The office real estate market of Kyiv and Ukraine’s largest cities by May 2026 is demonstrating cautious stabilization after several years of shocks caused by the pandemic, the full-scale war, business relocation and the transition of some companies to a hybrid work format. The main demand factors remain building safety, completed renovation, autonomous infrastructure, the availability of shelters and the ability to move in quickly without significant capital expenditures.

Kyiv still remains the country’s largest office market. According to InVenture estimates, the total competitive supply of office real estate in Kyiv in 2025 decreased to 2.10 million sq. m, while the vacancy rate fell to 18.5%. The annual volume of gross take-up amounted to about 160 thousand sq. m, which is 26% more than a year earlier. At the same time, about 40% of take-up was related not to the organic expansion of business, but to the forced relocation of companies from damaged properties.

According to the Confederation of Builders of Ukraine, citing a CBRE Ukraine presentation, in the first half of 2025 demand for offices in Kyiv grew by 16%, to 82 thousand sq. m, while supply decreased by 3%, to 2.1 million sq. m, due to damage to office buildings. Vacancy in the market stood at about 21%, while 20% of demand was formed by tenants forced to relocate from properties affected by strikes.

“The office market in Kyiv can no longer be assessed according to pre-war logic. Today, a tenant chooses not simply an address or a building class, but the ability of a property to ensure business continuity. A shelter, generators, engineering systems, the safety of the district and the readiness of the premises for quick move-in have become parameters as important as the rental rate,” says the founder of the Experts Club analytical center, Candidate of Economic Sciences Maksym Urakin.

Rental rates in Kyiv remain relatively stable, but the market retains pronounced differentiation. According to InVenture, effective rates for class A offices without renovation at the end of 2025 amounted to $14-18 per sq. m per month excluding VAT and operating expenses, while for offices with renovation they amounted to $19-25 per sq. m. Asking rates for class A were in the range of $16-27 per sq. m, and for class B — $8-18 per sq. m.

In 2026, Kyiv’s office market remains a tenant’s market: property owners are forced to offer flexible terms, divide large areas into smaller blocks, invest in ready-made finishing and increase the autonomy of buildings. At the same time, the best class A and B+ properties with shelters, stable power supply and high-quality operation are holding demand better than outdated buildings and premises without renovation.

CBRE Ukraine senior office real estate consultant Anastasiia Kachan noted that in Kyiv the connection between the rate and the specific location of a business center has strengthened: now not only proximity to the metro matters, but also the location relative to infrastructure or military facilities. According to her, each business center can effectively operate outside the typical rules of its submarket or district.

IT companies remain the key tenants in Kyiv, but the structure of demand has become broader. Activity is also being formed by the defense sector, medical companies, professional services, consulting, logistics, representative offices of international organizations and part of the business related to reconstruction. According to CBU/CBRE Ukraine, in 2025 demand from the military sector increased noticeably, and the market began adapting offers to such needs.

“The office has ceased to be a place of daily presence for all employees, but it has not lost its significance for management, communication and corporate culture. Companies are optimizing space, but they are not abandoning a quality office. Therefore, demand is shifting from large monofunctional spaces to more flexible, safe and technological formats,” Experts Club notes.

Development activity remains minimal. In 2025, not a single new business center was commissioned in Kyiv, and by the end of 2026, according to InVenture’s estimate, about 27 thousand sq. m may enter the market, but commissioning deadlines may be postponed due to security risks, limited financing and a weak level of pre-leasing.

The situation in Ukraine’s major cities is heterogeneous. Lviv remains one of the most active regional office markets thanks to business relocation, the presence of the IT sector, proximity to the EU border and a relatively higher level of safety compared with the eastern and southern regions. According to Forbes Ukraine, by the end of 2025 vacancy in Lviv business centers decreased to 25%, while rental rates remained at $7-15 per sq. m.

In 2026, the Lviv market can be considered the second most important after Kyiv in terms of office demand, but its scale is limited. For tenants, ready-made premises, transport accessibility, energy resilience and the possibility of accommodating small or medium-sized teams are important. Large deals remain rare, while some companies prefer hybrid formats or coworking spaces.

Dnipro retains the role of an industrial, logistics and service center, but the city’s office market remains more local and less institutionalized than in Kyiv or Lviv. Demand is formed by regional companies, service businesses, retail operators, logistics, medical services and part of production structures. Due to proximity to an area of increased risks, tenants are especially sensitive to the safety, cost and autonomy of premises.

Odesa remains an important southern business center, but the city’s office market is strongly dependent on the overall security situation, port and logistics activity, tourism, trade and service business. The market includes both classic offices in central districts and premises in new multifunctional complexes. Demand in 2026 remains selective: tenants choose ready-made small premises, while large corporate deals are limited.

Kharkiv remains the most difficult of the large office markets due to the high level of security risks and proximity to the frontline zone. A significant part of business operates in a reduced, distributed or remote format. Nevertheless, the market has not stopped completely: demand remains for small offices, service premises, spaces for local business and properties with minimal operating costs.

“In regional cities, office real estate has ceased to be a single segment. Lviv operates as a market of relocation and IT, Dnipro as a market of industrial and service business, Odesa as a southern trade and logistics hub, and Kharkiv as a market of survival and adaptation. Therefore, comparing them only by rental rate is no longer correct: it is more important to look at safety, the tenant profile and the resilience of the local economy,” Maksym Urakin believes.

A common trend for all major cities has been the reassessment of office space. Companies more often choose smaller areas, completed renovation, flexible lease terms and buildings where the owner assumes part of the capital expenditures. Premises without renovation and large blocks in outdated properties remain less liquid, since tenants are not ready to invest in expensive fit-out amid high uncertainty.

Another factor is autonomy. After energy crises and attacks on infrastructure, offices with generators, stable internet, backup systems, shelters and high-quality management gained a competitive advantage. In some cases, such characteristics allow properties to maintain their rate even with overall high market vacancy.

According to InVenture’s assessment, the investment logic of office real estate in 2026 has become more cautious: before the pandemic and the war, the typical payback period for office premises was estimated at about 7-8 years, whereas in 2026, 10-12 years is already becoming the norm for most assets. At the same time, the best properties with a strong tenant and a successful location may show more attractive results, but this is rather an exception.

According to Experts Club’s forecast, by the end of 2026 Ukraine’s office market will move according to a scenario of slow recovery without a sharp increase in rates. Kyiv will retain the status of the main market, Lviv the status of the main regional center of demand, while Dnipro, Odesa and Kharkiv will develop mainly at the expense of local tenants and selective deals.

“The main risk for the market is not the absence of demand, but its quality. Demand exists, but it has become cautious, rational and demanding. Tenants want to pay not for meters, but for a guaranteed ability to work. This means that office real estate in Ukraine is gradually moving from a space model to a service and resilience model,” Experts Club summarizes.

Thus, by May 2026, the office real estate market of Kyiv and major Ukrainian cities remains in a transitional phase. It has already passed through the period of a shock decline, but has not yet returned to a full-fledged investment cycle. The most sought-after offices are becoming safe, ready-to-use, energy-resilient and flexible ones. Outdated properties without renovation, autonomy and a clear operational model will continue to lose competitiveness.

This article presents key macroeconomic indicators for Ukraine and the global economy as of the end of December 2025. The analysis is based on current data from the State Statistics Service of Ukraine (SSSU), the National Bank of Ukraine (NBU), the International Monetary Fund (IMF), the World Bank, as well as leading national statistical agencies (Eurostat, BEA, NBS, ONS, TurkStat, IBGE). Maksym Urakin, Director of Development and Marketing at Interfax-Ukraine, Candidate of Economic Sciences, Doctor of Philosophy in History, and founder of the Experts Club information and analytical center, presented an overview of current macroeconomic trends that shaped the situation in Ukraine and the world at the beginning of 2026.

Ukraine’s Macroeconomic Indicators

As of the end of January 2026, the Ukrainian economy entered the new year with a combination of two opposing trends: on the one hand—a gradual easing of inflationary pressure, record-high international reserves, and a stable situation in the foreign exchange market; on the other—war risks, high budget dependence on external financing, weak exports, and a structural foreign exchange deficit in the private sector.

According to the NBU’s estimates, Ukraine’s real GDP grew by 1.8% in 2025. This meant that the economy maintained positive momentum for the third consecutive year, but the pace of recovery remained moderate. The NBU attributed this trend to resilient domestic demand, accommodative fiscal policy, business adaptability, and measures to maintain macrofinancial stability. At the same time, physical export volumes declined due to low agricultural inventories, weak external demand for mining and metallurgical products, and constraints related to the electricity shortage at the end of the year.

In January 2026, the disinflationary trend continued. According to data from the State Statistics Service (SSU), as commented on by the NBU, consumer inflation slowed to 7.4% year-on-year, while prices rose by 0.7% month-on-month. Core inflation also declined—to 7.0% y/y. The NBU attributed this trend to a reduction in labor market imbalances, the secondary effects of the high harvests of 2025, competition from certain imported goods, and a stable situation in the foreign exchange market. At the same time, the regulator noted the first signs of increasing pressure from raw food products.

According to Maksym Urakin, January 2026 became an important test for the Ukrainian economy following the conclusion of a challenging 2025. The decline in inflation to 7.4% showed that tight monetary conditions, stabilization of the foreign exchange market, and an improvement in the supply of food products had yielded results. However, in his assessment, this result should not be interpreted as a complete normalization.

“At the beginning of 2026, Ukraine experienced a rare combination for a war economy—inflation was falling, the foreign exchange market remained under control, reserves reached a historic high, and the economy did not lose its positive momentum. However, this does not mean that the country has entered a classic recovery phase. We are dealing rather with a stabilization regime in which many indicators look better thanks to external financing, budget expenditures, business adaptation, and NBU policy. If international aid were removed from this framework or a new severe energy or currency shock were to occur, the system’s stability would once again be in serious doubt,” Urakin noted.

The NBU’s January decision on the discount rate was one of the key signals of the start of the year. On January 29, 2026, the National Bank announced the start of a cycle of monetary policy easing and a reduction in the discount rate from 15.5% to 15.0% effective January 30. The regulator attributed this to a sustained decline in inflationary pressures and a reduction in risks associated with external financing. At the same time, the NBU emphasized that inflation expectations remained relatively high, and a return of inflation to the 5% target is expected only on the policy horizon.

This decision did not signify a shift to a soft monetary policy in the full sense. Real yields on hryvnia-denominated instruments remained positive, and continued interest in hryvnia assets was one of the key factors restraining demand for foreign currency. In its January Inflation Report, the NBU noted that maintaining a high rate in previous months had supported demand for hryvnia-denominated assets, and individuals’ investments in government bonds and deposits in the national currency continued to grow.

“Lowering the discount rate to 15% was a cautious and logical step, but it should not be interpreted as a signal of imminent cheapening of money. Ukraine remains in a state of war, with high budgetary needs and a significant private-sector foreign exchange deficit. Therefore, the NBU is effectively trying to navigate a very narrow corridor: on the one hand, not to stifle economic activity with excessively expensive money, and on the other, not to lose control over inflation expectations and the foreign exchange market. In such a situation, every rate cut should not be a political gesture, but the result of a real easing of risks,” Urakin emphasized.

The external sector remained the main pillar of Ukraine’s macrofinancial stability. As of the end of January 2026, Ukraine’s international reserves rose to $57.7 billion, setting a new all-time high. The NBU attributed the increase in reserves to inflows of external financing, which largely offset the National Bank’s net foreign exchange sales and the country’s foreign currency debt payments.

In its January Inflation Report, the NBU also noted that in 2025, Ukraine received $52.4 billion in international financial support, including $32.7 billion from the EU, $12.0 billion from the U.S., and $3.4 billion from Canada. At the beginning of 2026, reserves stood at $57.3 billion, equivalent to 5.8 months of future imports, and the NBU’s forecast projected an increase in international reserves to $65 billion by the end of 2026 and to $71 billion by the end of 2028.

At the same time, foreign trade remained a weak point. According to customs data, Ukraine’s trade turnover in January 2026 amounted to $9.9 billion: imports – $6.7 billion, exports – $3.2 billion. This meant that the trade deficit remained high, and domestic demand for imports continued to significantly exceed foreign exchange earnings from exports.

“Record reserves are a strong stabilizing factor, but they should not create the illusion of self-sufficiency. Ukraine’s balance of payments continues to rely heavily on foreign aid rather than the economy’s export capacity. When imports more than double exports in merchandise trade, it means that the country is financing a significant portion of current consumption and military needs with external resources. This is justified in wartime, but strategically, such a model cannot be permanent. “In 2026, the key task should be to expand the country’s own foreign exchange base through exports, processing, energy resilience, and investments in production,” Urakin emphasized.

The budget situation at the beginning of 2026 also remained relatively under control, but structurally strained. According to aggregated data on budget execution, in January 2026, state budget revenues amounted to approximately 303.8 billion UAH, while expenditures totaled approximately 286.2 billion UAH. This monthly picture did not negate the overall problem of the year: public finances remained dependent on the regularity of external financing, domestic borrowing, and the government’s ability to maintain confidence in hryvnia-denominated instruments.

The Global Economy

The global economy at the end of January 2026 appeared more resilient than expected at the end of 2025, but this resilience was uneven. In its January update to the World Economic Outlook, the IMF projected global economic growth of 3.3% in 2026 and 3.2% in 2027. The Fund attributed this to investments in technology, fiscal and monetary support, more favorable financial conditions, and the resilience of the private sector. At the same time, the IMF warned of risks associated with overoptimistic expectations regarding the technology sector and a potential escalation of geopolitical tensions.

In the U.S., the economy maintained positive momentum, but the pace slowed by the end of 2025. According to a preliminary BEA estimate, U.S. real GDP grew by 1.4% year-over-year in the fourth quarter of 2025 following a stronger third quarter, and by 2.2% for the full year 2025. Growth was driven by consumer spending and investment, while exports and government spending held back the result. Inflation in the U.S. remained moderately above target: the Consumer Price Index rose by 2.7% from December 2024 to December 2025, and core CPI by 2.6%. On January 28, 2026, the Federal Reserve kept the target range for the federal funds rate at 3.5–3.75%.

The eurozone entered early 2026 with inflation nearly at target but with weak economic momentum. According to Eurostat estimates, annual inflation in the Eurozone stood at 2.0% in December 2025, down from 2.1% in November. Services inflation remained the highest component at 3.4%, while the energy component was negative. ECB rates at the start of 2026 remained at the levels set in 2025: the deposit rate at 2.0%, the main refinancing operations rate at 2.15%, and the marginal lending rate at 2.40%.

The United Kingdom remained one of the most controversial major economies in Europe. According to ONS data, the UK’s GDP grew by 1.3% in 2025, driven in part by the services sector. However, inflation accelerated to 3.4% year-on-year in December 2025, remaining significantly above the Bank of England’s target. In December 2025, the Bank of England cut its base rate to 3.75%, but the decision was passed by a narrow 5–4 majority, indicating that disagreements within the regulator regarding the pace of further easing persisted.

“The global economy at the start of 2026 did not appear to be in crisis, but it could not be described as uniformly strong. The U.S. maintained positive momentum, though no longer at an overheated pace; the eurozone was effectively balancing between low inflation and weak growth; the UK experienced slow growth but still faced elevated inflationary pressures. For Ukraine, this means that external demand is unlikely to become a powerful independent driver of recovery. The global environment tends to create moderately favorable financial conditions, but does not guarantee automatic growth in Ukrainian exports,” noted Maksym Urakin.

China ended 2025 with a formally strong result. According to data from the National Bureau of Statistics of China, the country’s GDP grew by 5.0% in 2025, reaching 140.1879 trillion yuan. The primary sector grew by 3.9%, the secondary sector by 4.5%, and the tertiary sector by 5.4%. At the same time, the inflation picture remained weak: in December 2025, the CPI rose by only 0.8% year-on-year, while core inflation rose by 1.2%. This indicated that the Chinese economy maintained its manufacturing and export strength, but domestic consumer demand remained insufficiently robust.

India, by contrast, remained the main growth driver among major economies. According to the government’s first preliminary estimate, India’s real GDP was projected to grow by 7.4% in the 2025/26 fiscal year, following 6.5% in the 2024/25 fiscal year. Nominal GDP was estimated to grow by 8.0%, with the services sector being the main driver of real GVA. At the same time, inflation remained very low: in December 2025, the CPI stood at 1.33% year-on-year, and food inflation was negative.

At the start of 2026, Turkey remained an example of an economy with relatively high growth but a challenging inflationary legacy. According to TurkStat, inflation stood at 30.89% year-on-year in December 2025 and at 30.65% in January 2026. Subsequent official data from the Turkish Ministry of Trade showed that the country’s economy grew by 3.6% in 2025 and by 3.4% year-on-year in the fourth quarter.

Brazil ended 2025 on a cautiously positive note. According to IBGE data, IPCA inflation in 2025 stood at 4.26%, while the December monthly rate was 0.33%. Brazil’s GDP in 2025 grew by 2.3%, reaching 12.7 trillion reais at current prices. Growth was observed in all three major sectors: agriculture, industry, and services.

“China, India, Turkey, and Brazil clearly demonstrate how diverse the dynamics of major emerging economies have become. China has a large scale and a strong manufacturing base, but its price momentum remains weak. India demonstrates the most compelling combination of high growth and low inflation. Turkey maintains its momentum, but the price of this growth is a very high inflation rate. Brazil is moving more moderately but more balanced. “It is important for Ukraine to view these examples not in the abstract, but practically: in global competition, the economies that win are those capable of simultaneously maintaining macro-stability, a manufacturing base, exports, and domestic investment demand,” Urakin believes.

Conclusions

As of the end of January 2026, Ukraine was in a mode of managed macrofinancial stabilization. Inflation was declining, the discount rate had been cautiously reduced to 15%, international reserves had reached a historic high, and the economy maintained positive growth after the end of 2025. At the same time, this stability remained dependent on three key conditions: regular external financing, a controlled situation in the foreign exchange market, and the state’s ability to sustain domestic demand without triggering a new wave of inflation.

The main risks for Ukraine at the start of 2026 remained war-related losses, energy infrastructure deficits, weak exports, high budgetary needs, dependence on international aid, and a structural labor shortage. A positive factor was that the NBU had record reserves and room for cautious policy easing. A negative factor was that the real production and export base had not yet created sufficient domestic resources for self-sustained recovery.

The global economy was not in a phase of deep crisis at that time. The IMF projected global growth of 3.3% in 2026; the U.S. remained stable, the eurozone stayed close to its inflation target, India demonstrated high growth rates, and China remained a large but structurally mixed source of global demand. At the same time, none of these external factors guaranteed Ukraine a rapid recovery without domestic decisions.

“January 2026 showed that Ukraine is entering the new year not from a position of economic breakthrough, but from a position of maintained manageability. This is important because, in the context of war, the very ability to control inflation, the exchange rate, budget needs, and reserves is already a significant achievement. But the next stage will be more challenging: the country needs to transition from a model of survival and stabilization to a model of productive recovery. This means investing in energy, the defense-industrial complex, processing, logistics, export-oriented industries, human capital, and technology. Without this, even record reserves and foreign aid will remain merely a financial cushion, not a source of long-term growth,” concluded Maksym Urakin.

The monthly analytical and statistical product “Economic Monitoring” is available to Interfax-Ukraine clients.

Maksym Urakin, Head of the “Economic Monitoring” project, Director of Development and Marketing at Interfax-Ukraine, Candidate of Economic Sciences, Doctor of Philosophy in History, and founder of the Experts Club information and analytical center

ECONOMY, EXPERTS_CLUB, MACROECONOMICS, MONITORING, Ukrainian_economy, URAKIN

Canada is among the group of countries that consistently enjoy a high level of positive perception within Ukrainian society. According to the survey results, 76.2% of respondents describe their attitude toward Canada as positive. Specifically, 39.4% of Ukrainians indicated a “completely positive” attitude, while another 36.8% described it as “mostly positive.” This distribution of responses indicates not only broad support but also a deeply entrenched positive image of the country.

At the same time, the level of negative perception of Canada is minimal—only 2.3% (1.4% “mostly negative” and 0.9% “completely negative”). This is one of the lowest figures among all countries included in the study. This result confirms that negative assessments are isolated and do not significantly influence overall perception.

The share of neutral responses is 20.3%, which is a moderate figure. This means that while most Ukrainians have already formed a positive attitude toward Canada, a certain portion of respondents lack sufficient personal experience or information to make a clear assessment. At the same time, only 1.2% of respondents were unable to decide on an answer, which further underscores the high level of certainty in public opinion regarding this country.

Overall, Canada demonstrates one of the most balanced and positive perception profiles: the combination of a high share of “fully positive” assessments with virtually no negativity forms a solid reputation capital. This indicates that the country’s image in Ukraine is based not only on general perceptions but also on a systematic view of Canada as a reliable partner.

“Canada is among those countries toward which Ukrainians have formed not just a positive, but a consistently positive attitude. This is the result of long-term interaction, support, and presence in the Ukrainian information space. In such cases, even neutral responses do not blur the overall picture, but only underscore its consistency,” noted Oleksandr Pozniy, director of the research company Active Group.

Thus, Canada ranks among the top countries with the highest level of trust in Ukrainian society. The combination of high positive perception and minimal negativity creates a foundation for further strengthening bilateral relations, particularly in the areas of politics, the economy, and humanitarian cooperation.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, Canada ranks 41st in total trade volume of goods with Ukraine, with a figure of $416.2 million.

Imports of Canadian goods are twice as high as Ukrainian exports, resulting in a trade deficit of $139.9 million.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, CANADA, EXPERTS CLUB, Pozniy, SOCIOLOGY, SURVEY, UKRAINE, URAKIN

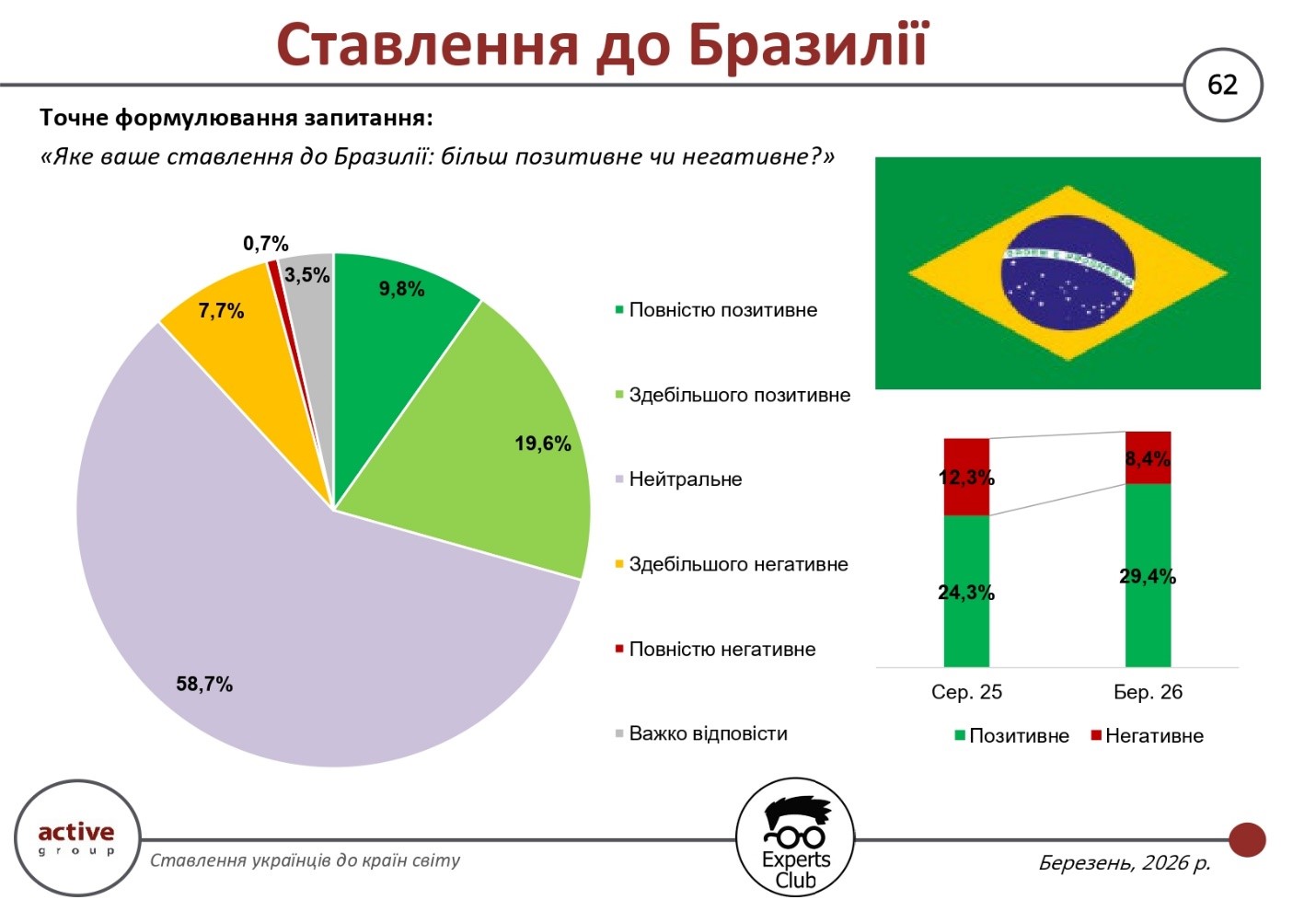

According to the results of a public opinion poll conducted in March 2026 by the research company Active Group in collaboration with the Experts Club information and analytical center, perceptions of Brazil in Ukrainian society show moderately positive trends, although a high level of neutrality remains the key characteristic. Most Ukrainians do not have a clearly formed attitude toward this country, but the share of positive assessments is gradually increasing.

Overall, the positive attitude toward Brazil stands at 29.4%, which is a noticeable increase compared to August 2025 (24.3%). At the same time, 9.8% of respondents chose the “completely positive” option, and another 19.6% selected “mostly positive.” This trend indicates a gradual strengthening of the country’s positive image, although it remains relatively moderate.

At the same time, negative assessments have decreased—from 12.3% to 8.4%. Within the structure of negative perceptions, 7.7% fall under the “mostly negative” category and only 0.7% under “completely negative.” This means that critical perceptions of Brazil in Ukraine are diminishing and are not systemic in nature.

Most telling is the high level of neutrality—58.7% of respondents. This indicates that for most Ukrainians, Brazil remains a country that does not occupy a significant place on the informational or political agenda. The absence of active interaction or regular information flows shapes precisely this model of perception.

Additionally, 3.5% of respondents were unable to determine their position. Combined with neutral assessments, this creates a significant segment of “undecided attitudes,” which could potentially change depending on the development of bilateral relations or the country’s media presence.

From a dynamic perspective, Brazil shows a positive trend: an increase in the share of positive assessments is accompanied by a simultaneous decrease in negative ones. This indicates a gradual improvement in the country’s image in Ukraine, although it is occurring against a backdrop of general inertia in neutral perception.

Overall, Brazil remains a “peripheral” country for Ukrainians in terms of emotional perception, yet with potential for further improvement of its image. The high proportion of neutral assessments means that future changes in perception will largely depend on the level of economic, diplomatic, and informational interaction between the two countries.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, Brazil ranks 50th in total trade volume of goods with Ukraine, with a figure of $335.6 million. At the same time, imports from Brazil are nearly four times higher than Ukrainian exports, resulting in a bilateral trade deficit of $193.5 million.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, BRAZIL, EXPERTS CLUB, Pozniy, SOCIOLOGY, SURVEY, UKRAINE, URAKIN

According to the results of a sociological survey conducted in March 2026 by the research company Active Group in collaboration with the Experts Club information and analytical center, perceptions of Mexico in Ukrainian society are characterized by a high level of neutrality and a relatively moderate share of both positive and negative assessments. At the same time, the trend shows a gradual increase in positive attitudes and a simultaneous decrease in negative ones, indicating a cautious normalization of the country’s image.

The total share of positive attitudes toward Mexico stands at 21.5%, of which 5.4% of respondents chose the option “completely positive,” and another 16.1% selected “mostly positive.” Compared to August 2025, this figure has increased (from 19.7% to 21.4%), indicating a gradual strengthening of positive perceptions, although they remain relatively limited.

Negative assessments, conversely, show a decline—from 10.0% to 8.6%. Within the structure of negative attitudes, 7.7% fall into the “mostly negative” category and only 0.9% into the “completely negative” category. This means that while a critical perception of Mexico exists, it is not dominant and is rather moderate in nature.

Neutrality remains the key characteristic of Ukrainians’ attitudes toward Mexico—66.2% of respondents chose this option. Such a high figure indicates the absence of a clearly formed image of the country in the public consciousness. For most respondents, Mexico is neither an important political partner nor a country with distinct emotional significance.

Additionally, 3.7% of respondents were unable to decide on their assessment, which, together with the high proportion of neutral responses, forms a significant segment of “undetermined attitudes.” This means that perceptions of Mexico depend to a large extent on the level of awareness and the country’s presence in the Ukrainian information space.

From a dynamic perspective, the situation appears moderately positive: the increase in positive assessments is accompanied by a simultaneous decrease in negative ones. This may indicate the gradual formation of a more favorable, albeit still weakly expressed, image of the country.

Ultimately, Mexico remains a country with a predominantly neutral perception among Ukrainians, but with a trend toward a slow improvement in its image. The high proportion of neutral assessments creates significant potential for future changes, which will depend on the development of economic, cultural, and informational ties between the countries.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, Mexico ranks 49th in total trade volume with Ukraine, which amounts to $350.0 million. At the same time, imports of Mexican goods exceed Ukrainian exports by more than seven times, resulting in a trade deficit of $264.7 million.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, EXPERTS CLUB, MEXICO, Pozniy, SOCIOLOGY, SURVEY, UKRAINE, URAKIN

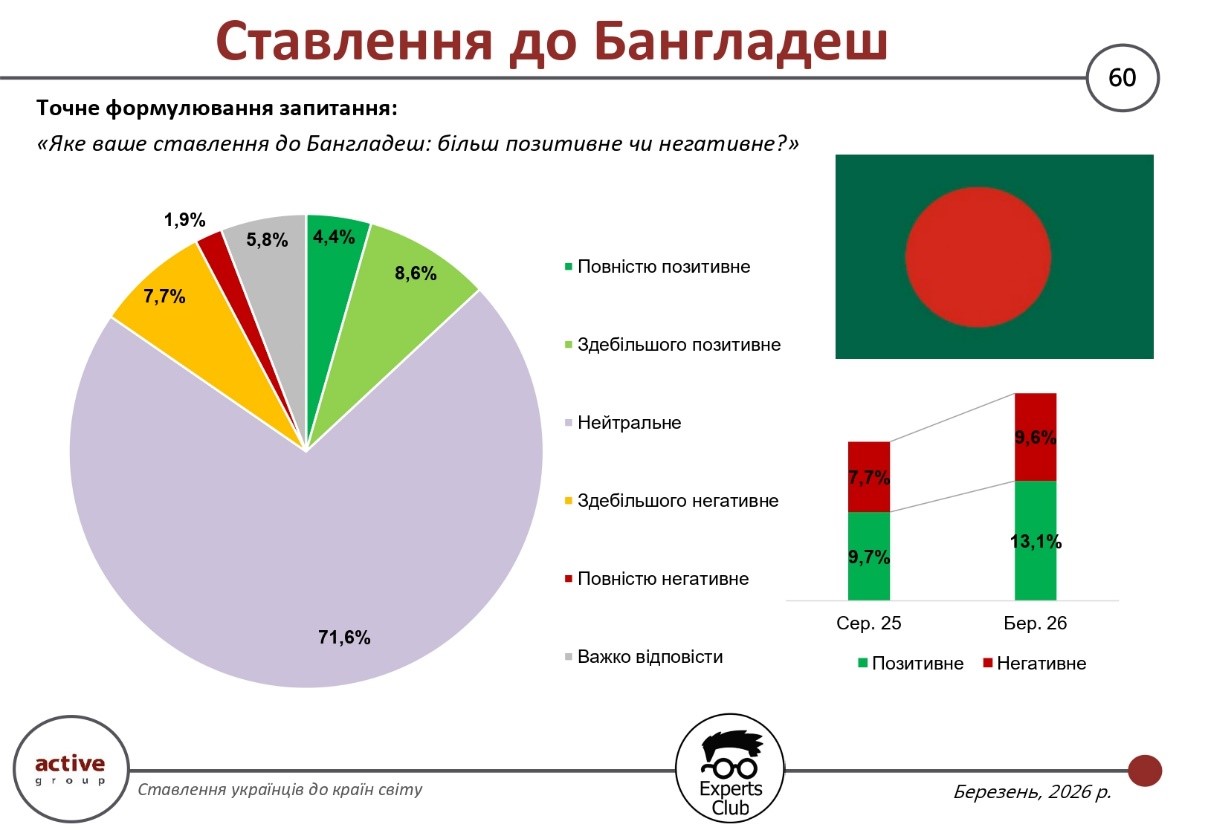

The results of a survey conducted in March 2026 by the research company Active Group in collaboration with the Experts Club information and analytical center showed that perceptions of Bangladesh in Ukrainian society are characterized by a predominance of neutral assessments and a relatively low level of both positive and negative attitudes. At the same time, compared to the previous survey, there has been a gradual increase in both positive and negative assessments, indicating a certain intensification of perceptions of this country.

The overall share of positive attitudes stands at 13.0% (specifically, 4.4% “completely positive” and 8.6% “mostly positive”). This is a relatively low figure, indicating a limited level of emotional engagement among Ukrainians regarding Bangladesh. At the same time, the trend shows an increase in positive attitudes—from 9.7% to 13.1%—which may indicate a gradual expansion of the country’s informational or economic presence in Ukrainian perceptions.

Negative assessments also show an increase—from 7.7% to 9.6%. In terms of composition, they consist of 7.7% “mostly negative” and 1.9% “completely negative” attitudes. Although these figures remain relatively low, their trend indicates the emergence of a more defined, albeit still limited, negative backdrop.

At the same time, a key characteristic of attitudes toward Bangladesh is the high level of neutrality—71.6%. This is one of the highest figures among the countries surveyed, indicating low awareness or a lack of clear associations. In practical terms, this means that for most Ukrainians, Bangladesh is not a country associated with significant political, economic, or cultural reference points.

Additionally, 5.8% of respondents were undecided, which, combined with the high proportion of neutral assessments, forms a significant segment of “undetermined perception.” This creates potential for future changes—both toward strengthening a positive image and toward an increase in critical attitudes, depending on the informational context.

In summary, Bangladesh remains a country with a minimally established image in the perception of Ukrainians. Despite a slight increase in both positive and negative assessments, neutrality is the defining factor. This means that the further evolution of attitudes will depend primarily on the country’s level of presence in the Ukrainian information space and the development of bilateral contacts.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, Bangladesh ranks 48th in total trade volume with Ukraine, with a figure of $355.8 million. The bilateral trade balance is relatively close to equilibrium, but imports still slightly exceed exports, resulting in a small trade deficit of $26.9 million.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, BANGLADESH, EXPERTS CLUB, Pozniy, SOCIOLOGY, SURVEY, UKRAINE, URAKIN