foreign exchange earnings from the sale of Ukrainian products abroad.

The largest sources of imports remained China, Poland, and Turkey. In the structure of imports, machinery, equipment, vehicles, and fuel and energy goods played an important role. The largest destinations for Ukrainian exports were Poland, Turkey, and Italy, while the basis of exports remained food products, metals, and certain machine-building items. Such a structure confirms that Ukraine does not yet have a sufficiently diversified export base for a rapid reduction of the trade deficit

“Foreign trade is precisely the key indicator of long-term resilience. Record reserves and international assistance can stabilize the situation, but they do not replace the economy’s own export capacity. When imports exceed exports by more than two times, this means that the country finances a significant part of consumption, investment needs, and the war economy from external sources. Such a model is justified in wartime conditions, but strategically it cannot be permanent. If Ukraine wants to move from a survival model to a development model, it needs to increase the share of products with higher added value, develop processing, logistics, energy resilience, the defense-industrial complex, and technological production,” Urakin stressed.

The budget situation in the first two months of the year also remained tense. According to the Ministry of Finance, in January-February 2026 revenues of the general fund of the state budget amounted to about UAH 466.8 billion, while cash expenditures of the general fund amounted to about UAH 546.5 billion. Tax revenues, customs payments, and international grants played a significant role in revenues, the volume of which over the two months amounted to more than UAH 160 billion.

This confirms that Ukraine’s public finances remain functional, but structurally dependent on external support. Expenditures on defense, security, social payments, and servicing state obligations form a very high level of budgetary burden. Under such conditions, the rhythmic nature of international financing, the government’s ability to attract funds on the domestic market, and the preservation of confidence in hryvnia instruments remain critically important.

“Ukraine’s budget in 2026 remains a budget of wartime resilience. Its task is not only to finance defense and social obligations, but also to maintain confidence in public finances. But when a significant part of revenues is directly or indirectly linked to international support, the country cannot afford to lose the regularity of financing. The government must work simultaneously on three tasks: ensuring external inflows, developing the domestic borrowing market, and gradually expanding its own tax base through the recovery of economic activity,” Urakin noted.

Global economy

As of the end of February 2026, the global economy looked more resilient than could have been expected amid high geopolitical tension, debt risks, and the restructuring of global supply chains. In its January update of the World Economic Outlook, the International Monetary Fund forecast global economic growth of 3.3% in 2026 and 3.2% in 2027. This meant the absence of a global recession scenario, but also did not indicate a return to rapid and synchronized growth.

The United States remained one of the main stabilizers of the global economy. Real U.S. GDP in the fourth quarter of 2025 grew by 1.4% year-on-year after a significantly stronger third quarter, while for 2025 as a whole the economy increased by 2.2%. The main drivers were consumer spending and private investment. At the same time, inflation was gradually declining: in January 2026, CPI stood at 2.4% year-on-year after 2.7% in December 2025. At the end of January, the Federal Reserve kept the federal funds rate range at 3.5–3.75%.

For Ukraine, U.S. economic dynamics had a dual significance. On the one hand, U.S. resilience supported global demand and financial markets. On the other hand, the preservation of relatively high rates meant that global liquidity remained not very cheap, while countries with elevated risk found it more difficult to count on a sharp reduction in the cost of capital.

The eurozone was in another phase of the cycle. Its economy demonstrated weaker growth, but inflation was closer to the target. According to Eurostat estimates, in the fourth quarter of 2025 eurozone GDP grew by 0.3% compared with the previous quarter, and by approximately 1.5% for 2025 as a whole. At the beginning of 2026, the European Central Bank kept the deposit rate at 2.0%, the main refinancing operations rate at 2.15%, and the marginal lending rate at 2.40%. The February inflation background in the eurozone remained close to the target level.

For Ukraine, the European economy is the key external environment through trade, financing, migration, logistics, and the process of integration into the EU. However, weak eurozone growth means that external demand from European partners is unlikely to become an independent powerful driver of Ukrainian exports in 2026. Ukraine must focus not only on the volume of raw material supplies, but also on production integration into European value-added chains.

The United Kingdom remained an example of an economy with moderate growth and a still elevated inflation background. After weak dynamics at the end of 2025, the British economy entered 2026 cautiously: the services sector remained the main pillar, while industry and construction did not provide a strong impulse. Inflation in January 2026 slowed to 3.0% year-on-year, but still exceeded the Bank of England’s target. This limited the space for rapid monetary easing.

“The global economy at the beginning of 2026 did not look crisis-ridden, but it cannot be called uniformly strong. The United States maintained positive dynamics, although no longer at an overheated pace; the eurozone was effectively balancing between low inflation and weak growth; the United Kingdom had slow growth, but still an elevated inflation background. For Ukraine, this means that external demand is unlikely to become a powerful independent driver of recovery. The global environment rather creates moderately favorable financial conditions, but does not guarantee automatic growth of Ukrainian exports,” Urakin noted.

China ended 2025 with a formally strong result: the country’s GDP grew by 5.0%, to more than 140 trillion yuan. In February 2026, consumer inflation in China stood at 1.3% year-on-year, which was higher than previous weak indicators, but still indicated moderate domestic price pressure. China maintained a powerful production and export base, but the issues of domestic demand, the real estate market, and debt burden remained important constraints.

India, by contrast, remained one of the most dynamic large markets in the world. According to the government’s first advance estimate, India’s real GDP in the 2025/26 fiscal year was expected to grow by 7.4%, while in the third quarter of the fiscal year the growth rate was estimated at 7.8%. The main driver remained the services sector, as well as domestic demand. Inflation in India at the beginning of 2026 remained moderate, creating favorable conditions for maintaining high economic dynamics.

Turkey at the beginning of 2026 continued to demonstrate a combination of economic growth and high inflation. According to official estimates, Turkey’s GDP grew by 3.6% in 2025, but inflation in February 2026 amounted to more than 31% year-on-year. This meant that the country maintained business activity and domestic demand, but at the cost of high price pressure and the need for strict macroeconomic policy.

Brazil looked more balanced. Its GDP grew by 2.3% in 2025, to 12.7 trillion reais at current prices, while IPCA inflation for 2025 amounted to 4.26%. Growth was supported by the agricultural sector, services, and industry. For the global economy, Brazil remained an important example of a large market that combines raw material potential, domestic demand, and a relatively controlled inflation background.

“China, India, Turkey, and Brazil show very well how different the dynamics of large developing economies have become. China has great scale and a strong production base, but still faces structural imbalances and insufficiently strong domestic demand. India demonstrates the most convincing combination of high growth and moderate inflation. Turkey maintains momentum, but the price of this growth is a very high inflation background. Brazil is moving more moderately, but more balanced. For Ukraine, it is important to look at these examples practically: in global competition, those economies win that are able simultaneously to maintain macro-stability, a production base, exports, and domestic investment demand,” Urakin believes.

Conclusions

As of the end of February 2026, Ukraine maintained macrofinancial manageability, but February showed that stabilization remains fragile. Inflation accelerated to 7.6% y/y, the key policy rate remained at 15.0%, international reserves declined to about $54.8 billion, and the foreign exchange market required almost $3 billion in net NBU interventions during the month. At the same time, reserves remained sufficient, the budget was executed with the support of domestic revenues and international grants, and the economy maintained positive dynamics.

The main weaknesses of the Ukrainian economy remained the high trade deficit, the dependence of the budget on external financing, war risks, labor shortages, energy vulnerability, and insufficient export diversification. Positive factors included high international reserves, controlled monetary policy, business adaptability, the continuation of international support, and the preservation of the functionality of public finances.

The global economy at the same moment demonstrated moderate resilience. The IMF forecast global growth at 3.3% in 2026. The United States remained strong, but no longer with excessive overheating; the eurozone balanced between weak growth and almost target-level inflation; China maintained scale, but had structural challenges; India remained the main growth driver among large economies; Turkey was fighting high inflation; Brazil demonstrated moderately positive dynamics.

“February 2026 became a reminder for Ukraine that macrofinancial stability in wartime conditions is not a final result, but a process of constant balancing. The country has a financial cushion in the form of reserves and partner support, but long-term resilience will depend on the ability to create its own economic base for growth. For this, investments in energy, processing, logistics, export-oriented production, technologies, and human capital remain critically important in 2026. Without this, even high reserves and external assistance will remain only a financial cushion, and not a source of long-term development,” Urakin summarized.

The monthly analytical and statistical product “Economic Monitoring” is available to Interfax-Ukraine clients.

Maksym Urakin, Head of the “Economic Monitoring” project, Director of Development and Marketing at Interfax-Ukraine, Candidate of Economic Sciences, Doctor of Philosophy in History, and founder of the Experts Club information and analytical center

The office real estate market of Kyiv and Ukraine’s largest cities by May 2026 is demonstrating cautious stabilization after several years of shocks caused by the pandemic, the full-scale war, business relocation and the transition of some companies to a hybrid work format. The main demand factors remain building safety, completed renovation, autonomous infrastructure, the availability of shelters and the ability to move in quickly without significant capital expenditures.

Kyiv still remains the country’s largest office market. According to InVenture estimates, the total competitive supply of office real estate in Kyiv in 2025 decreased to 2.10 million sq. m, while the vacancy rate fell to 18.5%. The annual volume of gross take-up amounted to about 160 thousand sq. m, which is 26% more than a year earlier. At the same time, about 40% of take-up was related not to the organic expansion of business, but to the forced relocation of companies from damaged properties.

According to the Confederation of Builders of Ukraine, citing a CBRE Ukraine presentation, in the first half of 2025 demand for offices in Kyiv grew by 16%, to 82 thousand sq. m, while supply decreased by 3%, to 2.1 million sq. m, due to damage to office buildings. Vacancy in the market stood at about 21%, while 20% of demand was formed by tenants forced to relocate from properties affected by strikes.

“The office market in Kyiv can no longer be assessed according to pre-war logic. Today, a tenant chooses not simply an address or a building class, but the ability of a property to ensure business continuity. A shelter, generators, engineering systems, the safety of the district and the readiness of the premises for quick move-in have become parameters as important as the rental rate,” says the founder of the Experts Club analytical center, Candidate of Economic Sciences Maksym Urakin.

Rental rates in Kyiv remain relatively stable, but the market retains pronounced differentiation. According to InVenture, effective rates for class A offices without renovation at the end of 2025 amounted to $14-18 per sq. m per month excluding VAT and operating expenses, while for offices with renovation they amounted to $19-25 per sq. m. Asking rates for class A were in the range of $16-27 per sq. m, and for class B — $8-18 per sq. m.

In 2026, Kyiv’s office market remains a tenant’s market: property owners are forced to offer flexible terms, divide large areas into smaller blocks, invest in ready-made finishing and increase the autonomy of buildings. At the same time, the best class A and B+ properties with shelters, stable power supply and high-quality operation are holding demand better than outdated buildings and premises without renovation.

CBRE Ukraine senior office real estate consultant Anastasiia Kachan noted that in Kyiv the connection between the rate and the specific location of a business center has strengthened: now not only proximity to the metro matters, but also the location relative to infrastructure or military facilities. According to her, each business center can effectively operate outside the typical rules of its submarket or district.

IT companies remain the key tenants in Kyiv, but the structure of demand has become broader. Activity is also being formed by the defense sector, medical companies, professional services, consulting, logistics, representative offices of international organizations and part of the business related to reconstruction. According to CBU/CBRE Ukraine, in 2025 demand from the military sector increased noticeably, and the market began adapting offers to such needs.

“The office has ceased to be a place of daily presence for all employees, but it has not lost its significance for management, communication and corporate culture. Companies are optimizing space, but they are not abandoning a quality office. Therefore, demand is shifting from large monofunctional spaces to more flexible, safe and technological formats,” Experts Club notes.

Development activity remains minimal. In 2025, not a single new business center was commissioned in Kyiv, and by the end of 2026, according to InVenture’s estimate, about 27 thousand sq. m may enter the market, but commissioning deadlines may be postponed due to security risks, limited financing and a weak level of pre-leasing.

The situation in Ukraine’s major cities is heterogeneous. Lviv remains one of the most active regional office markets thanks to business relocation, the presence of the IT sector, proximity to the EU border and a relatively higher level of safety compared with the eastern and southern regions. According to Forbes Ukraine, by the end of 2025 vacancy in Lviv business centers decreased to 25%, while rental rates remained at $7-15 per sq. m.

In 2026, the Lviv market can be considered the second most important after Kyiv in terms of office demand, but its scale is limited. For tenants, ready-made premises, transport accessibility, energy resilience and the possibility of accommodating small or medium-sized teams are important. Large deals remain rare, while some companies prefer hybrid formats or coworking spaces.

Dnipro retains the role of an industrial, logistics and service center, but the city’s office market remains more local and less institutionalized than in Kyiv or Lviv. Demand is formed by regional companies, service businesses, retail operators, logistics, medical services and part of production structures. Due to proximity to an area of increased risks, tenants are especially sensitive to the safety, cost and autonomy of premises.

Odesa remains an important southern business center, but the city’s office market is strongly dependent on the overall security situation, port and logistics activity, tourism, trade and service business. The market includes both classic offices in central districts and premises in new multifunctional complexes. Demand in 2026 remains selective: tenants choose ready-made small premises, while large corporate deals are limited.

Kharkiv remains the most difficult of the large office markets due to the high level of security risks and proximity to the frontline zone. A significant part of business operates in a reduced, distributed or remote format. Nevertheless, the market has not stopped completely: demand remains for small offices, service premises, spaces for local business and properties with minimal operating costs.

“In regional cities, office real estate has ceased to be a single segment. Lviv operates as a market of relocation and IT, Dnipro as a market of industrial and service business, Odesa as a southern trade and logistics hub, and Kharkiv as a market of survival and adaptation. Therefore, comparing them only by rental rate is no longer correct: it is more important to look at safety, the tenant profile and the resilience of the local economy,” Maksym Urakin believes.

A common trend for all major cities has been the reassessment of office space. Companies more often choose smaller areas, completed renovation, flexible lease terms and buildings where the owner assumes part of the capital expenditures. Premises without renovation and large blocks in outdated properties remain less liquid, since tenants are not ready to invest in expensive fit-out amid high uncertainty.

Another factor is autonomy. After energy crises and attacks on infrastructure, offices with generators, stable internet, backup systems, shelters and high-quality management gained a competitive advantage. In some cases, such characteristics allow properties to maintain their rate even with overall high market vacancy.

According to InVenture’s assessment, the investment logic of office real estate in 2026 has become more cautious: before the pandemic and the war, the typical payback period for office premises was estimated at about 7-8 years, whereas in 2026, 10-12 years is already becoming the norm for most assets. At the same time, the best properties with a strong tenant and a successful location may show more attractive results, but this is rather an exception.

According to Experts Club’s forecast, by the end of 2026 Ukraine’s office market will move according to a scenario of slow recovery without a sharp increase in rates. Kyiv will retain the status of the main market, Lviv the status of the main regional center of demand, while Dnipro, Odesa and Kharkiv will develop mainly at the expense of local tenants and selective deals.

“The main risk for the market is not the absence of demand, but its quality. Demand exists, but it has become cautious, rational and demanding. Tenants want to pay not for meters, but for a guaranteed ability to work. This means that office real estate in Ukraine is gradually moving from a space model to a service and resilience model,” Experts Club summarizes.

Thus, by May 2026, the office real estate market of Kyiv and major Ukrainian cities remains in a transitional phase. It has already passed through the period of a shock decline, but has not yet returned to a full-fledged investment cycle. The most sought-after offices are becoming safe, ready-to-use, energy-resilient and flexible ones. Outdated properties without renovation, autonomy and a clear operational model will continue to lose competitiveness.

This article presents key macroeconomic indicators for Ukraine and the global economy as of the end of December 2025. The analysis is based on current data from the State Statistics Service of Ukraine (SSSU), the National Bank of Ukraine (NBU), the International Monetary Fund (IMF), the World Bank, as well as leading national statistical agencies (Eurostat, BEA, NBS, ONS, TurkStat, IBGE). Maksym Urakin, Director of Development and Marketing at Interfax-Ukraine, Candidate of Economic Sciences, Doctor of Philosophy in History, and founder of the Experts Club information and analytical center, presented an overview of current macroeconomic trends that shaped the situation in Ukraine and the world at the beginning of 2026.

Ukraine’s Macroeconomic Indicators

As of the end of January 2026, the Ukrainian economy entered the new year with a combination of two opposing trends: on the one hand—a gradual easing of inflationary pressure, record-high international reserves, and a stable situation in the foreign exchange market; on the other—war risks, high budget dependence on external financing, weak exports, and a structural foreign exchange deficit in the private sector.

According to the NBU’s estimates, Ukraine’s real GDP grew by 1.8% in 2025. This meant that the economy maintained positive momentum for the third consecutive year, but the pace of recovery remained moderate. The NBU attributed this trend to resilient domestic demand, accommodative fiscal policy, business adaptability, and measures to maintain macrofinancial stability. At the same time, physical export volumes declined due to low agricultural inventories, weak external demand for mining and metallurgical products, and constraints related to the electricity shortage at the end of the year.

In January 2026, the disinflationary trend continued. According to data from the State Statistics Service (SSU), as commented on by the NBU, consumer inflation slowed to 7.4% year-on-year, while prices rose by 0.7% month-on-month. Core inflation also declined—to 7.0% y/y. The NBU attributed this trend to a reduction in labor market imbalances, the secondary effects of the high harvests of 2025, competition from certain imported goods, and a stable situation in the foreign exchange market. At the same time, the regulator noted the first signs of increasing pressure from raw food products.

According to Maksym Urakin, January 2026 became an important test for the Ukrainian economy following the conclusion of a challenging 2025. The decline in inflation to 7.4% showed that tight monetary conditions, stabilization of the foreign exchange market, and an improvement in the supply of food products had yielded results. However, in his assessment, this result should not be interpreted as a complete normalization.

“At the beginning of 2026, Ukraine experienced a rare combination for a war economy—inflation was falling, the foreign exchange market remained under control, reserves reached a historic high, and the economy did not lose its positive momentum. However, this does not mean that the country has entered a classic recovery phase. We are dealing rather with a stabilization regime in which many indicators look better thanks to external financing, budget expenditures, business adaptation, and NBU policy. If international aid were removed from this framework or a new severe energy or currency shock were to occur, the system’s stability would once again be in serious doubt,” Urakin noted.

The NBU’s January decision on the discount rate was one of the key signals of the start of the year. On January 29, 2026, the National Bank announced the start of a cycle of monetary policy easing and a reduction in the discount rate from 15.5% to 15.0% effective January 30. The regulator attributed this to a sustained decline in inflationary pressures and a reduction in risks associated with external financing. At the same time, the NBU emphasized that inflation expectations remained relatively high, and a return of inflation to the 5% target is expected only on the policy horizon.

This decision did not signify a shift to a soft monetary policy in the full sense. Real yields on hryvnia-denominated instruments remained positive, and continued interest in hryvnia assets was one of the key factors restraining demand for foreign currency. In its January Inflation Report, the NBU noted that maintaining a high rate in previous months had supported demand for hryvnia-denominated assets, and individuals’ investments in government bonds and deposits in the national currency continued to grow.

“Lowering the discount rate to 15% was a cautious and logical step, but it should not be interpreted as a signal of imminent cheapening of money. Ukraine remains in a state of war, with high budgetary needs and a significant private-sector foreign exchange deficit. Therefore, the NBU is effectively trying to navigate a very narrow corridor: on the one hand, not to stifle economic activity with excessively expensive money, and on the other, not to lose control over inflation expectations and the foreign exchange market. In such a situation, every rate cut should not be a political gesture, but the result of a real easing of risks,” Urakin emphasized.

The external sector remained the main pillar of Ukraine’s macrofinancial stability. As of the end of January 2026, Ukraine’s international reserves rose to $57.7 billion, setting a new all-time high. The NBU attributed the increase in reserves to inflows of external financing, which largely offset the National Bank’s net foreign exchange sales and the country’s foreign currency debt payments.

In its January Inflation Report, the NBU also noted that in 2025, Ukraine received $52.4 billion in international financial support, including $32.7 billion from the EU, $12.0 billion from the U.S., and $3.4 billion from Canada. At the beginning of 2026, reserves stood at $57.3 billion, equivalent to 5.8 months of future imports, and the NBU’s forecast projected an increase in international reserves to $65 billion by the end of 2026 and to $71 billion by the end of 2028.

At the same time, foreign trade remained a weak point. According to customs data, Ukraine’s trade turnover in January 2026 amounted to $9.9 billion: imports – $6.7 billion, exports – $3.2 billion. This meant that the trade deficit remained high, and domestic demand for imports continued to significantly exceed foreign exchange earnings from exports.

“Record reserves are a strong stabilizing factor, but they should not create the illusion of self-sufficiency. Ukraine’s balance of payments continues to rely heavily on foreign aid rather than the economy’s export capacity. When imports more than double exports in merchandise trade, it means that the country is financing a significant portion of current consumption and military needs with external resources. This is justified in wartime, but strategically, such a model cannot be permanent. “In 2026, the key task should be to expand the country’s own foreign exchange base through exports, processing, energy resilience, and investments in production,” Urakin emphasized.

The budget situation at the beginning of 2026 also remained relatively under control, but structurally strained. According to aggregated data on budget execution, in January 2026, state budget revenues amounted to approximately 303.8 billion UAH, while expenditures totaled approximately 286.2 billion UAH. This monthly picture did not negate the overall problem of the year: public finances remained dependent on the regularity of external financing, domestic borrowing, and the government’s ability to maintain confidence in hryvnia-denominated instruments.

The Global Economy

The global economy at the end of January 2026 appeared more resilient than expected at the end of 2025, but this resilience was uneven. In its January update to the World Economic Outlook, the IMF projected global economic growth of 3.3% in 2026 and 3.2% in 2027. The Fund attributed this to investments in technology, fiscal and monetary support, more favorable financial conditions, and the resilience of the private sector. At the same time, the IMF warned of risks associated with overoptimistic expectations regarding the technology sector and a potential escalation of geopolitical tensions.

In the U.S., the economy maintained positive momentum, but the pace slowed by the end of 2025. According to a preliminary BEA estimate, U.S. real GDP grew by 1.4% year-over-year in the fourth quarter of 2025 following a stronger third quarter, and by 2.2% for the full year 2025. Growth was driven by consumer spending and investment, while exports and government spending held back the result. Inflation in the U.S. remained moderately above target: the Consumer Price Index rose by 2.7% from December 2024 to December 2025, and core CPI by 2.6%. On January 28, 2026, the Federal Reserve kept the target range for the federal funds rate at 3.5–3.75%.

The eurozone entered early 2026 with inflation nearly at target but with weak economic momentum. According to Eurostat estimates, annual inflation in the Eurozone stood at 2.0% in December 2025, down from 2.1% in November. Services inflation remained the highest component at 3.4%, while the energy component was negative. ECB rates at the start of 2026 remained at the levels set in 2025: the deposit rate at 2.0%, the main refinancing operations rate at 2.15%, and the marginal lending rate at 2.40%.

The United Kingdom remained one of the most controversial major economies in Europe. According to ONS data, the UK’s GDP grew by 1.3% in 2025, driven in part by the services sector. However, inflation accelerated to 3.4% year-on-year in December 2025, remaining significantly above the Bank of England’s target. In December 2025, the Bank of England cut its base rate to 3.75%, but the decision was passed by a narrow 5–4 majority, indicating that disagreements within the regulator regarding the pace of further easing persisted.

“The global economy at the start of 2026 did not appear to be in crisis, but it could not be described as uniformly strong. The U.S. maintained positive momentum, though no longer at an overheated pace; the eurozone was effectively balancing between low inflation and weak growth; the UK experienced slow growth but still faced elevated inflationary pressures. For Ukraine, this means that external demand is unlikely to become a powerful independent driver of recovery. The global environment tends to create moderately favorable financial conditions, but does not guarantee automatic growth in Ukrainian exports,” noted Maksym Urakin.

China ended 2025 with a formally strong result. According to data from the National Bureau of Statistics of China, the country’s GDP grew by 5.0% in 2025, reaching 140.1879 trillion yuan. The primary sector grew by 3.9%, the secondary sector by 4.5%, and the tertiary sector by 5.4%. At the same time, the inflation picture remained weak: in December 2025, the CPI rose by only 0.8% year-on-year, while core inflation rose by 1.2%. This indicated that the Chinese economy maintained its manufacturing and export strength, but domestic consumer demand remained insufficiently robust.

India, by contrast, remained the main growth driver among major economies. According to the government’s first preliminary estimate, India’s real GDP was projected to grow by 7.4% in the 2025/26 fiscal year, following 6.5% in the 2024/25 fiscal year. Nominal GDP was estimated to grow by 8.0%, with the services sector being the main driver of real GVA. At the same time, inflation remained very low: in December 2025, the CPI stood at 1.33% year-on-year, and food inflation was negative.

At the start of 2026, Turkey remained an example of an economy with relatively high growth but a challenging inflationary legacy. According to TurkStat, inflation stood at 30.89% year-on-year in December 2025 and at 30.65% in January 2026. Subsequent official data from the Turkish Ministry of Trade showed that the country’s economy grew by 3.6% in 2025 and by 3.4% year-on-year in the fourth quarter.

Brazil ended 2025 on a cautiously positive note. According to IBGE data, IPCA inflation in 2025 stood at 4.26%, while the December monthly rate was 0.33%. Brazil’s GDP in 2025 grew by 2.3%, reaching 12.7 trillion reais at current prices. Growth was observed in all three major sectors: agriculture, industry, and services.

“China, India, Turkey, and Brazil clearly demonstrate how diverse the dynamics of major emerging economies have become. China has a large scale and a strong manufacturing base, but its price momentum remains weak. India demonstrates the most compelling combination of high growth and low inflation. Turkey maintains its momentum, but the price of this growth is a very high inflation rate. Brazil is moving more moderately but more balanced. “It is important for Ukraine to view these examples not in the abstract, but practically: in global competition, the economies that win are those capable of simultaneously maintaining macro-stability, a manufacturing base, exports, and domestic investment demand,” Urakin believes.

Conclusions

As of the end of January 2026, Ukraine was in a mode of managed macrofinancial stabilization. Inflation was declining, the discount rate had been cautiously reduced to 15%, international reserves had reached a historic high, and the economy maintained positive growth after the end of 2025. At the same time, this stability remained dependent on three key conditions: regular external financing, a controlled situation in the foreign exchange market, and the state’s ability to sustain domestic demand without triggering a new wave of inflation.

The main risks for Ukraine at the start of 2026 remained war-related losses, energy infrastructure deficits, weak exports, high budgetary needs, dependence on international aid, and a structural labor shortage. A positive factor was that the NBU had record reserves and room for cautious policy easing. A negative factor was that the real production and export base had not yet created sufficient domestic resources for self-sustained recovery.

The global economy was not in a phase of deep crisis at that time. The IMF projected global growth of 3.3% in 2026; the U.S. remained stable, the eurozone stayed close to its inflation target, India demonstrated high growth rates, and China remained a large but structurally mixed source of global demand. At the same time, none of these external factors guaranteed Ukraine a rapid recovery without domestic decisions.

“January 2026 showed that Ukraine is entering the new year not from a position of economic breakthrough, but from a position of maintained manageability. This is important because, in the context of war, the very ability to control inflation, the exchange rate, budget needs, and reserves is already a significant achievement. But the next stage will be more challenging: the country needs to transition from a model of survival and stabilization to a model of productive recovery. This means investing in energy, the defense-industrial complex, processing, logistics, export-oriented industries, human capital, and technology. Without this, even record reserves and foreign aid will remain merely a financial cushion, not a source of long-term growth,” concluded Maksym Urakin.

The monthly analytical and statistical product “Economic Monitoring” is available to Interfax-Ukraine clients.

Maksym Urakin, Head of the “Economic Monitoring” project, Director of Development and Marketing at Interfax-Ukraine, Candidate of Economic Sciences, Doctor of Philosophy in History, and founder of the Experts Club information and analytical center

ECONOMY, EXPERTS_CLUB, MACROECONOMICS, MONITORING, Ukrainian_economy, URAKIN