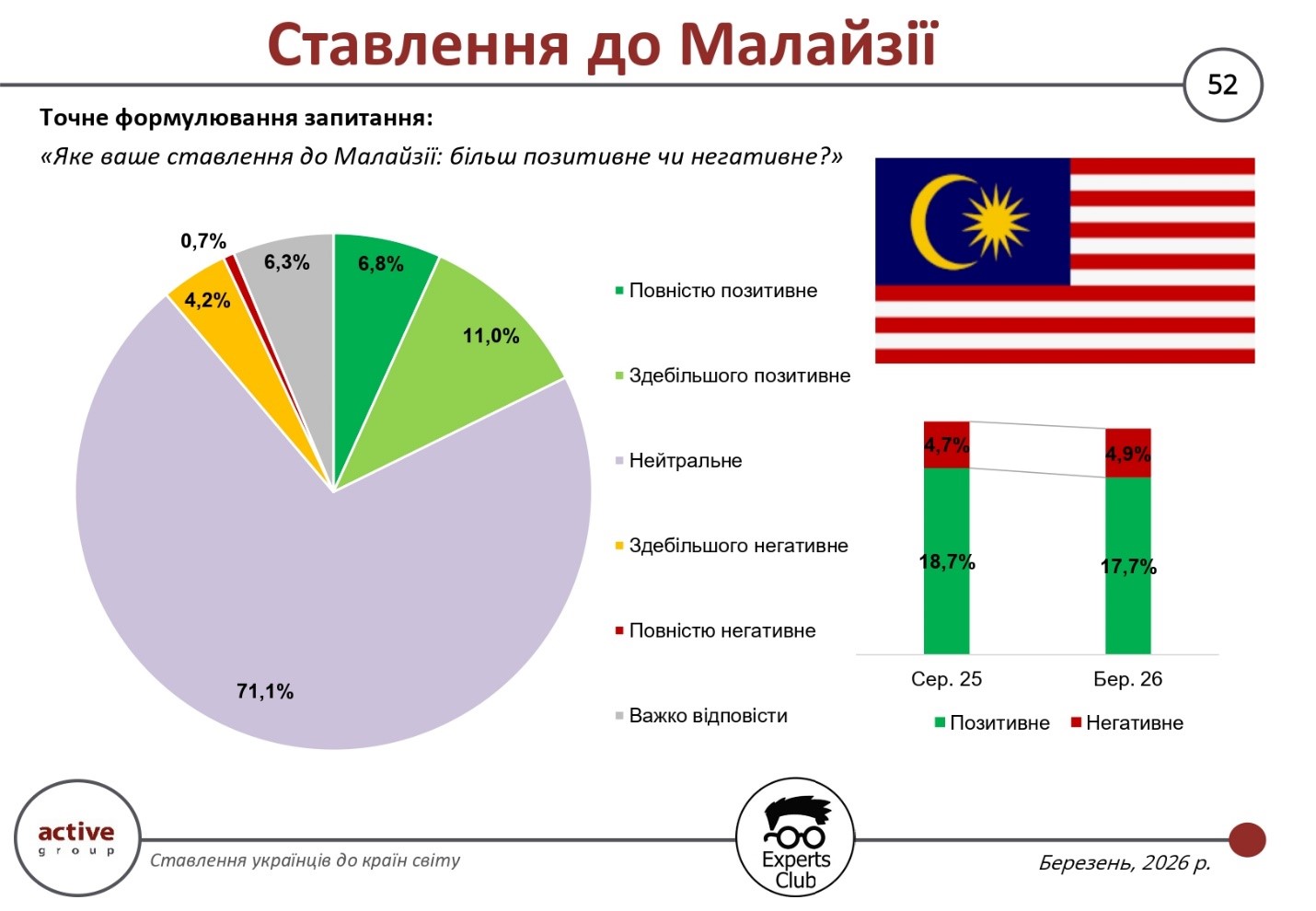

The results of a survey conducted in March 2026 by the research company Active Group in collaboration with the Experts Club information and analytical center indicate that Ukrainians’ attitudes toward Malaysia are characterized by a high proportion of neutral assessments and relatively low levels of both positive and negative perceptions. Overall, 17.7% of respondents expressed a positive attitude toward this country, which is slightly lower compared to August 2025 (18.7%). At the same time, negative attitudes remained virtually unchanged—4.9% versus 4.7% in the previous period.

The breakdown of responses shows a clear dominance of neutral views: 71.1% of respondents have no formed attitude toward Malaysia. This is one of the highest figures among the countries surveyed, indicating the limited presence of this country in the information landscape and in the everyday experience of Ukrainians.

Positive assessments are formed primarily due to a moderately favorable perception: only 6.8% of respondents chose the “completely positive” option, while 11.0% selected “mostly positive.” This distribution indicates the absence of a clearly defined positive image, even among those who generally view the country favorably.

Negative assessments also remain at a low level: 4.2% of respondents expressed a “mostly negative” attitude, and only 0.7% selected “completely negative.” The share of those who could not answer is 6.3%, which further underscores the uncertainty in perceptions of this country.

The trend in indicators compared to August 2025 shows a slight decline in positive perceptions while negative assessments remain stable. This means that Malaysia is not the subject of active image change in Ukrainian society, and its perception remains inertial and largely independent of current international events.

In a broader context, these results indicate that Southeast Asian countries, including Malaysia, do not yet occupy a prominent place in the structure of Ukrainians’ foreign policy or economic priorities. The high proportion of neutral assessments indicates significant potential for image-building, but at the same time points to the absence of a clearly defined perception.

Thus, Ukrainians’ attitude toward Malaysia can be characterized as neutral-indifferent: the country does not evoke significant negativity, but is also not associated with processes important to Ukrainian society that shape a positive perception of other states.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, Malaysia ranks 39th in total trade volume with Ukraine, with a figure of $454.1 million. At the same time, imports from Malaysia are more than three times higher than Ukrainian exports, resulting in a trade deficit of $239.9 million.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, EXPERTS CLUB, MALAYSIA, Pozniy, SOCIOLOGY, SURVEY, UKRAINE, URAKIN

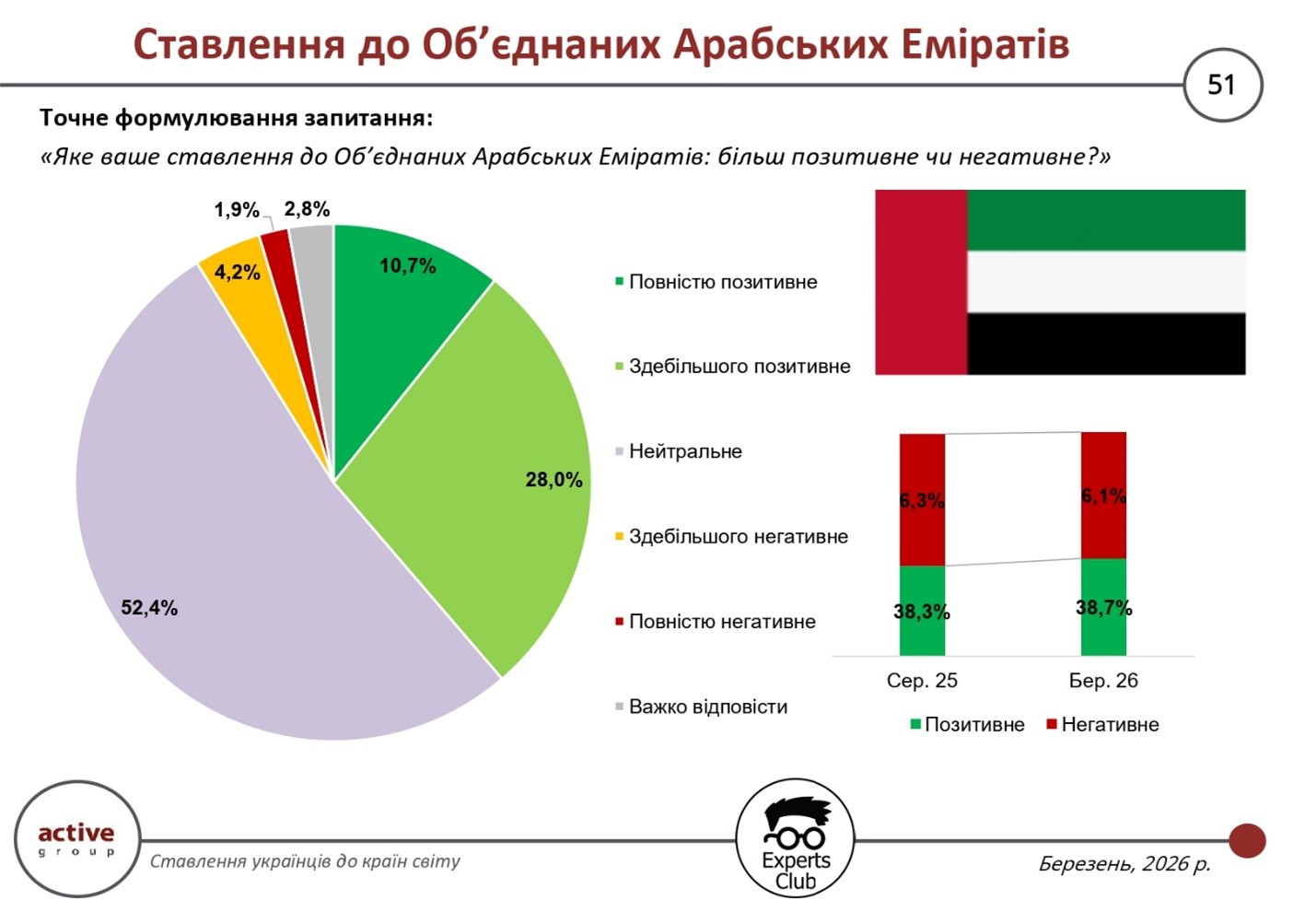

The results of a survey conducted in March 2026 by the research company Active Group in collaboration with the Experts Club information and analytical center show that Ukrainians’ attitude toward the United Arab Emirates remains stable and is characterized by a combination of moderate positivity and a significant proportion of neutral assessments. Overall, 38.7% of respondents describe their attitude as positive, which is virtually unchanged from August 2025 (38.3%). At the same time, negative attitudes have decreased slightly—from 6.3% to 6.1%.

The distribution of responses indicates a predominance of neutral perceptions: 52.4% of respondents do not have a clearly formed opinion regarding the UAE. The positive segment consists of 10.7% who selected “completely positive” and 28.0% who selected “mostly positive.” This pattern indicates a generally favorable backdrop, though without a high level of emotional engagement.

Negative assessments remain relatively low: 4.2% of respondents chose “mostly negative,” and 1.9% chose “completely negative.” The share of those who could not decide is 2.8%. This confirms that the UAE does not evoke significant negative perceptions in Ukrainian society, yet it also does not form a clearly positive image.

The change between August 2025 and March 2026 is minimal. A slight increase in positive assessments is accompanied by an equally slight decrease in negative ones, indicating a stabilization of attitudes. At the same time, a key characteristic remains the high proportion of neutral responses, which exceeds half of all respondents.

In a broader context, this means that Ukrainians perceive the UAE as an economically interesting country, but one that is not close enough or well understood. The absence of sharp fluctuations in the indicators confirms that the established image is stable but not deeply integrated into the public consciousness.

“In the case of countries such as the United Arab Emirates, we see a typical example of a predominantly neutral perception. This means that Ukrainians’ level of knowledge and experience of interaction with this country remains limited, even despite economic contacts. At the same time, this creates potential for the positive image to grow, provided there is a more active presence in Ukraine’s information and economic spheres,” noted Maksym Urakin, founder of the Experts Club information and analytical center.

Thus, the survey results indicate that Ukrainians’ attitudes toward the UAE are stable and moderately positive, though neutrality remains the dominant feature. This opens opportunities for further shaping the country’s image through economic cooperation, investment, and public diplomacy.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, the United Arab Emirates ranks 38th in total trade volume with Ukraine, amounting to $456.7 million. At the same time, Ukraine has a trade surplus with the UAE of $214.1 million, as exports of Ukrainian goods exceed imports.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, EXPERTS CLUB, Pozniy, SOCIOLOGY, SURVEY, UAE, UKRAINE, URAKIN

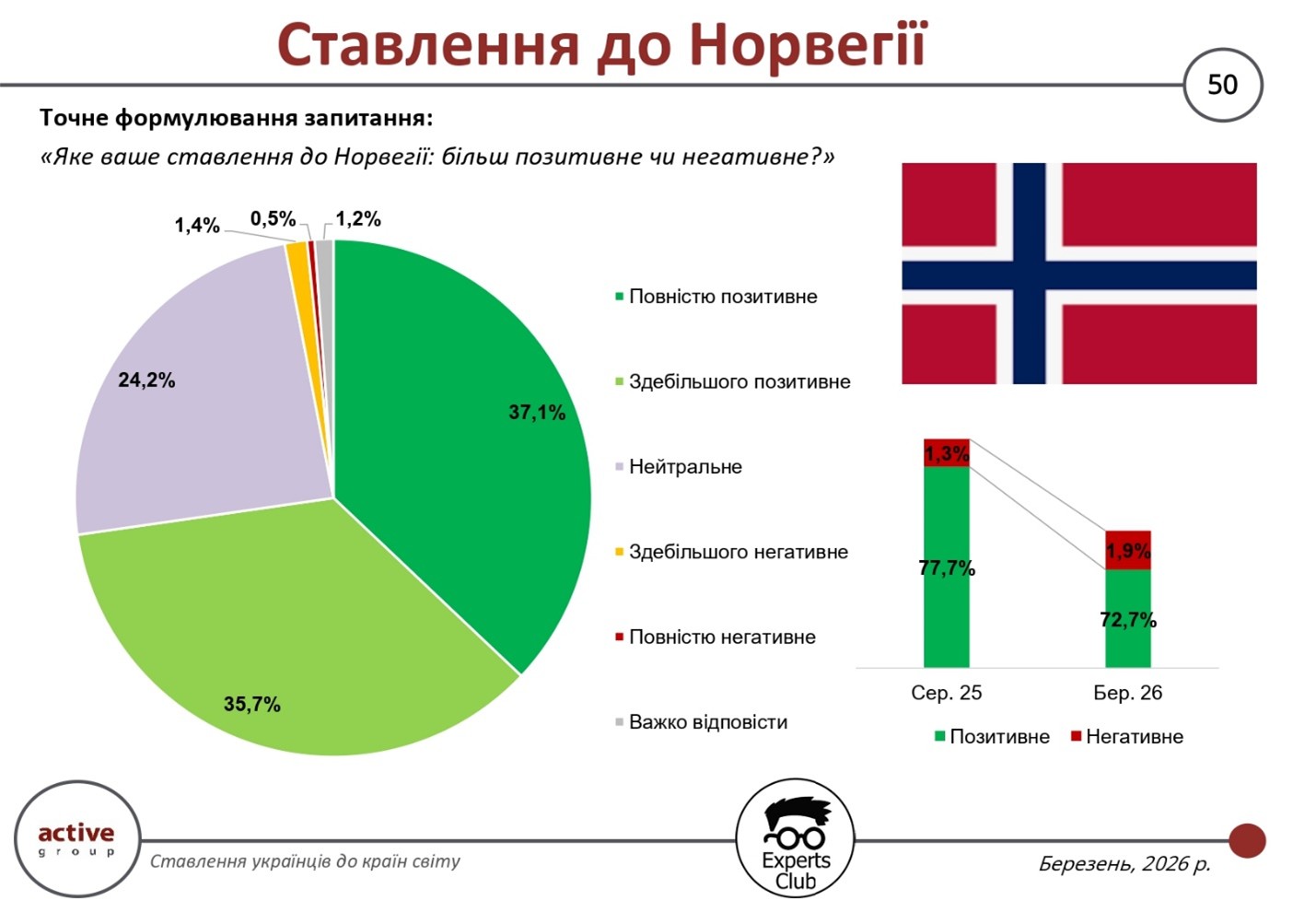

The results of a public opinion poll conducted in March 2026 by the research firm Active Group in collaboration with the Experts Club information and analytical center show that Norway continues to rank among the countries with the highest level of positive perception among Ukrainians. Overall, 72.7% of respondents rate their attitude toward this country as positive, although this figure has declined slightly from 77.7% compared to August 2025. At the same time, negative ratings remain minimal—1.9% versus 1.3% previously.

The breakdown of responses shows a consistently high level of positivity. The share of those who have a completely positive attitude toward Norway stands at 37.1%, while another 35.7% selected the “mostly positive” option. Thus, the dominance of positive perception is undeniable. At the same time, 24.2% of respondents hold a neutral position, indicating a certain degree of distance in their perception of the country, despite its generally favorable image.

Negative assessments remain marginal: 1.4% of respondents chose “mostly negative,” and another 0.5% selected “completely negative.” The share of those who could not decide on an answer is 1.2%. This distribution of responses confirms that Norway practically does not evoke rejection in the public consciousness of Ukrainians.

The decline in the positive rating by a few percentage points is accompanied not so much by an increase in negative views as by an increase in neutral assessments. This means that the changes are more a matter of a redistribution of responses than a fundamental shift in attitude. Ukrainians continue to perceive Norway as a stable and friendly partner, although the intensity of this perception has decreased somewhat.

In the broader context of the study, Norway belongs to the group of Northern and Western European countries that demonstrate the highest levels of positive attitude. This reflects a general trend in Ukrainian society toward countries with a high level of development, a stable political system, and consistent support for Ukraine.

“Ukrainians quite clearly differentiate countries based on levels of trust and actual support. In the case of Norway, we see a consistently high level of positive attitude, which is not shaped by current events but rather by a long-term perception of this country as a reliable partner. Even a slight decline in the indicators does not change the overall picture—it remains one of the most positive among all the countries surveyed,” noted Oleksandr Pozniy, director of the research company Active Group.

Thus, the survey results confirm that Norway maintains a strong position in Ukrainians’ positive perception. The slight downward trend is not systematic and is not accompanied by an increase in negative sentiment. This indicates a well-established and stable image of the country, which is not dependent on short-term factors and remains one of the strongest in Europe.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, Norway ranks 37th in total trade volume with Ukraine, with a figure of $502.5 million. At the same time, imports of Norwegian goods significantly exceed exports of Ukrainian products, resulting in a negative bilateral trade balance of $430.7 million.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club think tank’s website.

ACTIVE GROUP, EXPERTS CLUB, NORWAY, Pozniy, SOCIOLOGY, SURVEY, UKRAINE, URAKIN

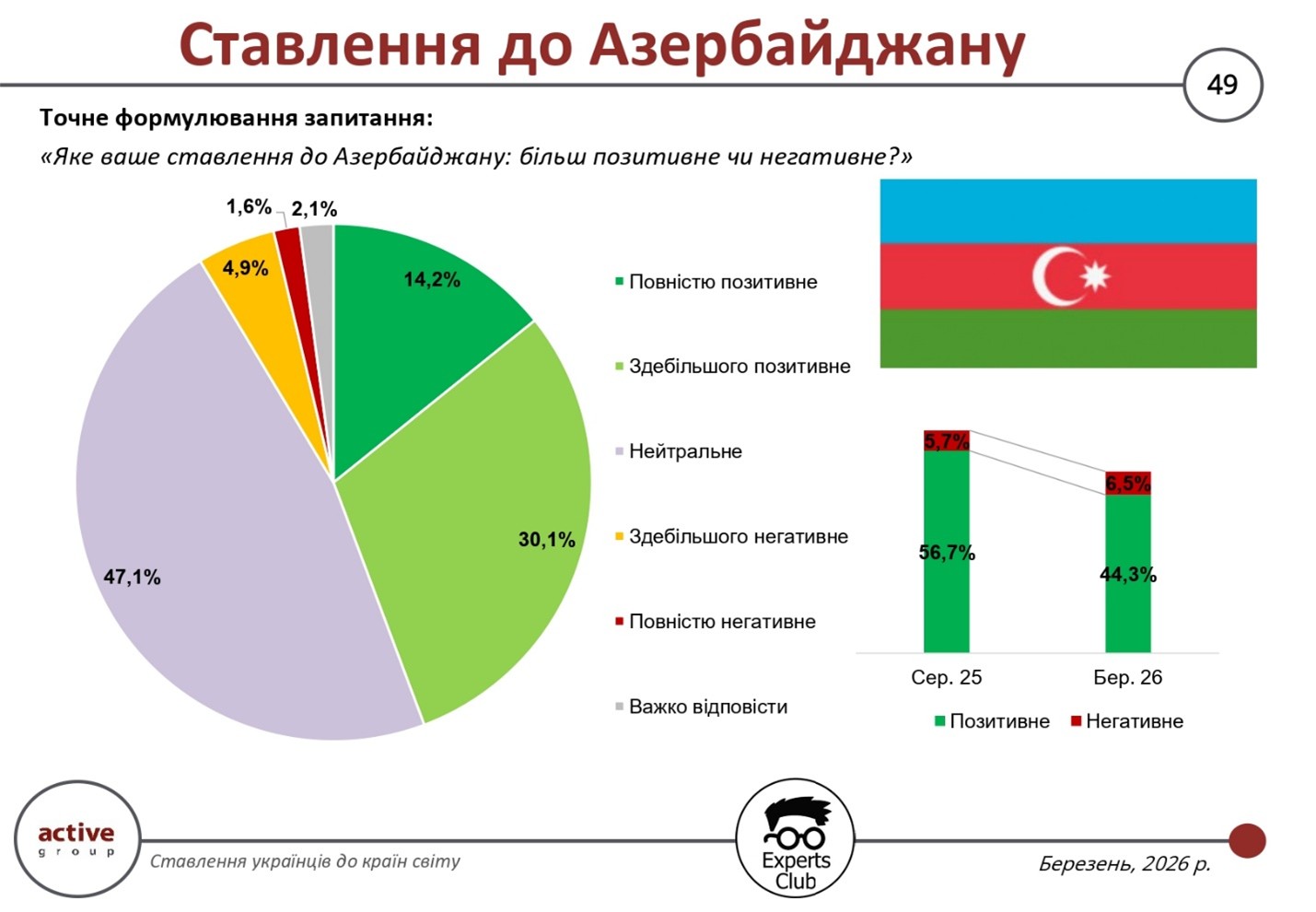

According to a survey conducted in March 2026 by the research firm Active Group in collaboration with the Experts Club information and analytical center, Ukrainians’ attitudes toward Azerbaijan show a noticeable decline in positive sentiment and an increase in the proportion of neutral assessments. Overall, 44.3% of respondents expressed a positive attitude toward this country, whereas in August 2025 this figure stood at 56.7%. At the same time, the share of negative assessments rose slightly—from 5.7% to 6.5%—which indicates not a sharp deterioration in perception, but rather a shift in responses toward neutrality.

The breakdown of responses confirms this trend. The share of those who view Azerbaijan entirely positively stands at 14.2%, while another 30.1% selected the “mostly positive” option. At the same time, the largest category was the neutral position—47.1% of respondents. This means that for a significant portion of Ukrainians, Azerbaijan is not a country with a clearly defined emotional or political image.

Negative assessments remain relatively low, although they show some growth. The share of “mostly negative” attitudes stands at 4.9%, and “completely negative” at 1.6%. The share of those who were undecided is 2.1%, indicating a sufficient level of awareness among respondents regarding this country, but at the same time—a lack of clear reference points for evaluation.

The trend over the past six months points to a decline in the level of emotional certainty regarding Azerbaijan. The drop in positive assessments by more than 12 percentage points is accompanied by a sharp rise in neutral views. This may indicate a weakening of the country’s media presence in the Ukrainian media landscape or a decline in the relevance of bilateral issues in public discourse.

Compared to European Union countries or Ukraine’s strategic partners, Azerbaijan is perceived much less unequivocally. The high proportion of neutral assessments means that public opinion regarding this country is less stable and more sensitive to external factors—whether informational, political, or economic.

“If we look at these results, we see that attitudes toward Azerbaijan are not negative, but they are becoming less defined. The decline in positive assessments is not due to an increase in criticism, but rather to a shift of some respondents into the neutral zone. This means that the further shaping of the country’s image will largely depend on its activity in the Ukrainian information and economic spheres,” noted Maksym Urakin, founder of the Experts Club information and analytical center.

Thus, the survey results indicate a gradual weakening of Azerbaijan’s positive image in Ukraine, which is not accompanied by a sharp rise in negative sentiment but manifests itself in an increase in the share of neutral assessments. This creates both challenges and opportunities: on the one hand, the country is losing some of its positive perception, and on the other, it retains the potential to restore it through more active engagement with Ukrainian society.

According to a study conducted by the Experts Club Information and Analytical Center based on data from the State Customs Service, Azerbaijan ranks 36th in total trade volume of goods with Ukraine as of December 31, 2025, with a figure of $511.2 million. At the same time, imports from Azerbaijan slightly exceed Ukrainian exports, resulting in a moderate trade deficit of $44.7 million.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, AZERBAIJAN, EXPERTS CLUB, Pozniy, SOCIOLOGY, SURVEY, UKRAINE, URAKIN

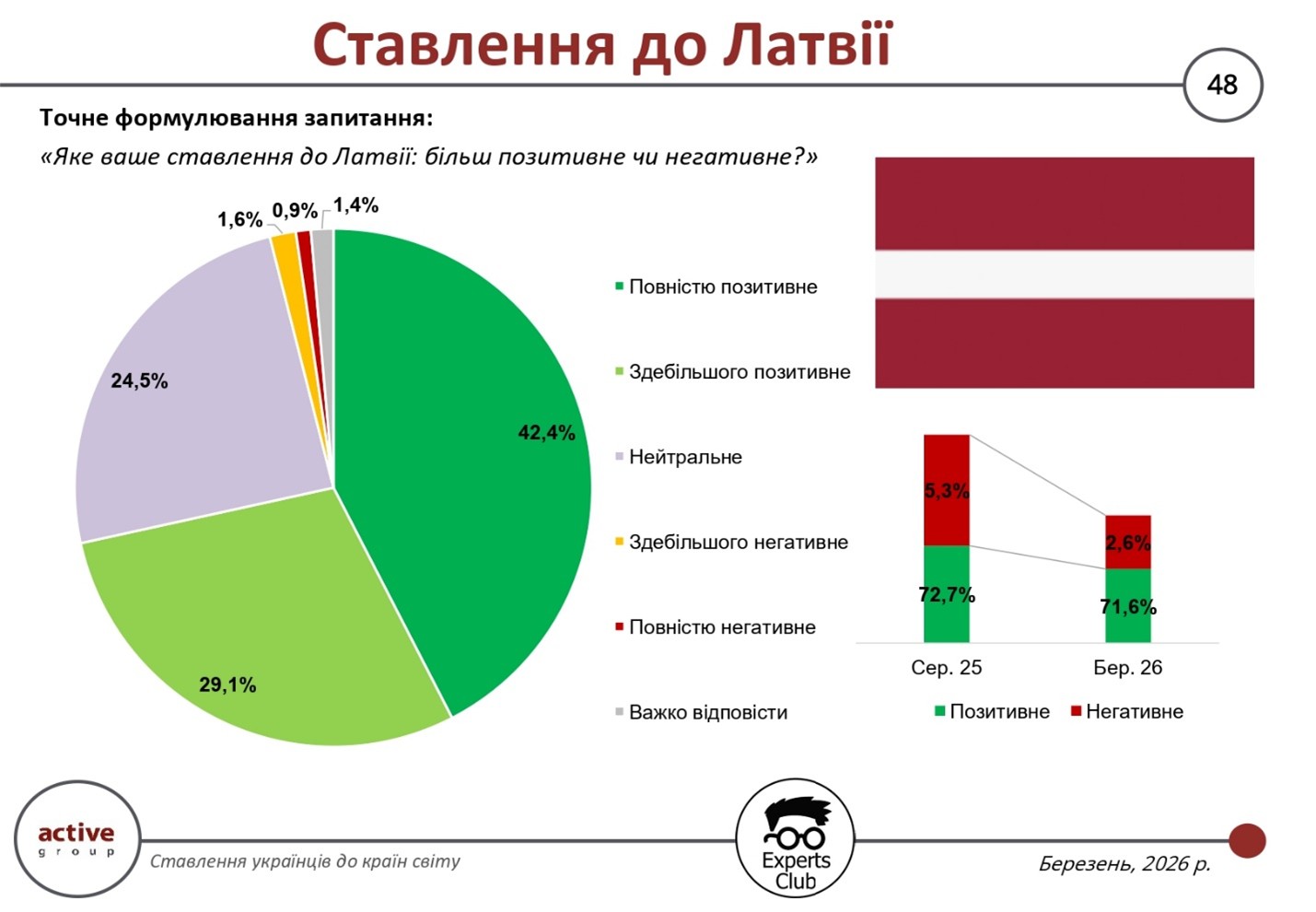

In March 2026, Ukrainians’ attitudes toward Latvia were characterized by a high level of positive perception and a low proportion of negative assessments. According to the results of a survey conducted in March 2026 by the research company Active Group in collaboration with the Experts Club information and analytical center, a total of 71.6% of respondents expressed a positive attitude toward this country, which is only slightly less than in August 2025 (72.7%). At the same time, the share of negative assessments has more than halved—from 5.3% to 2.6%—indicating a further strengthening of the overall positive perception.

The breakdown of responses shows a clear dominance of positive assessments. The share of those who have a completely positive attitude toward Latvia stands at 42.4%, while another 29.1% selected the “mostly positive” option. Thus, it is the category of unconditionally positive perception that forms the foundation of the country’s image in Ukrainian society. A neutral attitude was reported by 24.5% of respondents, which is a relatively low figure for international studies of this type.

Negative assessments remain marginal. Only 1.6% of respondents expressed a mostly negative attitude, and another 0.9%—a completely negative one. At the same time, the share of those who could not decide on an answer is 1.4%, which also confirms the established and stable nature of public opinion regarding Latvia.

The dynamics of change over the past six months reveal an interesting trend. A slight decrease in the share of positive responses is accompanied by an even more significant reduction in negative assessments. This means that a portion of respondents who previously held a critical stance have shifted to either a neutral or positive stance, which generally improves the overall balance of perceptions of the country.

Compared to other European Union member states, Latvia remains among the countries with the highest levels of trust and favorability among Ukrainians. This result can be explained by a combination of political support for Ukraine, an active stance in international organizations, and clear communication at the level of state policy.

At the same time, a relatively significant share of neutral responses (24.5%) indicates that there remains potential for further strengthening the country’s image. For some Ukrainians, Latvia is not yet a country with a sufficiently deep informational or economic presence, which opens opportunities for strengthening contacts in the spheres of business, culture, and humanitarian cooperation.

“Ukrainians generally distinguish very well between countries that demonstrate consistent support for Ukraine. At the same time, the level of positive attitude is shaped not only by political statements but also by concrete actions that people can feel. That is why even small countries can have a very strong positive image,” noted Oleksandr Pozniy, director of the research company Active Group.

Thus, the survey results confirm that Latvia has established itself in Ukrainian public perception as a reliable and friendly partner. A high level of positive sentiment with minimal negativity creates favorable conditions for the further development of bilateral relations, particularly in the areas of the economy, security, and humanitarian cooperation.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, Latvia ranks 35th in total trade volume of goods with Ukraine, with a figure of $522.7 million. At the same time, Ukraine has a positive bilateral trade balance, as exports of Ukrainian goods exceed imports from Latvia.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, EXPERTS CLUB, LATVIA, Pozniy, SOCIOLOGY, SURVEY, UKRAINE, URAKIN

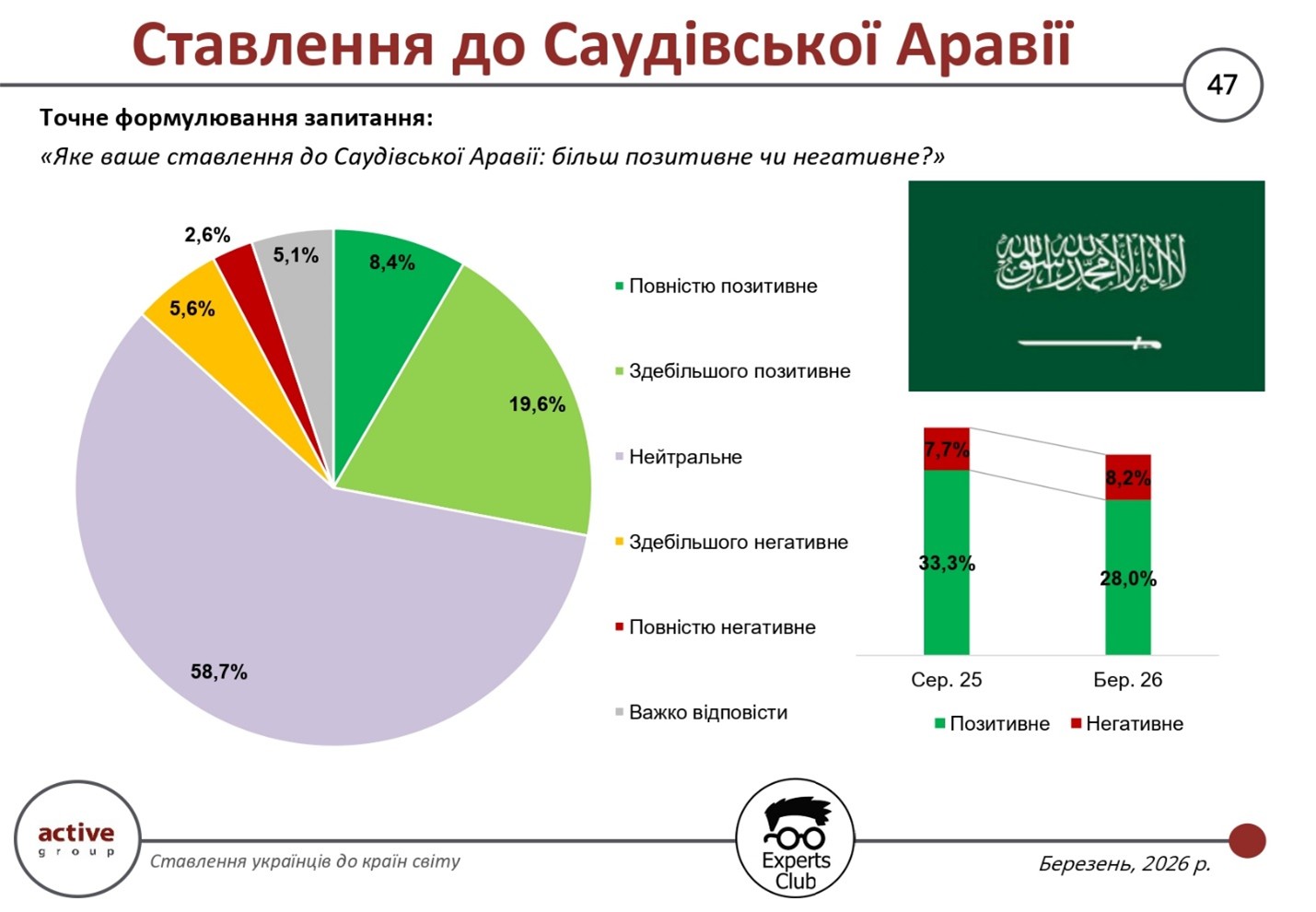

The results of a public opinion poll conducted in March 2026 by the research company Active Group in collaboration with the Experts Club information and analytical center show that Ukrainians’ attitudes toward Saudi Arabia remain largely neutral, though with a slight decline in positive assessments and a gradual increase in negative sentiment. This forms a perception profile characteristic of some Middle Eastern countries—low polarization with a high degree of uncertainty.

The overall level of positive attitudes toward Saudi Arabia stands at 28.0%. Of these, 8.4% of respondents view the country “entirely positively,” while another 19.6% view it “mostly positively.” At the same time, negative assessments reach 8.2% (5.6% — “mostly negative,” 2.6% — “completely negative”). As in previous waves of the survey, the largest share is held by neutral attitudes — 58.7%, while another 5.1% of respondents were unable to determine their position.

Compared to August 2025, positive attitudes decreased from 33.3% to 28.0%, while negative assessments rose slightly—from 7.7% to 8.2%. This trend indicates a gradual shift in the balance of assessments toward a more critical perception, although the changes remain moderate and do not go beyond the general neutral pattern.

The high proportion of neutral responses indicates that Saudi Arabia does not occupy a clearly defined place in the consciousness of Ukrainian society. Perceptions of the country are formed in a fragmented manner, without a systematic information presence or intensive contacts that could shift the balance toward more defined assessments. Under such conditions, even minor informational or political signals can influence the dynamics of public opinion.

“When we see that a country remains predominantly in the zone of neutral perception, it means that it effectively lacks sufficient ‘weight’ in the everyday information landscape of Ukrainians. In such a situation, even small changes in the information landscape can shift the balance of assessments in one direction or another. That is why, for such countries, it is crucial not only to increase their presence but also to shape a clear and positive image,” noted Maksym Urakin, founder of the Experts Club information and analytical center.

Thus, Saudi Arabia remains in the group of countries with a predominantly neutral image in Ukraine, where the level of positive perception is gradually declining, while the negative segment is slowly growing. The further evolution of this balance will depend on the intensity of economic, political, and informational contacts between the countries, as well as on how actively Saudi Arabia can shape its own image in the perception of Ukrainian society.

According to a study conducted by the Experts Club information and analytical center based on data from the State Customs Service, Saudi Arabia ranks 34th in total trade volume with Ukraine, amounting to $530.8 million. At the same time, Ukraine has a trade surplus with this country, as exports exceed imports by more than 1.6 times.

The study was presented at the Interfax-Ukraine press center; the video can be viewed on the agency’s YouTube channel. The full version of the study can be found at this link on the Experts Club analytical center’s website.

ACTIVE GROUP, EXPERTS CLUB, Pozniy, SAUDI ARABIA, SOCIOLOGY, SURVEY, UKRAINE, URAKIN